In 3 articles, you’ll get a deep dive of Teqnion AB (76 pages).

It will be structured in three Parts:

Part 1 (today): From Compounding to Stress Test: Why the Model Cracked

Part 2 (today): From Repairing to Re-Accelerating: What Changed in 2025

Part 3: Show Me the Numbers: Cohorts, Margin Mix, and much more

All parts are now available in one PDF. You can download it below.

👔 Company Name: Teqnion AB (“Teqnion”)

🔎 ISIN: SE0012308088

🔧 Business model: niche industrial serial acquirer

🌍 Geographic exposure: Sweden, UK (sales in Europe)

📈 Stock Price: SEK 169

💰 Market Capitalization: SEK 2.9 billion (~$321 million)

👨💼 Number of CEOs since foundation: 2

👨👩👦 Founder-/Owner-operator: Yes

📅 CEO tenure: Since 2009

🥇 Insider ownership: 5.0% of shares

📊 10Y EPS CAGR: ~23%

🔁 Reinvestment profile: High

💸 Capital intensity: Capital-light

🏰 Moat: M&A edge due to size, type of acquisition targets and deal-making approach

🧨 Main risks: Execution, quality drift, M&A engine, key-person risk

🌳 Slow Compounding fit: Yes – high-quality serial acquirer

Business Model in a Nutshell: Teqnion is a small Swedish sector-agnostic serial acquirer that describes itself as a builder of a conglomerate of industrial companies. The company is run as a decentralized group of subsidiaries, with a strong emphasis on culture, cash generation, and M&A.

3.6. Phase 4 (2025-?): Closing the Process Maturity Gap and Gaining Momentum

Phase 4 is Teqnion’s deliberate shift from a people-driven holding company to a repeatable operating system by adding the minimum set of shared processes needed to stop small problems from turning into portfolio-wide earnings drag. In other words, it’s about fixing issues that have been compounding for years and ultimately culminated in the second multi-year crisis in Teqnion’s history.

Management describes 2025 explicitly as a “new Teqnion” period: changing how subsidiaries are measured, becoming more proactive with support when trends turn, and demanding faster reversals of negative trajectories than in the past. Concretely, the group is standardizing monthly P&L and balance sheet collection, CEO reporting, and a transparent KPI “collector sheet” built around simple green-flag metrics. The aim is to spot underperformance early and address it consistently, rather than solving it only after it has already compounded into a crisis.

“This is in the process of doing a lot of changes on the organizational level and how we measure ourselves within the group. We are on the road to doing something that will be the new Teqnion.” (Johan Steene, CEO, Earnings Call 2025 Q2)

Phase 3 was when Teqnion realized that decentralization can hide problems for longer than you expect. Phase 4 is the attempt to fix what went wrong and build an operating system that makes issues visible early and forces action before they turn structural. Management’s language shifts from explaining underperformance to engineering the response: standardized reporting, faster escalation, clearer accountability, and more explicit “trust, but verify” mechanisms that anchor autonomy in leading indicators rather than gut feel.

Phase 4 is about closing the process maturity gap and upgrading the acquisition strategy. Let’s look at what they have done so far:

3.6.1. Closing the Gap: From “Soft” Decentralization to Measurable Execution

There’s no silver bullet here. It takes a set of reinforcing adjustments working together.

“The issue on my side is that I have not established a stringent system for reporting and action. It has led to a bit of individual ways of working. Now, we have pulled everything back and established a standardized approach. We follow specific KPIs, and when we notice something is going wrong, we require immediate actions.” (Johan Steene, InPractice interview, 28.08.2025)

For example, management has introduced new reporting mechanisms, including a standardized monthly data flow.

“We collect the P&L and balance sheet monthly from each subsidiary. We also have a CEO report where they input numbers, some of which may be found in the P&L. We want them to focus on these numbers as well. It’s not complex; it’s common sense. We monitor earnings, EBIT for the last month compared to the budget and last year’s month. We also track sales, order intake, backlog, gross margin, net margin, and other metrics.” (Johan Steene, InPractice interview, 28.08.2025)

The clearest example is the “collector sheet.” It’s a KPI traffic-light system that management says was implemented and rolled out broadly around mid-2025.

“What we have done for about a quarter now is implement a collector sheet that we present to everyone. We want to ensure that all KPIs have green flags.” (Johan Steene, InPractice interview, 28.08.2025)

It’s best viewed as conditional governance: subsidiaries remain autonomous when they are “green,” but HQ becomes increasingly directive once early-warning indicators turn “red.”

green flag → freedom

red flag → autonomy is reduced and intervention increases

“As long as you have a green flag in the sheet, you’re free to do as you like because you’re on the right track. When you have a red flag, you lose some autonomy. We’ll step in and tell you what to do. First, tell us why we’re on red and what you’ll do to get back to green. If we don’t believe you, we’ll tell you what to do. I know I’m free as long as I’m green.” (Johan Steene, InPractice interview, 28.08.2025)

The point isn’t to centralize decisions; it’s to centralize signal.

“We lacked structures to capture data effectively, which made us slow and ineffective. Over the last year, we’ve put more safety measures in place to detect issues early and implement actions quickly, not just for the future but for immediate improvement.” (Johan Steene, InPractice interview, 28.08.2025)

Read that again. It’s critical. The issue wasn’t decentralization itself. The issue was that Teqnion didn’t have a sufficiently standardized early-warning layer across 20–30+ independent units. And management is unusually self-critical about this, explicitly saying that better systems and processes likely would have allowed them to act earlier and perform better.

“There are numerous reasons we’ve underperformed for a while, and I know we could have done better earlier if we had better systems and processes in place from the start.” (Johan Steene, InPractice interview, 28.08.2025)

“I mean, decentralization still is the heart and the center of our business model. Where I think that we have not done good enough, and to be honest, far from good enough, is that decentralization works when you have individuals that are doing the right things, that have autonomy to do the right things, but it’s also people that have the capabilities and the ownership, feeling the ownership of doing the right things. If there is a person like that that is running the company in the right direction, autonomy is the right to go, and decentralization is the model.

However, when we see, and we are following this up more closely nowadays, when we see that operations are deteriorating, and we’re not talking about the financial numbers, but rather more forward-looking indicators, in those cases, we need to be quicker to identify that as number one, and secondly, to ensure that the people that are running the companies are running in the right direction. It’s really about trust, but verify. As long as the person is doing the right things, it is an autonomy. The more we feel that it’s going in the wrong direction, in the first step, they need to explain to us why it’s going in that direction that we feel is wrong. They also need to tell us the plan of righting the ship. If we believe in that, then we support that CEO fully in going in that direction, full steam ahead.

If we try that, or if we don’t feel that they are having the right plan of righting the ship, then we get to a point where we basically have to draw up the map and say, “This is now your journey going forward. Please implement.” If that is going in the right direction, then everyone is happy, and hopefully we all learn something.”

(Daniel Zhang, CXO and Co-CEO, Earnings Call 2025 Q2)

This also explains why Phase 4 inevitably creates more “friction.” If you move from broad trust and light-touch follow-up (where problems were sometimes addressed too late) to a model where underperformance triggers immediate scrutiny, the system will feel tighter. Management acknowledges this directly: there is more friction now because they are making clearer demands of the leaders who are responsible for running them well.

“There’s more friction since we have been more actively out with the subsidiaries and putting demands on the people that have given the responsibility to run them well.” (Johan Steene, CEO, Earnings Call 2025 Q2)

When performance deteriorates, subsidiary CEOs are expected to put forward a clear business plan and action plan. If they can’t, Teqnion helps build one. And if execution still doesn’t improve, management is prepared to conclude that it’s simply the wrong person in the role.

“If the subsidiary CEO is not able to produce a great action plan, then we will help them to develop one of those and then make sure that they follow them. If that’s not possible, of course, maybe that’s the wrong person for the job.” (Johan Steene, CEO, Earnings Call 2024 Q4)

“We will ask the companies for a business plan or action plan of how to make things better and see if they deliver on it, if we like the action plan. If we do not think the action plan is good, we make the action plan for the CEOs and ensure that they will run with it. If they do not, we find someone that will do it for us. It sounds harsh. I think that we’ve been a little bit too patient, to use a nice word, during 2024.” (Daniel Zhang, CXO and Co-CEO, Earnings Call 2024 Q4)

This highlights a potential downside of a soft-skill, trust-heavy leadership style, especially in a decentralized model where you assume local CEOs will do the right thing without constant oversight. It can delay tough calls.

In addition, Teqnion introduced a new governance structure in 2025 with two divisions: the Nordics and the UK Each division is led by a segment head who reports to Johan and Daniel. The goal is to strengthen accountability, improve scalability, and deepen local market insight.

In other words, Phase 4 is Teqnion formalizing what decentralization always required, but what had been enforced inconsistently: clear measurement, fast trend detection, and a repeatable escalation playbook. Management even frames it as moving away from “how we feel” and toward following metrics.

“We have metrics that we actually look at and we follow up on the metrics and not so much on how we feel.” (Johan Steene, CEO, Earnings Call 2025 Q2)

A subtle but important architectural change is that Teqnion is also tightening its follow-up culture. Management says the approach was historically too unstructured and insufficiently standardized, and it directly links the new “country manager” role to more structured, closer follow-up.

“The way we have been organized, just to be self-critical of myself, is that we haven’t followed up close enough in a structured way and maybe a little bit in a, let’s say, standardized way. That is the new role of the country managers that we will have.” (Johan Steene, CEO, Earnings Call 2025 Q2)

3.6.2. Raising the Quality Bar in M&A

The second fix is the acquisition engine itself, both what Teqnion buys and how fast it allows itself to buy.

Management’s messaging is now remarkably consistent: focus on higher-quality companies with stronger earnings and cash flow, niche offerings, real pricing power, and margins above the group average, so the group’s mix (and margin profile) improves mechanically over time.

“What we constantly try to improve even in this case is that we try to find higher quality companies, meaning that our the things that we look in a company, high earnings, high cash flow and niche products and whatever that we look at companies that are better, better in those aspects.” (Johan Steene, CEO, Earnings Call 2023 Q1)

“We are also acquiring companies with higher margin than the average margin from the group. So over time, we’re going to increase it and our goal is to constantly increase it.” (Johan Steene, CEO, Earnings Call 2024 Q2)

Management lays out fairly concrete criteria for what it wants to own: high margins, high returns on capital, resilience, strong cash conversion and ideally businesses that control more of their own destiny (own brand, own design/product) rather than being price-takers.

“We meet a lot of companies and what we’re looking for is, of course, companies that we believe is going to be relevant in the decade and more fulfilling these criteria that we mentioned already. They should be really good. They should have high margins, high return on capital and they should produce something that is more or less their own like their own brand name, their own design product or so they hold their own future in their own hands so to speak. Also, we look at the free cash flow there. We look at how good they are at actually turning their earnings into cash. And yes, so we should understand what they’re doing. We should realize that it’s a strong and resilient business model and we should believe that the people is really good at what they’re doing. And then of course there’s so many other aspects to look at, but those are a few things that we definitely look for and try to pinpoint before we proceed to try to acquire something.” (Johan Steene, CEO, Earnings Call 2024 Q3)

Management is clear about what they are avoiding going forward: turnarounds, startups, and typical contract manufacturers. They’re equally clear about the lesson learned: in some cases, they didn’t apply their own criteria strictly enough. Reward Catering is one example they cite, highlighting the importance of a long, proven operating history, since Reward was acquired only four years after it was founded.

“When it comes to the non-negotiables, I mean, the financials, historical robustness when it comes to growth, when it comes to profit margin, when it comes to return on capital, and having an organization where knowledge is spread out and importance is spread out, also when it comes to customers and suppliers, those are things that are super important for us.” (Daniel Zhang, CXO and Co-CEO, Earnings Call 2025 Q1)

“We don’t buy from anyone that has, you know, started a company three years ago, and then we buy it. We want a longer track record than that. We’ve done a mistake when it comes to that” (Daniel Zhang, CXO and Co-CEO, Earnings Call 2025 Q3)

“When it comes to Reward Catering, we just didn’t follow our own criteria, at least in one aspect. That was to acquire companies that have a long, solid history.” (Johan Steene, CEO, Earnings Call 2025 Q3)

Phase 4 also brings in a more mature concept: absorption capacity. In other words, the bottleneck is absorption capacity, not deal flow. It’s the ability to integrate, follow up, and support new subsidiaries without breaking the core.

That’s why management says it could do more deals, but deliberately holds back. They want to ensure they have the capacity to onboard new companies properly and they want to pay the “right” price.

“We look at many, many companies and we could acquire more, but we want to be sure that we have the resources to incorporate them into the group in a good way and also that we find companies that we pay the right amount of money for.” (Johan Steene, CEO, Earnings Call 2024 Q2)

Johan and Daniel are putting in place a structure designed to reduce one of Teqnion’s earlier vulnerabilities: being pulled between operational firefighting and continuous deal sourcing.

As discussed above, both have emphasized buying higher-quality companies as a way to reset portfolio construction. They now articulate a clearer ambition to build a more robust group by acquiring businesses that are less macro-dependent and have more uncorrelated risk versus the existing portfolio, explicitly to avoid ending up in the same situation again.

“We’re looking for companies that are not as dependent on macro, and we’re looking for companies that have uncorrelated risk with the rest of the companies so that we can build a more robust group because we never want to be in this current situation again.” (Daniel Zhang, CXO and Co-CEO, Earnings Call 2024 Q4)

This is not just a “quality” shift; it’s a risk architecture shift.

In fact, the recent UK acquisitions are higher-margin businesses and less economically sensitive, improving returns on capital and reinforcing the “acquire better over time” strategy.

The early indicators are compelling. The nine companies acquired in 2025 delivered, on average, a 25% EBT margin over the first three quarters, with a range of 14–45%. Compare that with Teqnion’s historical group EBT margin of roughly ~10–11% (in good years), and the quality upgrade becomes obvious. If this high-margin cohort continues to grow as a share of the portfolio, it should mechanically lift the group’s profit margin profile over the coming years.

As you keep adding margin accretive companies to your portfolio, you’re bound to see some significant margin expansion

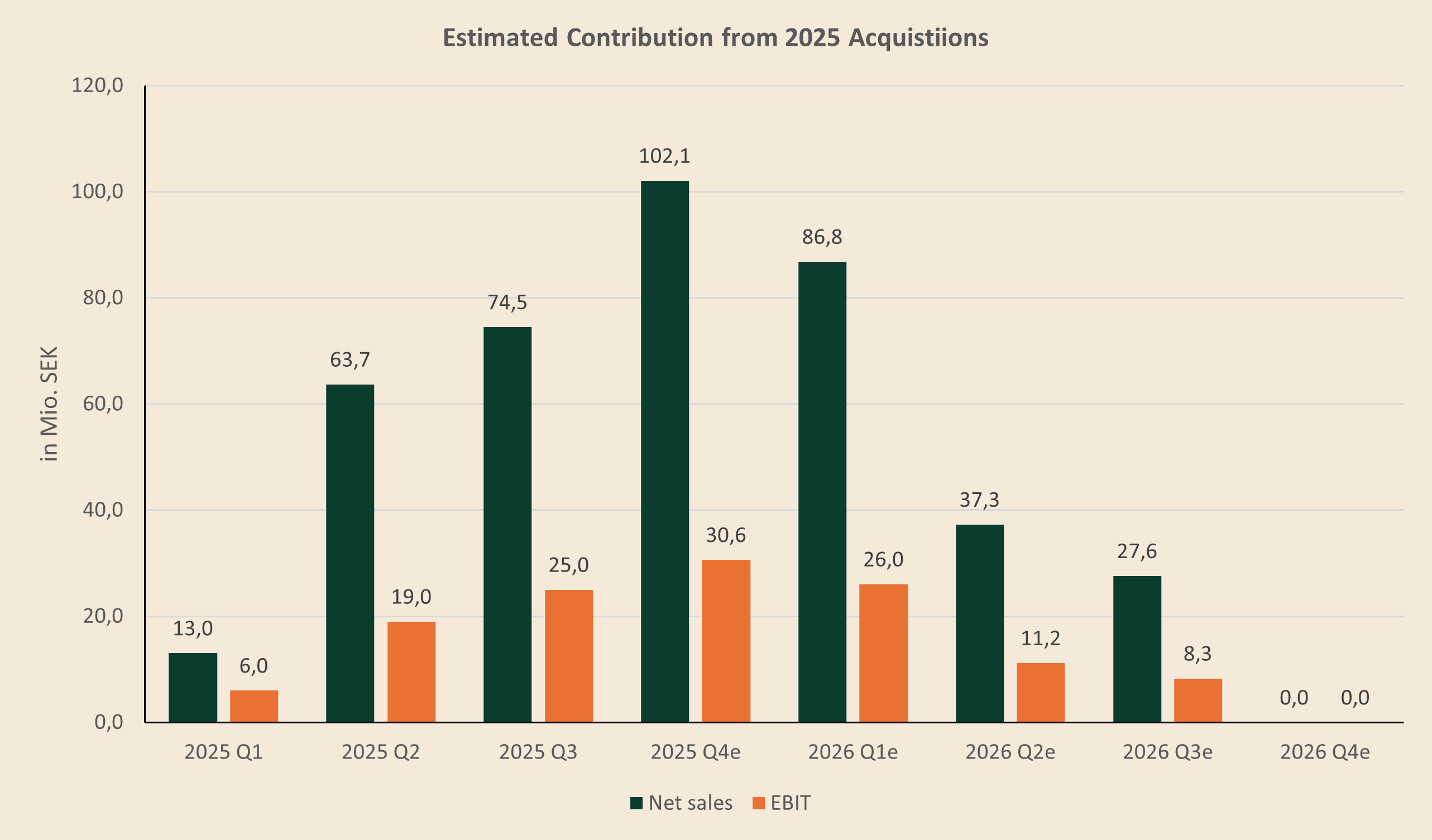

Quick thought experiment: Teqnion reported, that the 2025 acquisitions contributed SEK 25 million EBT in Q3 2025. Since two of the nine companies were only consolidated toward the end of the quarter, the “run-rate” EBT contribution should be higher. If we assume SEK 30 million per quarter, that implies SEK 120 million per year. For context, Teqnion’s group EBT in 2024 was SEK 119 million. Put differently: the 2025-acquired companies could be generating roughly as much EBT as the other ~30 subsidiaries combined.

A visible profitability step-up is already within reach and neither does it require heroic assumptions nor redeployment of capital during 2026. The chart below is a simple timing bridge for the 2025 acquisition cohort. Methodically, I take the average revenue of the nine acquired companies over the last three years as reported by Teqnion (as a proxy for a “normalized” revenue base) and then allocate that revenue linearly from the quarter in which each company was consolidated. I apply the same logic to earnings, using the profitability disclosed for the cohort to translate the phased revenue into an estimated quarterly profit contribution. This is not meant to be a precise forecast. It’s a directional tool to understand when the cohort should show up in the reported numbers as consolidation rolls through.

The picture is intuitive: the contribution ramps as more companies are consolidated for a full quarter. You get a partial contribution in early quarters, then a meaningful step-up once the cohort is fully in the numbers, and finally a normalization as the comparison base catches up. Importantly, when you sum the quarterly contributions, you end up with ~SEK 400 million of annualized revenue and ~SEK 120 million of annualized earnings across the quarters. In other words: even without any further capital deployment in 2026, and even if the struggling bucket doesn’t improve materially, the “math” alone suggests Teqnion should see a tangible earnings step-up as the 2025 cohort becomes fully reflected in the P&L.

The largest year-over-year step-up in EBIT should come in Q4 2025. On my estimates, 2026 EBIT could be roughly ~SEK 45 million higher than 2025 from full-year consolidation alone—and for context, full-year 2024 EBIT was SEK 148 million.

3.6.3. Incentives, Hiring, and Accountability

Phase 4 is about more than dashboards and deal criteria: it’s also about people and behavior. Management openly says it has changed the type of people it hires, putting more emphasis on a “business mindset” and a clear understanding of how to make money.

“We changed during the year when it comes to what type of people we hire. We focus much more on the business mindset of those individuals, and they should have a clear view on how to make money.” (Johan Steene, CEO, Earnings Call 2024 Q4)

That’s a cultural signal: Teqnion is trying to reduce the risk that a subsidiary drifts operationally because its CEO lacks commercial sharpness.

Even more telling are the incentive changes. Management says it has tightened incentives through a bonus structure with both upside and downside. A “negative” theoretical bonus carries forward and is netted against future positive bonuses.

“Yeah. I should maybe also add that we have changed the bonus structure a little bit in order to tighten the incentives a little bit. It is exactly as what Johan said, but there’s also a change so that if the theoretical bonus was negative, i.e., the results are lower, that’s a negative bonus that you will be carrying forward and netted against future plus bonuses. It is upside and downside. Maybe one more change that we can add for flavor is that if you get a high bonus, you will be forced to use part of that to actually buy shares on the open market that you will need to keep to create even more incentive alignment.” (Daniel Zhang, CXO and Co-CEO, Earnings Call 2024 Q4)

That’s a meaningful shift because it discourages short-term smoothing. In addition, management describes requiring that part of a high bonus is used to buy Teqnion shares in the open market and hold them. This explicitly strengthens alignment.

Put together, it forms a coherent picture. Phase 4 is Teqnion making decentralization conditional on performance and competence and embedding that logic into processes (KPI sheet, standardized reporting), people decisions (CEO replacement if plans or execution are inadequate), and incentives (downside carry plus share purchases).

3.6.4. Why this Phase Can Change the Long-term Trajectory

The simplest way to summarize Phase 4 is this: Teqnion is trying to become the kind of serial acquirer it always aimed to be; one that compounds through decentralization, but with a holding-company control layer mature enough to prevent multi-year deterioration from compounding in silence.

Management itself frames this as an organizational transformation:

“This is in the process of doing a lot of changes on the organizational level and how we measure ourselves within the group. We are on the road to doing something that will be the new Teqnion.” (Johan Steene, CEO, Earnings Call 2025 Q2)

That brings us back to the time horizon. The measures Teqnion has taken are not meant to “fix” a single quarter. They are meant to build a platform that should look meaningfully different several years from now.

4. M&A Playbook 2.0: Raising the Bar

Teqnion’s compounding story ultimately comes down to acquisition quality. The company can build a better operating system, but if new deals are low-margin, cyclical, or require constant fixing, the portfolio will never reach a “mostly fine” steady state.

The encouraging part of Teqnion’s current narrative is how explicit management is about raising the bar. They repeatedly say the number one rule is to buy high-quality companies that require very little work from the parent. They also acknowledge that earlier in Teqnion’s history, limited capital often meant that “turnaround is what you get”—a candid way of saying the group sometimes bought what it could afford, not what it would ideally have wanted.

Stripping down Teqnion to one principle: the main growth engine is acquisitions. Management is clear that this remains the key lever going forward, but it is just as clear that they won’t “do deals” simply to hit an annual quota or to meet short-term investor and analyst expectations.

“But we will never do businesses, do deals just because to get hit a certain number of deals in a certain year.” (Daniel Zhang, CXO and Co-CEO, Earnings Call 2023 Q3)

What has changed materially is the quality bar, and the infrastructure that makes the acquisition engine repeatable. In other words, Teqnion is trying to preserve what made the model work (simple rules, disciplined valuation, human trust) while upgrading what made it fragile (wide variance in portfolio quality, integration strain, and inconsistent follow-up).

4.1. The “Unchanged Core”: Buy Forever, Avoid Fads, Demand Cash

Teqnion’s long-term orientation shows up in how management talks about targets and how it structures deals. The message is simple:

Teqnion isn’t buying businesses to look good next quarter. Teqnion is buying businesses it wants to own “forever.”

“The thing is that we don’t buy things for now to perform well now. We buy things that’s going to be with us forever.” (Johan Steene, CEO, Earnings Call 2022 Q2)

“We tend to focus on industrial companies that sell something that hopefully will be needed by society in more or less with a tweak forever.” (Johan Steene, CEO, Earnings Call 2023 Q3)

“So in the early days where we bought companies where we thought that there will be very limited organic growth, getting our money back in 5 years meant more or less 5 times earnings after tax. Nowadays when we buy companies where we think that there is a higher growth potential that multiple of course it becomes higher, but we are not multiple focused. We are cash flow focused, future cash flow focused.” (Daniel Zhang, CXO and Co-CEO, Earnings Call 2023 Q1)

That mindset has a few practical consequences that have remained remarkably consistent over time:

First, Teqnion prefers businesses where demand and product relevance change slowly, and where compounding is driven by relationships, know-how, and niche application expertise.

“And we don’t try to find what’s hot at the moment or trending at this time. It’s try to find things that we believe is going to be something that’s needed in a long way in the future.” (Johan Steene, CEO, Earnings Call 2023 Q1)

“We try to find things where things change very, very slowly, where we can build the business on having great relationships” (Daniel Zhang, CXO and Co-CEO, Earnings Call 2023 Q1)

Second, the group has long favored “light” balance sheets, i.e. businesses that don’t require heavy capex or large machine parks, and where earnings convert into cash at a high rate. That’s why valuation discussions are often anchored in a proxy for free cash flow (earnings after tax as an approximation), and why cash conversion is repeatedly emphasized as a core filter.

“So when we look at it, we try to look at companies where the profit net of tax more or less is very close to free cash flow over time.” (Daniel Zhang, CXO and Co-CEO, Earnings Call 2023 Q4)

“We tend to focus on companies that have a light balance sheet and doesn’t need to buy many machines or things inventory to function. That’s one of our criteria when we’re searching for good companies.” (Johan Steene, CEO, Earnings Call 2023 Q3)

Third, Teqnion’s valuation discipline is consistent across the cycle. Management explicitly says it didn’t “expand multiples” when interest rates were low and it isn’t “shrinking” the hurdle rate now that rates are more normal either. That matters because serial acquirers don’t just need good targets; they need price discipline that holds up across macro regimes.

Beyond the long-term mindset, Teqnion’s “unchanged core” also shows up in how it structures ownership and risk. The group has consistently preferred clean, unambiguous control. Teqnion typically acquires 100% of a target to create a clear cut. Everyone knows who is responsible for running the company going forward, while using earn-outs as a strong incentive mechanism for sellers and continued performance.

“I think for us, we’ve always acquired 100% to make a clear cut. It’s very, it’s obvious to everyone involved who is responsible for running the company going forward. We have the incentive for the sellers in earnouts that is very, very strong normally.” (Johan Steene, CEO, Earnings Call 2025 Q3)

In parallel, Teqnion has remained conservative on balance-sheet risk at the target level. It typically avoids acquiring companies with debt, reinforcing its preference for asset-light businesses where earnings translate into cash.

Finally, management consistently communicates a target of earning back its investment in roughly five years on a realistic forecast (using earnings after tax as a proxy for free cash flow), and it brings that into the conversation early to avoid wasting anyone’s time.

“We try to get our money back or our investment back in 5 years on a realistic forecast. So, we talk with the seller of the company about realistic forecast. And we when we both have agreed on that, we see that we have there is a good chance for us to get our investment back in 5 years and the seller feels that that’s fair value of their company, then we will proceed and do business together. And we have had that approach since we started in 2006 and we still have the same approach and it seems to be working.” (Johan Steene, CEO, Earnings Call 2023 Q1)

“We try to be quick since we’re strict on valuation rules. We talk to many good companies to find a few that value selling to us over others who might pay more. We lay this out quickly to save everyone’s time, as we meet with many companies annually to find the right ones.” (Johan Steene, InPractice interview, 28.08.2025)

4.2. The Early Playbook: Good Rules, Messy Targets (and why that Mattered Later)

Here’s the candid part Teqnion has increasingly been willing to say out loud: it didn’t always buy what its own rulebook would call “ideal.” In the early years, especially when capital was constrained and the organization was tiny, targets were often selected because they were available and affordable, and sometimes because they looked “cheap” on paper. In hindsight, that led to periods where Teqnion acquired businesses that didn’t fit the long-term profile: more cyclical exposure, weaker pricing power, and structurally lower margins (for example, certain contract manufacturing situations).

Practically, that means it helps explain how the acquisition engine could “work” for many years while quietly building fragility. If you buy businesses that need more fixing, the holding company’s operating system has to be stronger to prevent small problems from compounding into big ones.

4.3. What’s New in Playbook 2.0

The “2.0” shift is a bundle of upgrades all pointing in the same direction: reduce portfolio volatility, improve structural margin quality, and treat integration capacity as a real constraint.

Higher quality filters (margin, cash, resilience)

Management describes a clear intention to “constantly improve” the quality of acquired companies, explicitly linking this to higher earnings power, stronger cash conversion, niche products, and better returns over time.

You can see that evolution even in how they talk about target size and maturity. What used to qualify as “big enough” historically—only a few hundred thousand SEK of earnings—is no longer the bar. Today, they reference meaningfully higher earnings levels as the starting point for a serious evaluation.

The companies that we’re acquiring today are, on average, much bigger compared to three years ago, and those were bigger compared to ones three years ago. (Daniel Zhang, CXO and Co-CEO, Earnings Call 2025 Q1)

A cleaner “business model mix”

Teqnion increasingly frames the portfolio by “types” and is much more explicit about what it wants less of: businesses with weaker pricing power and structurally margin-compressed customer dynamics. That’s why the acquisition focus is shifting toward companies that control more of their own destiny: they own their brand, their design, and have specialized niche know-how.

Integration capacity discipline

A subtle but important sign of maturity is that management repeatedly says it could do more deals, but chooses not to unless it is confident it has the resources to onboard the company properly and pay the right price. In other words, integration capacity becomes a throttle, not an afterthought.

Geographic expansion

Teqnion has also started to broaden its opportunity set beyond Sweden. It’s a staged approach: learn one new territory well, build a self-sufficient local platform, and only then move to the next. The UK is the prime example of this approach, and management explicitly describes it as having a strong pipeline.

4.4. Acquisition Process: Sourcing, Valuation Conversations, and Soft Factors

Teqnion rarely competes with PE, as PE is usually not interested in small deals. Teqnion wins on trust, alignment, clarity, and speed—not the highest price. That only works if you consistently explain how you operate after the deal, and then actually live up to it.

A few elements reinforce that advantage:

They meet many companies each year and try to be quick and transparent about valuation expectations, often after the first real meeting, so sellers don’t burn emotional energy.

“And I think we meet a bit over 100 companies in meetings every year” (Daniel Zhang, CXO and Co-CEO, Earnings Call 2022 Q4)

The seller is treated as a future partner. That’s also why Teqnion is cautious about using stock as acquisition currency: if the shares are undervalued, issuing them dilutes existing owners; if they’re overvalued, it’s unfair to the seller you’re trying to turn into a long-term partner.

“I mean for us if we would pay with stock when we think that it’s undervalued, we would never do that because we are owners of this company as well, we don’t want to give away that value. So it would make sense financially to do it when it’s overvalued. But we don’t want to do that either because the people that we pay become our partners.” (Daniel Zhang, CXO and Co-CEO, Earnings Call 2022 Q4)

Relationship building can be genuinely long-cycle. Management explicitly references multi-year dialogues with entrepreneurs before closing. For example, Johan had been in contact with the owner of Schill Reglerteknik AB since 2015 before completing the acquisition in 2023.

In newer markets (like the UK), Teqnion has leaned more on broker relationships after learning that cold outreach alone can be too slow. Management explicitly frames “being straightforward, responsive, and keeping promises” as a way to improve lead quality over time.

“More and more sell-side advisors have learned that it’s actually fun to work with us, that we keep our word, etc” (Daniel Zhang, CXO and Co-CEO, Earnings Call 2025 Q3)

“But I think one of our competitive advantages when it comes to acquisition is our relationship building with potential sellers, with the entrepreneurs. I think they see after a while that we understand them and how tough it has been to build that company that they are trying to sell. And that is maybe soft values, but those soft values is still values. And since we tend to be very honest in what we see and what we kind of demand from them after transaction. If the people that likes what we do and likes Teqnion and want Teqnion to be a harbor for their life’s work, they sell to us and they sell to us at the price that and the valuation that we like and that we stick to.” (Daniel Zhang, CXO and Co-CEO, Earnings Call 2022 Q4)

4.5. Deal Structure: Five-year Payback and Earn-outs as Alignment (and Risk Control)

The capital allocation “math” behind the playbook is simple.

Teqnion aims to earn back its investment in roughly five years on a realistic base case (again using earnings after tax as a proxy for free cash flow). Downside is protected by keeping the upfront payment limited. Upside is then shared through earn-outs if performance improves materially over the next few years (more risk = less cash upfront and a larger earn-out component).

“On average, we pay between 60% to 70% upfront, and the rest is on earn-outs.” (Johan Steene, InPractice interview, 28.08.2025)

This also explains why Teqnion prefers sellers to stay involved for a meaningful transition period. Earn-outs aren’t just price mechanics. They’re incentive mechanics. They “incentivize the seller to stay on” and keep the business on its trajectory, with typical earn-out periods often lasting two to three years.

“We prefer to buy a company where the succession is in place or where the entrepreneur can stay on but we are also looking at companies where the owner wants to retire and then together with him or her, we make that succession happen over a 2 or 3 year period.” (Johan Steene, CEO, Earnings Call 2023 Q3)

Finally, there’s a practical, human side to succession. Many entrepreneurs sell because they want to step back. Teqnion frames the transition as a planned, multi-year process. In some cases, founders stay on as cultural ambassadors, board members, or part-time relationship holders while the next management layer is put in place.

“We usually discuss these matters thoroughly before acquiring a company, focusing on what the seller envisions for the future. Typically, when they sell the company, it’s because they want to pursue something else or reduce their involvement in running the business. In such cases, we agree to find new management within three years, hoping they enjoy working with us and choose to stay on in some capacity. They might continue for a day or two a week, or a few days a month, to maintain relationships with customers or suppliers and serve as a cultural ambassador for the company. We often invite them to join the company’s board, even if they’re not operationally involved anymore. Some individuals express a desire to continue working, which we appreciate. Although we don’t formalize this in writing, they might commit to five years before reassessing. If they decide to retire, we collaborate to find new management. However, some are ready to retire immediately upon selling, and they communicate this early on. In such cases, we ask for a certain amount of time to work together to find new management.” (Johan Steene, CEO, Earnings Call 2023 Q3)

4.6. Upgrading Diligence (Reward Catering Disaster)

One of the most valuable aspects of “Playbook 2.0” is that it’s not just about what Teqnion buys. It’s also about lowering the odds of repeating the same mistake.

Reward Catering was Teqnion’s first acquisition in Ireland, completed in September 2022. In early communications and Q&A, management described Reward as an asset-light niche player (final assembly in Ireland, with much of the work outsourced), with optionality to expand internationally, even mentioning the U.S. as a “very early days” opportunity.

At the time, Reward seemed to fit: a specialized product, strong entrepreneurial drive, and (apparently) attractive economics—exactly the kind of small business you’d want in a permanent home.

The situation later deteriorated into a seller dispute over the earn-out. In Teqnion’s own words, the disagreement “turned into a court case,” and during/after that process “a couple of other legal cases” emerged. The Irish court asked the parties to keep discussions in court and not in public, which limited what management could disclose.

By October 2025, Teqnion escalated significantly. It announced that it had decided to seek the appointment of provisional liquidators for Reward Catering. Around the same time, Teqnion recognized a goodwill impairment of SEK 73 million related to Reward, and management explicitly linked that impairment to the decision and process around pursuing liquidation.

For the Deep Dive, the key point isn’t the legal detail, it’s the process lesson Teqnion itself draws from it.

“It has been the biggest mistake that we’ve done.“ (Daniel Zhang, CXO and Co-CEO, Earnings Call 2025 Q3)

Management is direct about what they got wrong: (1) they didn’t fully follow their own criteria, especially the preference for companies with a long, solid operating history; and (2) they relied too heavily on third-party diligence reports, letting their own guard down.

The “fix” in the M&A process is described in concrete, procedural terms: running personal background checks not only on legal entities but also on the individuals involved; securing tighter and earlier control over critical systems (e.g., IT and banking access); and intervening faster when something looks off. Management also says that since then, they’ve walked away from several deals where the business itself looked fine, but personal-background signals raised concerns—an explicit cost of being stricter.

4.7. Summary: Playbook 2.0 Acquisition Criteria

The following table summarizes Teqnion’s acquisition criteria as described by management.

5. Acquisitions: The Track Record

Teqnion’s long-term compounding story is inseparable from its acquisition engine. Management is very clear that acquisitions are the primary growth lever: Teqnion is built to keep adding subsidiaries and let the portfolio compound over time.

This chapter takes a closer look at Teqnion’s acquisition history.

5.1. Acquisition History

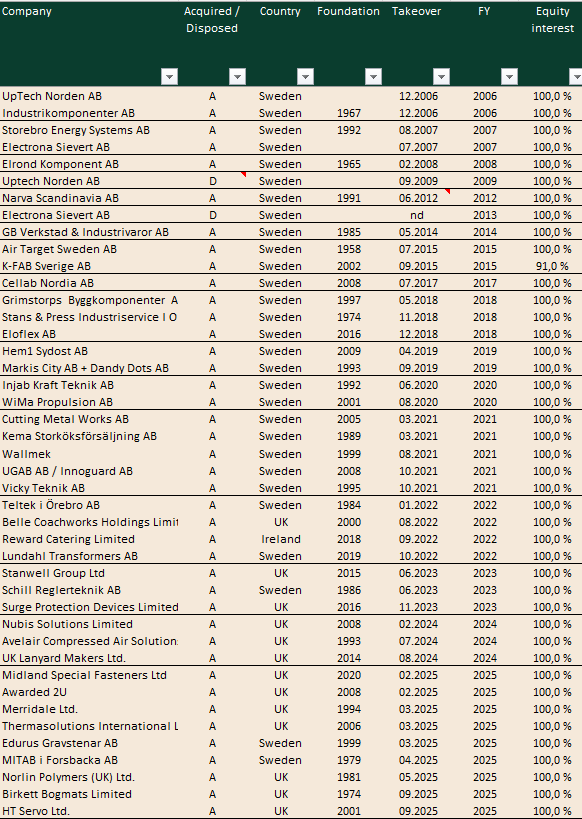

Before discussing outcomes, it’s worth laying out the transaction list. A complete acquisition table forces clarity: how quickly did the portfolio expand, when did the group expand abroad, and how concentrated is the portfolio in any one geography?

Let’s first look at what these businesses actually do (excluding UpTech Norden AB and Electrona Sievert AB, since they were disposed of / went bankrupt).

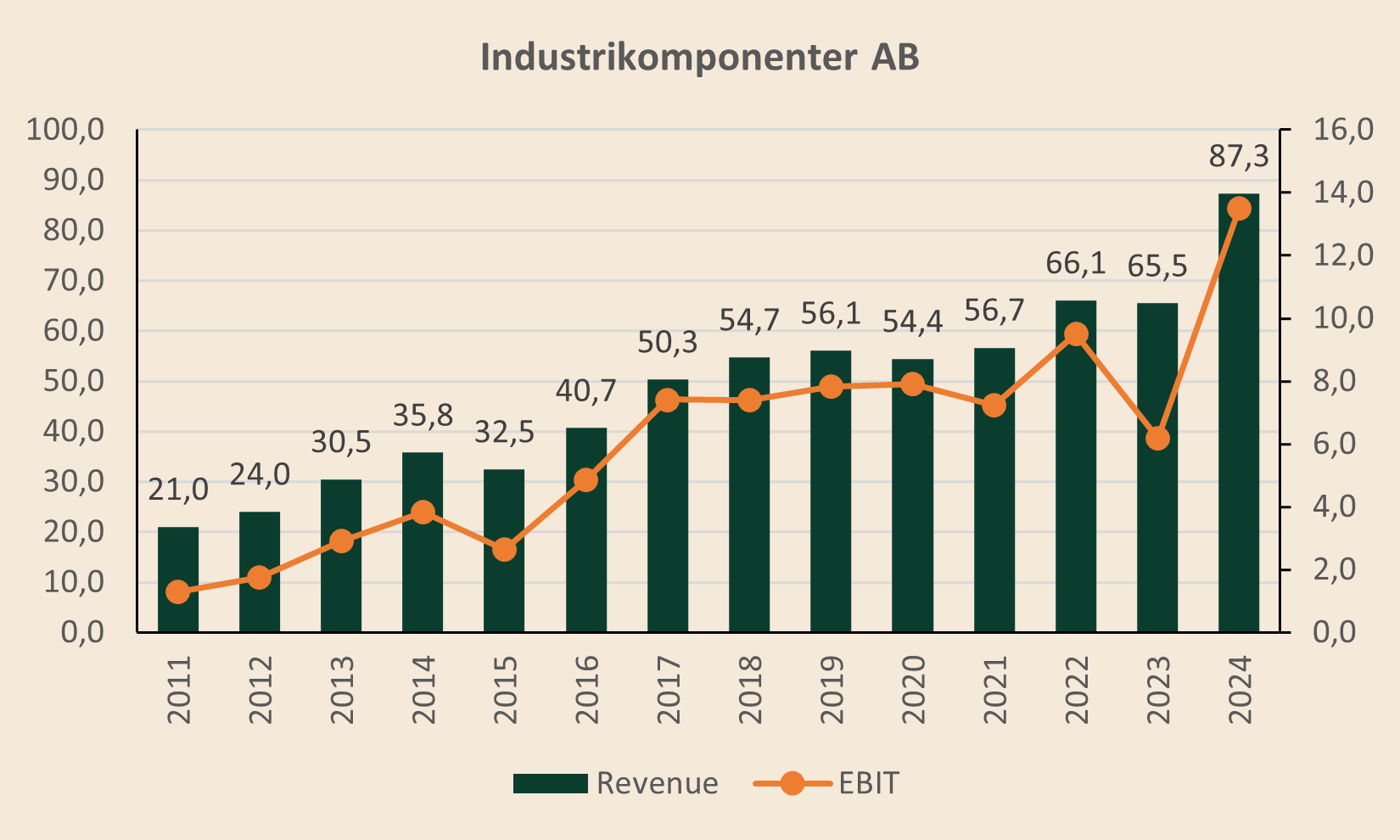

Industrikomponenter AB (2006): INKOM supplies electromechanical and electronic components for demanding industrial applications across the Nordics. The company acts as a specialized value-added distributor, combining strong supplier relationships with technical product expertise and reliable availability from its own warehouse.

Storebro Energy Systems AB (2007): Storebro Energy Systems operates in sales/trading and installation of electronic products, mainly serving customers in the leisure and automotive sectors. The model is largely product-based distribution plus installation/service work depending on customer needs.

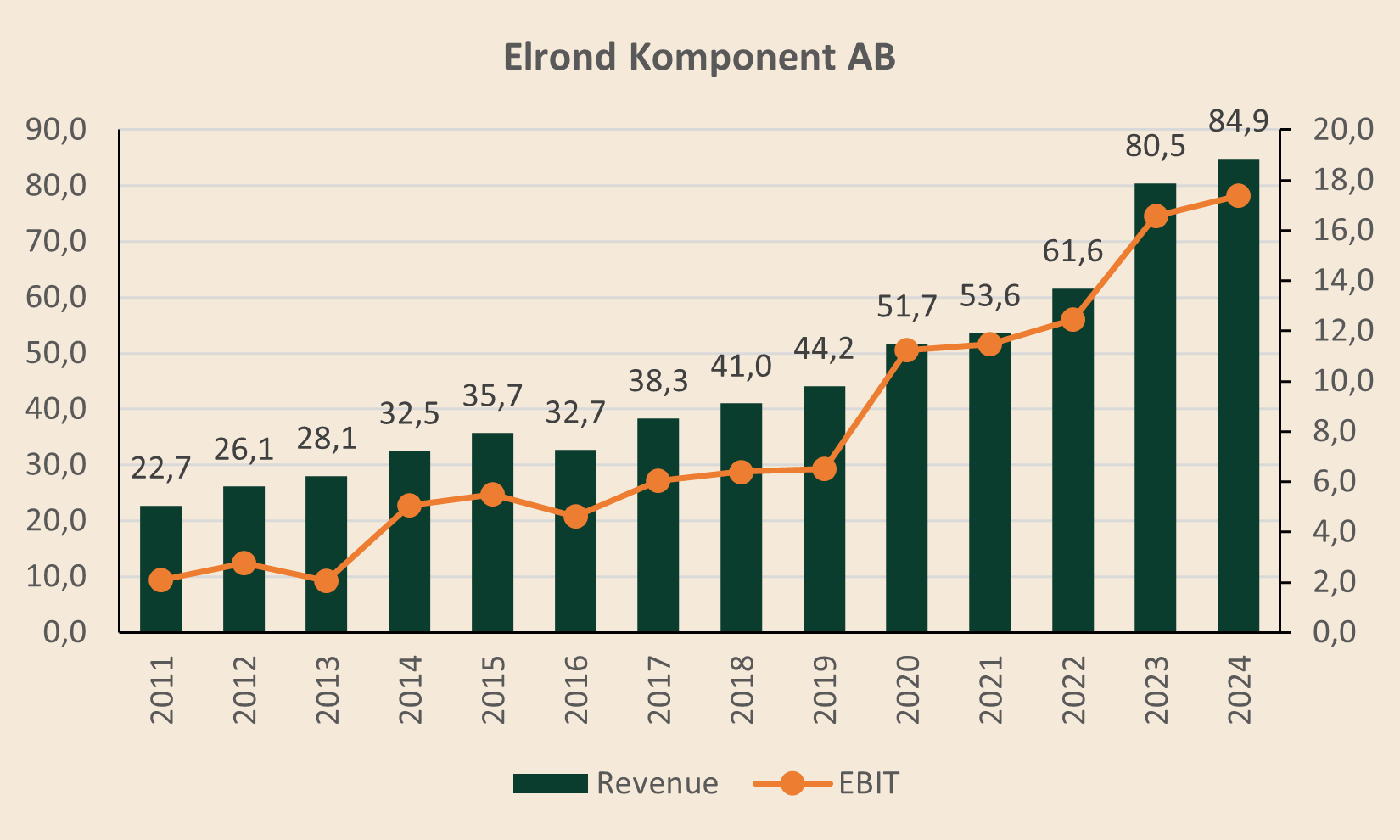

Elrond Komponent AB (2008): Elrond provides complete solutions for a safe electrical environment in automation and installation. It is a Nordic leader in lightning protection, offering surge/lightning protection products, UPS systems, and equalization materials, supported by commissioning and service.

Narva Scandinavia AB (2012): Narva Scandinavia sells light sources and LED lighting under its own brand (NASC), mainly to electrical wholesalers and professional customers across the Nordic region. The business is built around product availability, distribution reach, and a focused lighting portfolio.

GB Verkstad & Industrivaror AB (2014): GB Verkstad provides industrial consumables and components with one of Northern Sweden’s broadest assortments, ranging from fasteners and hydraulics to seals, bearings, lifting products, and transmission items. Its value proposition is local presence, fast access, and customized logistics for industrial customers.

Air Target Sweden AB (2015): Air Target develops and sells acoustic target indication systems used for military practice shooting with supersonic projectiles. It stores and presents shooting data and serves defense organizations in 30+ countries, operating as a long-lived specialist with global reach.

K-FAB Sverige AB (2015): K-FAB supplies modern, affordable lighting for home environments and sells through retailers worldwide. It combines Scandinavian product design and branding with international sourcing capabilities (including operations in China).

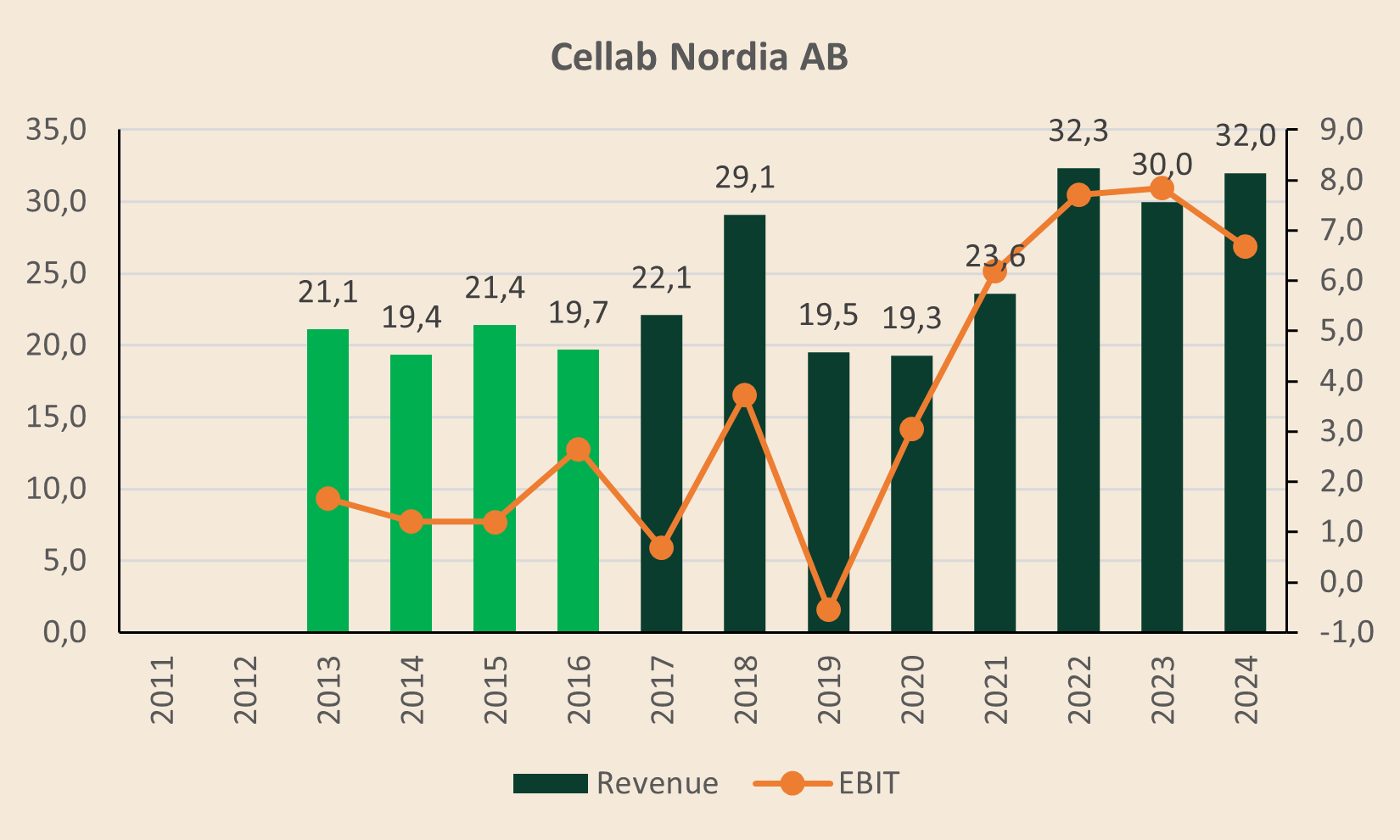

Cellab Nordia AB (2017): Cellab Nordia markets and sells laboratory instruments and consumables (pathology, histology, cytology, cell and molecular biology) and provides certified technical service. Customers are mainly clinical and research labs in Sweden, including pharma, biotech, food, and QA environments.

Grimstorps Byggkomponenter AB (2018): Grimstorps manufactures wooden building components such as trusses and house frames and delivers complete building kits (including drawings). The model benefits from industrialized production, reliability, and repeatable B2B demand in the construction supply chain.

Stans & Press Industriservice I Olofström AB (2018): Stans & Press is a contract manufacturer focused on high-quality sheet metal products. It operates with a modern machine park and long experience, serving both international industrial customers and smaller regional players.

Eloflex AB (2018): Eloflex is a European leader in foldable electric wheelchairs, sold across many markets. Products are often prescribed via public healthcare systems and also distributed via partner networks, with strong positioning in the assistive technology ecosystem.

Hem1 Sydost AB (2019): Hem1 sells architect-designed detached houses and takes responsibility for the entire construction process. With its own factory and long operating history, it functions as a turnkey homebuilder serving customers with customized “dream house” projects.

Markis City AB (2019): Markis City refurbishes and distributes professional coolers/freezers to beverage and food industry customers, extending equipment life through service and upgrades. The model blends logistics + refurbishment + customer relationships, supported by demand from major brands and sustainability-driven replacement cycles.

Injab Kraft Teknik AB (2020): Injab provides a full range of current and measuring transformers and deep application knowledge for installation. It also supplies relay protection (low/medium voltage) and components for grid stations and medium/high voltage use cases.

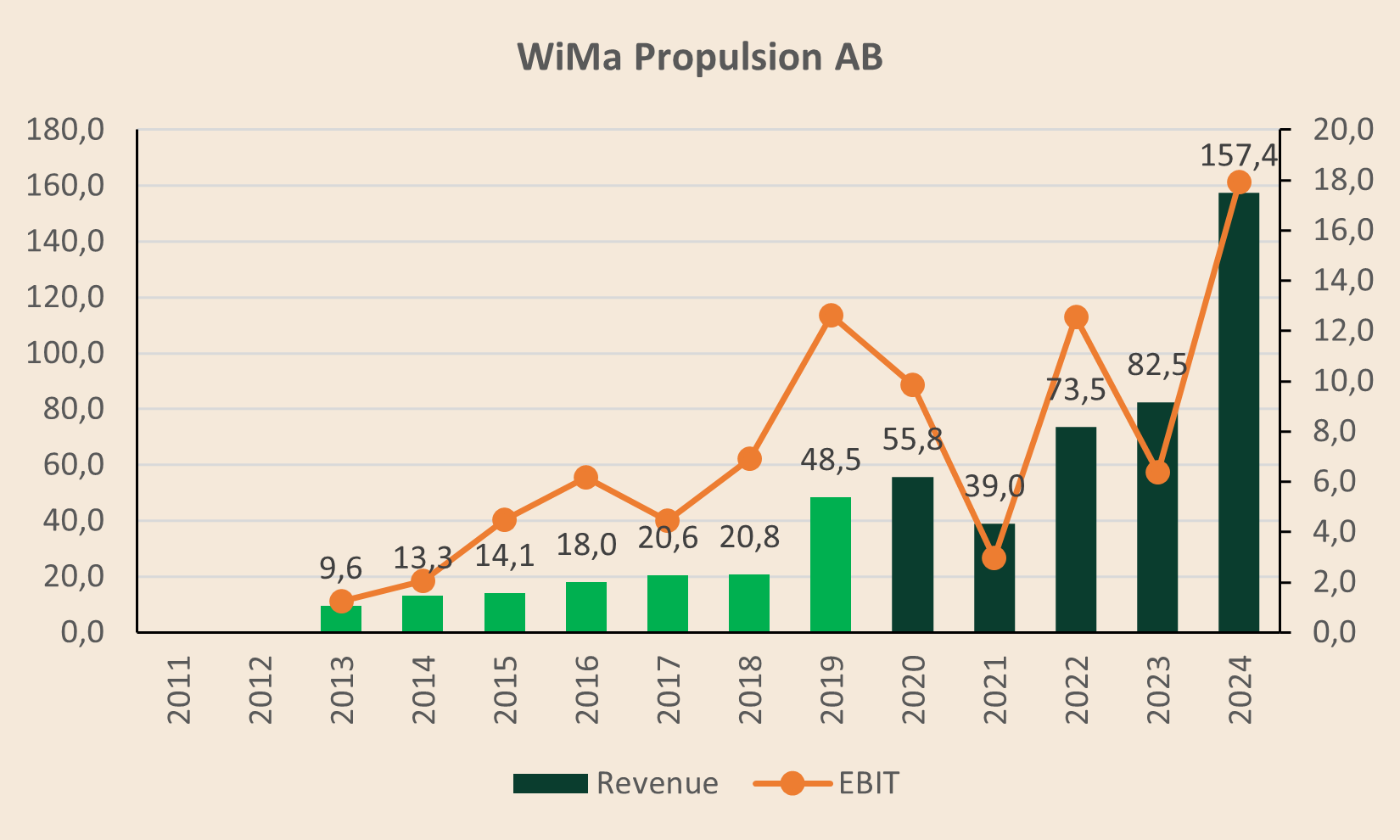

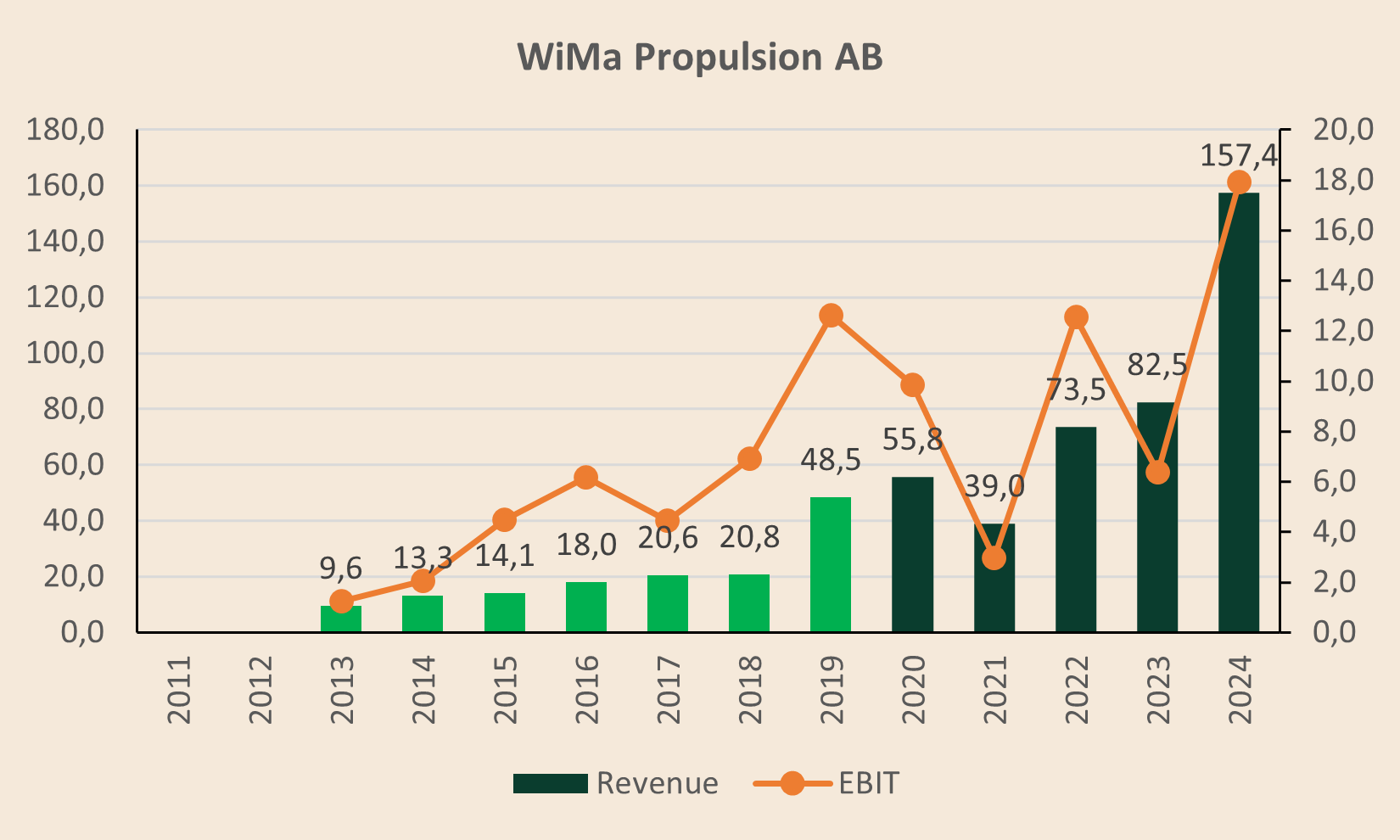

WiMa Propulsion AB (2020): WiMa repairs and maintains gas turbine installations both in-house and in the field. The company supports customers with maintenance, rebuilds, service work, and technical analyses, positioned as a specialist service provider in a demanding niche.

Cutting Metal Works i Valdemarsvik AB (2021): CMW is a contract manufacturer specializing in precision chip-cutting metalworking. The company is known for high quality and on-time delivery, serving demanding customers that require complex components with tight tolerances.

Kema Storköksförsäljning AB (2021): Kema designs, manufactures, and sells stainless steel products for professional kitchens under its own brand, such as wine coolers, warming benches, and refrigerated counters. The moat is customization, reputation, and long-standing quality leadership in a demanding customer segment.

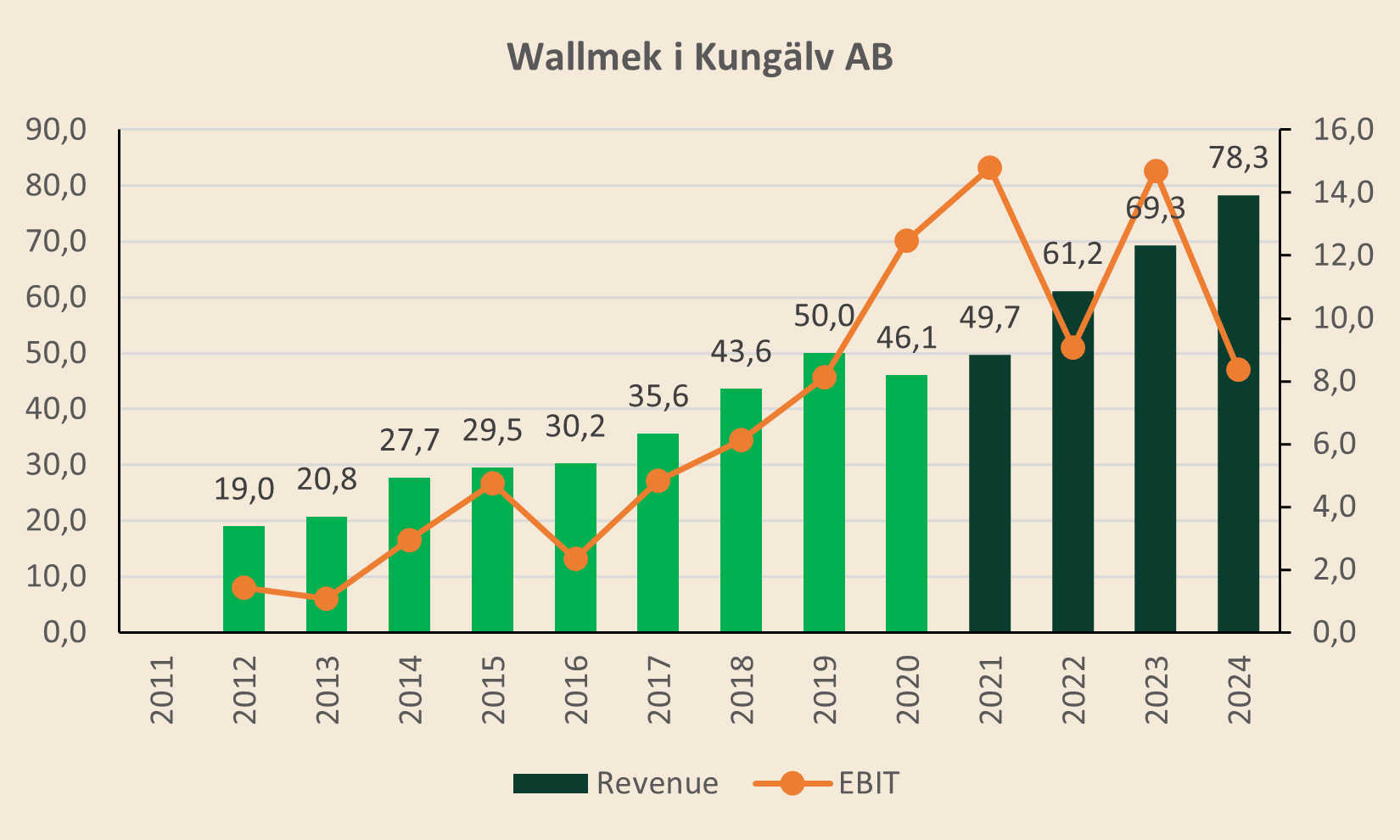

Wallmek i Kungälv AB (2021): Wallmek designs and manufactures special tools used in vehicle repair and dismantling (cars, trucks, trailers, construction machines). Products are sold under its own brand to customers in Europe and North America, improving efficiency and ergonomics in workshops.

UGAB AB / Innoguard AB (2021): INNOGUARD develops, manufactures, and markets laboratory and medical technology products designed to integrate into labs and healthcare environments. Products are sold under its own brand primarily to customers in Scandinavia.

Vicky Teknik AB (2021): Vicky Teknik supplies complete equipment solutions for TMA (Truck Mounted Attenuator) protective vehicles, including its own variable LED signs and associated peripherals. It operates as a turnkey system provider with a strong position in the Nordic market.

Teltek i Örebro AB (2022): Teltek delivers solutions for weighing, process control, and labeling in process industries. It provides tailored systems such as self-developed check scales and IT systems, and also represents equipment like X-ray machines and metal detectors.

Belle Coachworks Holdings Limited (2022): Belle designs and manufactures enclosed vehicle transporters for needs that few others can handle, such as luxury cars, concept cars, and armored vehicles. The differentiation is premium build quality, service level, and superior finish.

Reward Catering Limited (2022): Reward Catering designs and manufactures high-end food trucks and trailers, known for visually striking builds sold primarily to customers in the UK and Ireland, with reach into European and American markets. The model is design-led manufacturing with strong margins and execution-driven growth.

Lundahl Transformers AB (2022): Lundahl develops and manufactures premium transformers for demanding audio applications, used across professional and high-end audio signal chains. The company also delivers custom adaptations and entirely new designs upon request, anchored in a globally respected specialist brand.

Stanwell Group Ltd. (2023): Stanwell develops and sells dispensers, pumps, and liquid handling systems, primarily serving beverage dispense applications. Its products are widely installed across UK pubs, with customer loyalty built on reliability, consistent service, and specialist know-how.

Schill Reglerteknik AB (2023): Schill develops advanced measuring equipment for dynamic and static alignment of weapon systems, mainly used on naval vessels (and some land platforms). The equipment enables fast and precise alignment to maximize firing accuracy.

Surge Protection Devices Ltd. (2023): Surge Protection provides surge protection solutions across the British Isles, serving sectors such as public buildings, defense, airports, and museums. The business combines high-quality products with tailored consultation, driving long-term customer relationships.

Nubis Solutions Ltd. (2024): Nubis designs custom enclosures used in high-intensity data center environments. Its solutions help customers improve server efficiency and lifespan while reducing energy use and carbon footprint compared with alternative setups.

Avelair Ltd. (2024): Avelair designs and manufactures energy-efficient screw compressors and provides complete compressed-air solutions, from system design and installation to servicing and maintenance. The offering includes fixed/variable speed compressors, air treatment systems, and customized packages.

UK Lanyard Makers Ltd. (2024): UKLM manufactures custom lanyards used in operationally critical settings such as large events, trade shows, and product launches. Customers choose the company for design quality, delivery reliability, and flexibility in execution.

Midland Special Fasteners Ltd. (2025): Midland Special Fasteners supplies special fasteners and machined parts where unique specifications and quality cannot be compromised—serving extreme requirements ranging from supercars to aerospace and defense-related applications. It fulfills demand via in-house manufacturing and global sourcing, supported by deep industry expertise and a loyal export customer base

Awarded 2U Ltd. (2025): Awarded 2U provides corporate customers with custom-made awards and manages the full workflow in-house, from design through production and finishing. Its success is driven by creativity, reliability, and strong customer-centric execution.

Merridale Ltd. (2025): Merridale supplies, installs, and services commercial fueling equipment, from single pumps to fully turnkey depot systems. It also offers fuel management systems, tank gauges, and associated equipment, with thousands of installed sites generating long-term service and upgrade opportunities.

Thermasolutions International Ltd. (2025): Thermasolutions designs and manufactures refrigeration blind systems that reduce energy usage in supermarkets and hospitality settings. It serves both UK and international customers, from small outlets to major global retailers.

Edurus Gravstenar AB (2025): Edurus is the Swedish market leader in headstones, stone figurines, and second-name engraving, selling mainly through funeral homes (and some direct-to-consumer). It operates in a conservative, stable market where reliability, quality, and operational efficiency matter.

MITAB i Forsbacka AB (2025): Mitab supplies cremation furnaces and associated equipment (coffin handling, ash handling, flue gas cooling, etc.) and supports customers end-to-end. From planning and manufacturing to installation and service. The company is a technical and market leader in the Nordic region.

Norlin Polymers (UK) Ltd. (2025): Norlin compounds technical polymers tailored to each customer’s needs, primarily for medical device and pharmaceutical applications across Europe. Its products are bespoke and aligned with regulatory requirements, manufactured through a highly automated continuous heat extrusion process.

Birkett Bogmats Ltd. (2025): Birkett Bogmats specializes in supplying hardwood timber bog mats used for ground protection and temporary access. From its UK depot it serves construction, civil engineering, plant hire, and energy projects, with a reputation built on reliability and consistent product quality.

HT Servo Ltd. (2025): HT Servo supplies high-precision motion control components and systems, with emphasis on direct drive technology. Customers include leading UK aerospace and defense companies, relying on the firm’s technical expertise and service mindset for reliable servo solutions.

5.2. Portfolio Evolution: Geography and Age-at-acquisition

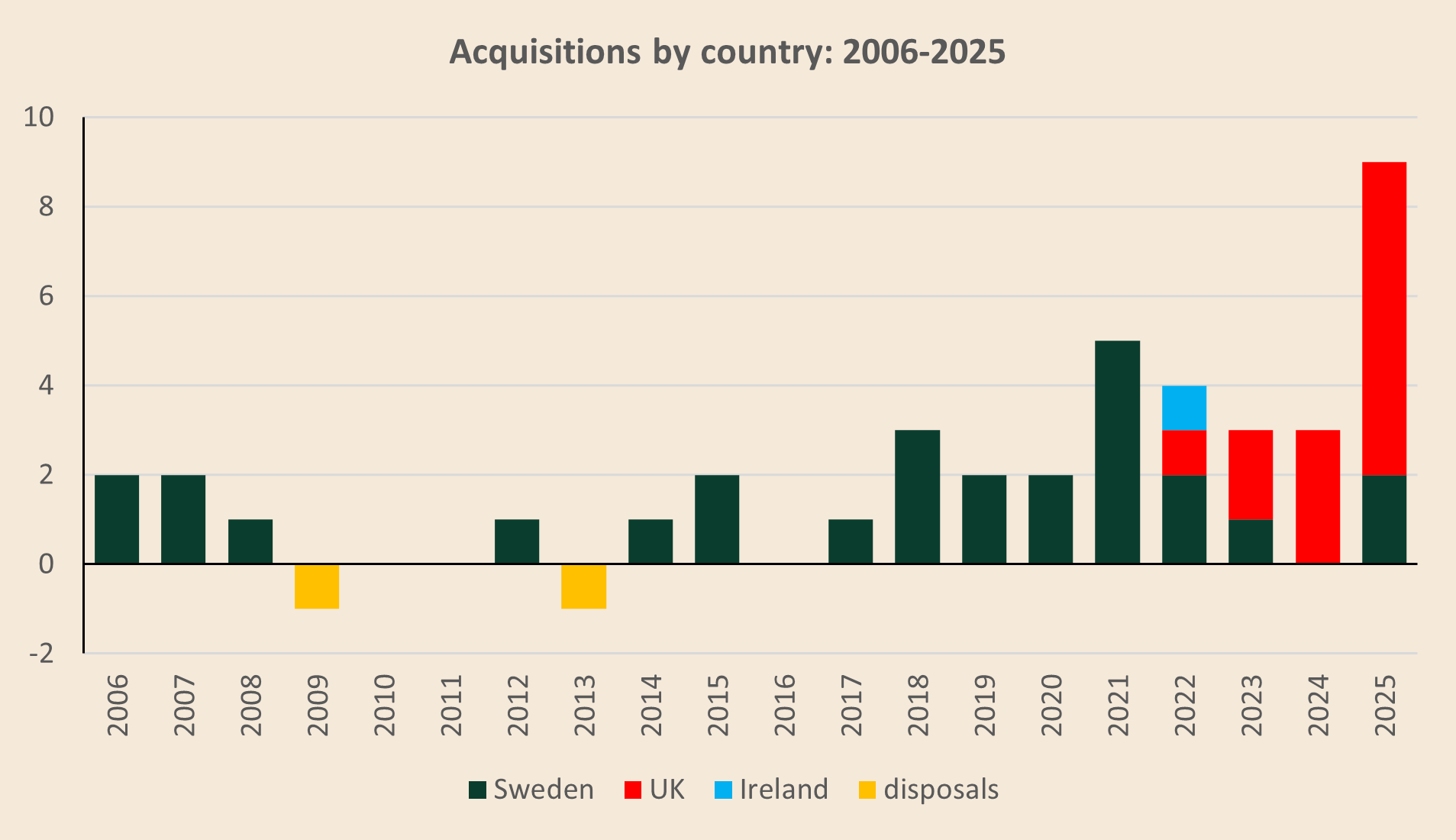

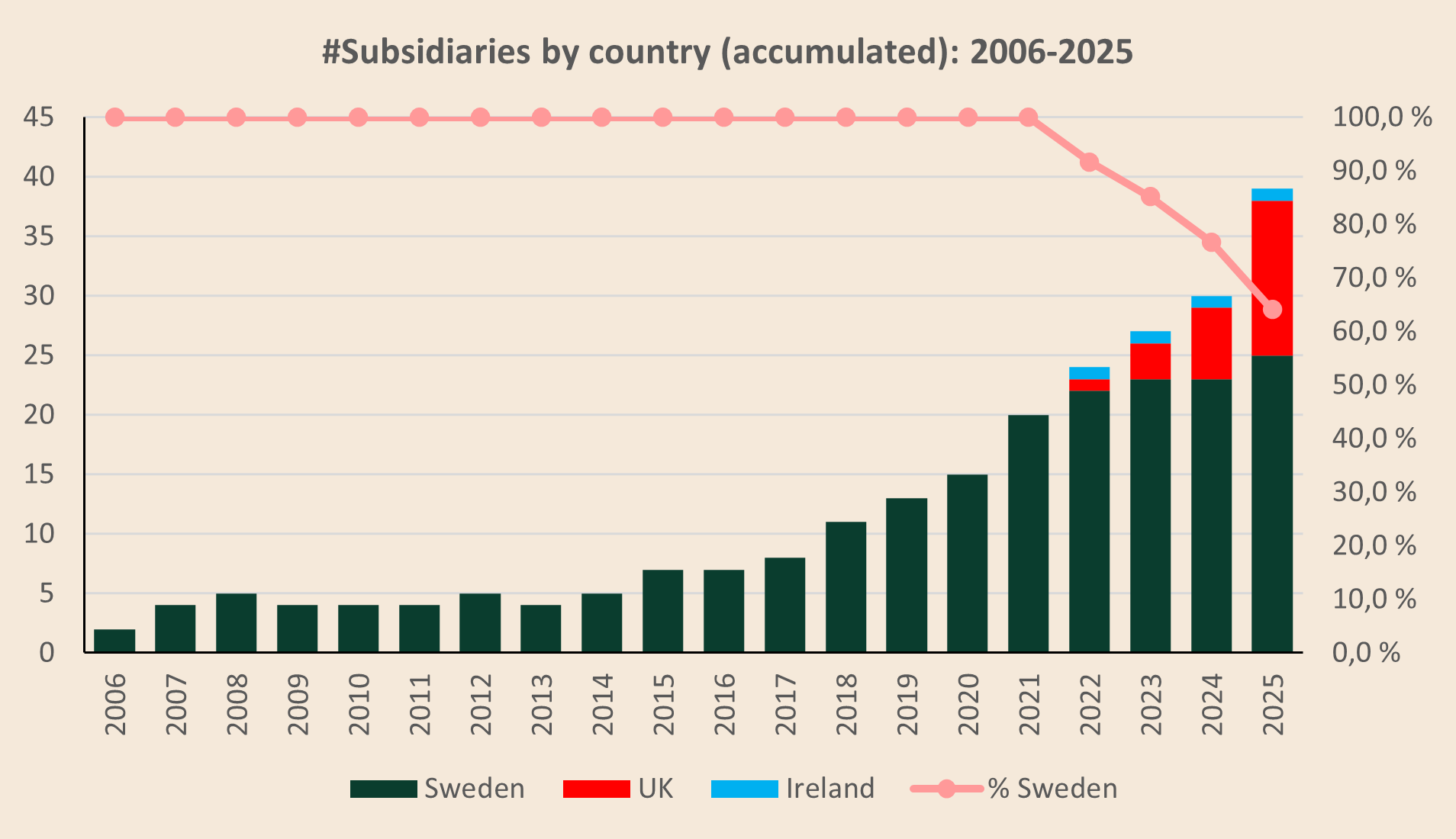

The following chart summarizes acquisitions by geographic footprint. It highlights clearly that Teqnion began its “internationalization” with acquisitions outside its home market, Sweden, in 2022. Over the last four years, Teqnion acquired 19 subsidiaries (vs. 22 from 2006–2021). Of those 19, only five were in Sweden, one in Ireland, and 13 in the UK In other words, about 74% of acquisitions over the last four years were made outside Sweden.

The next chart shows the same picture, but on a cumulative basis (also reflecting the two disposals). One point stands out. In the Q3 2024 earnings call, management said the UK and Ireland operations together accounted for roughly half of group profit in that quarter, even though about ~76% of subsidiaries were still Swedish at the time. That suggests the acquisitions abroad have, so far, been (a) larger and (b) more profitable.

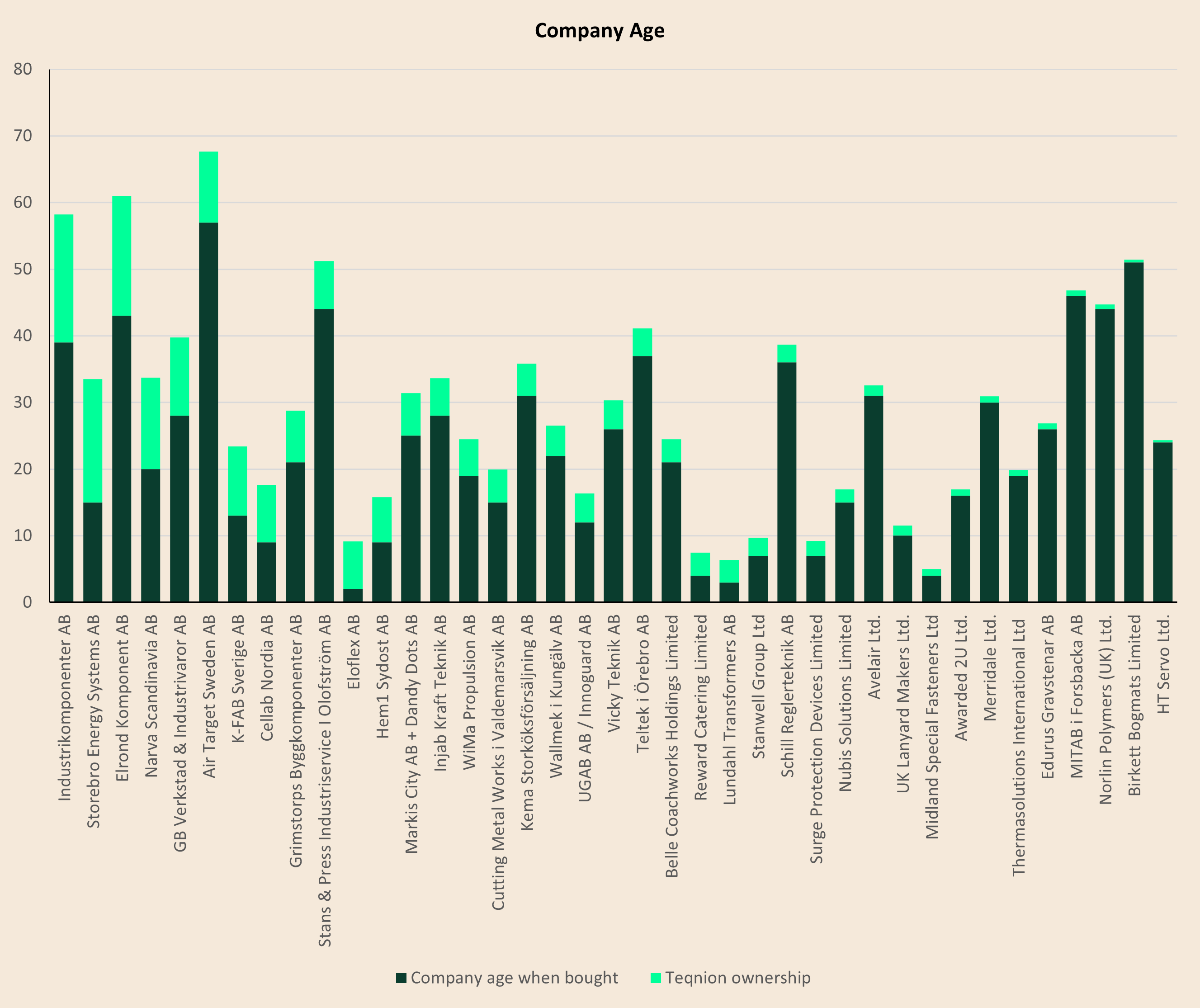

The following chart shows that Teqnion typically buys mature, long-established businesses (acquisitions are sorted chronologically). The average age at acquisition is ~23 years, although there is meaningful dispersion on both ends.

Notably, the younger outliers cluster in 2022 and 2023, when Teqnion acquired several companies with shorter operating histories. Since then, the pattern shifts back toward older targets, with a clear move higher in age-at-acquisition, consistent with the tightened M&A strategy and management’s stated intent to avoid “startup-like” situations in favor of businesses with a longer, proven track record.

Overall, it supports the narrative that the quality bar has moved up and that Teqnion is increasingly buying companies with more operating history rather than relying on short-track-record exceptions (as discussed above).

5.3. Case Studies

The next question is straightforward: how do Teqnion’s acquisitions perform before and after they are acquired? In a decentralized model, the key capability isn’t “integration” in the classic corporate sense. It’s making sure each subsidiary has the right leadership, the right incentives, and the right operating discipline in order to remain autonomous while still being held accountable.

Chapter 3 might give the impression that Teqnion is struggling across most subsidiaries. That’s not the case, as the analysis below shows.

I split the case studies into two buckets. First, problem cases. Second, selected positive examples, where the goal is to show what the model looks like when it works over many years.

For the Swedish subsidiaries, the last 9–10 separate financial statements can be accessed on hitta.se for free. The UK acquisitions come with a disclosure limitation: the income statement isn’t disclosed. That’s why this chapter focuses on the Swedish businesses.

5.3.1. The Problem Cases

Problem cases matter not because any acquisition-led business avoids mistakes—none do—but because they show whether the holding company learns from them and upgrades its system. As discussed above, Teqnion’s struggling bucket simply became too large.

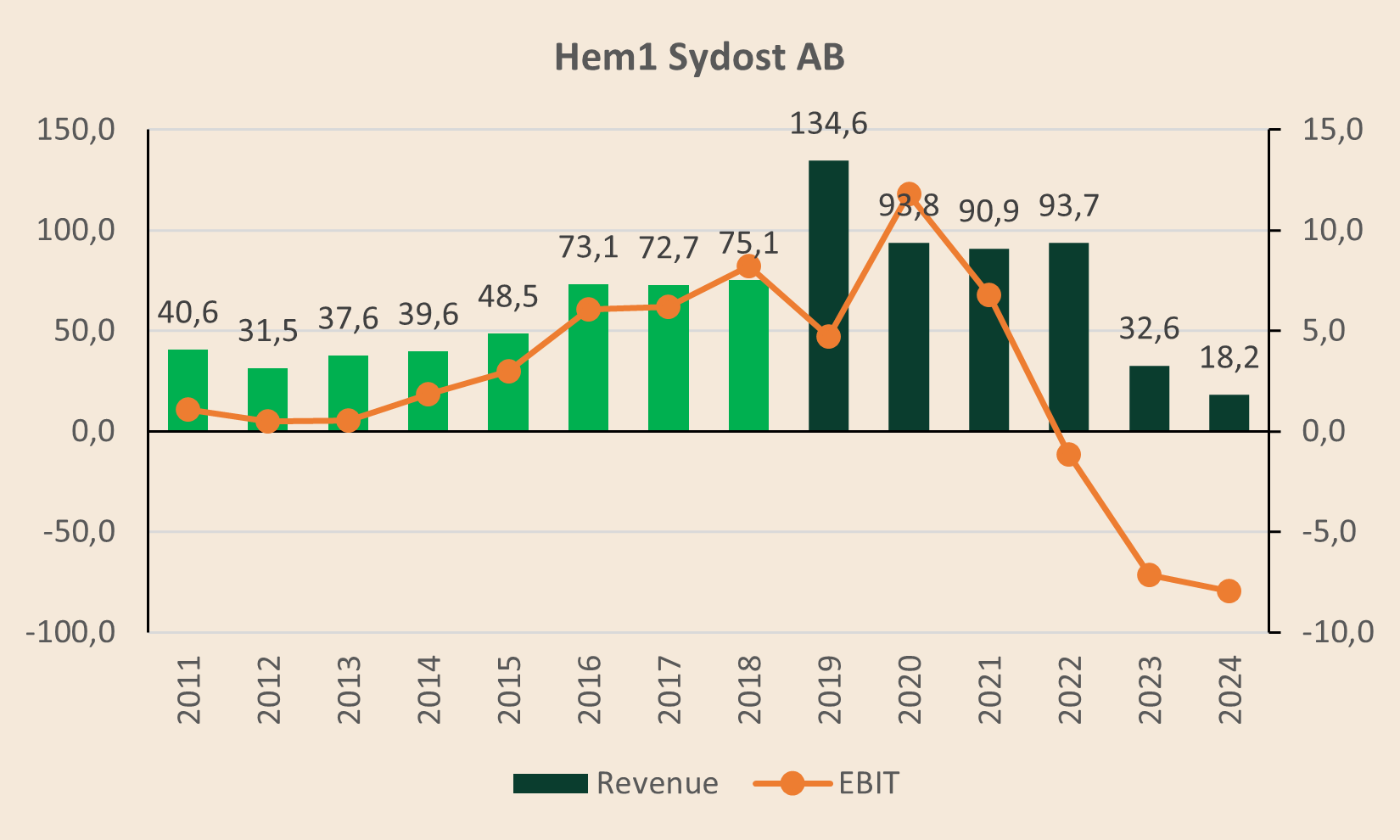

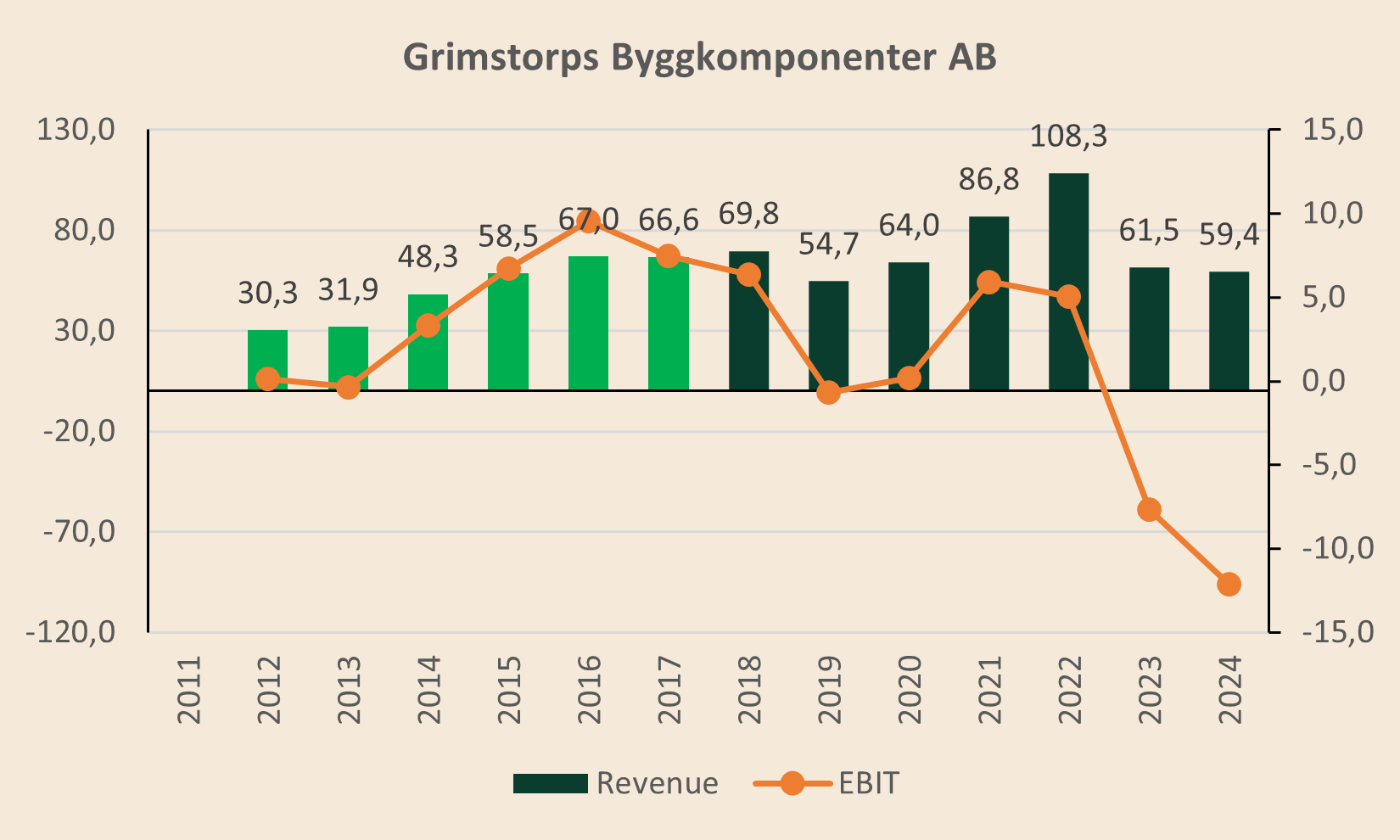

Housing-exposed subsidiaries (Hem1 and Grimstorp):

Management’s framing of housing is instructive. They acknowledge severe volume pressure, but also emphasize that housing has historically been a small part of group turnover. The implication is that housing can meaningfully drag results in a downturn, but it shouldn’t define Teqnion’s through-cycle earnings power.

“We’ve had some people wondering about our exposure to the construction or housing market, which, as you know, we have 2 companies, Hem1 and Grimstorp, that are exposed to that. Historically, there have been less than 10% of the turnover. And I think that Hem1 has sold close to 0 houses for the last quarter or two.” (Daniel Zhang, CXO and Co-CEO, Earnings Call 2022 Q4)

Hem1 Sydost AB and Grimstorps Byggkomponenter AB are good examples of why Teqnion has become more cautious with housing-exposed, cyclical businesses. Both companies compounded revenue and produced solid profitability for many years. Eventually the housing cycle turned and the economics broke sharply as interest rates rose.

Hem1 grew from ~SEK 41 million in revenue in 2011 to a peak of ~SEK 135 million in 2019. It then stayed around ~SEK 90–94 million in 2020–2022, before collapsing to ~SEK 33 million in 2023 and ~SEK 18 million in 2024. Over the same period, EBIT swung from healthy profits in 2016–2021 to losses in 2023–2024. It’s a classic operating leverage effect once volumes fall below the fixed-cost base.

(In the charts that follow, the light green bars represent the period before Teqnion acquired the company, while the dark green bars start in the acquisition year and reflect the period in which the business is part of the Teqnion group.)

Grimstorps shows the same pattern. Revenue climbed steadily to ~SEK 67–70 million in 2016–2018, then accelerated to ~SEK 108 million in 2022, before dropping back to ~SEK 62 million in 2023 and ~SEK 59 million in 2024. Profitability followed the cycle even more brutally, moving from high-single-digit EBIT margins in the good years to deep losses once demand weakened.

In 2025 management commented that both businesses do see a positive trend.

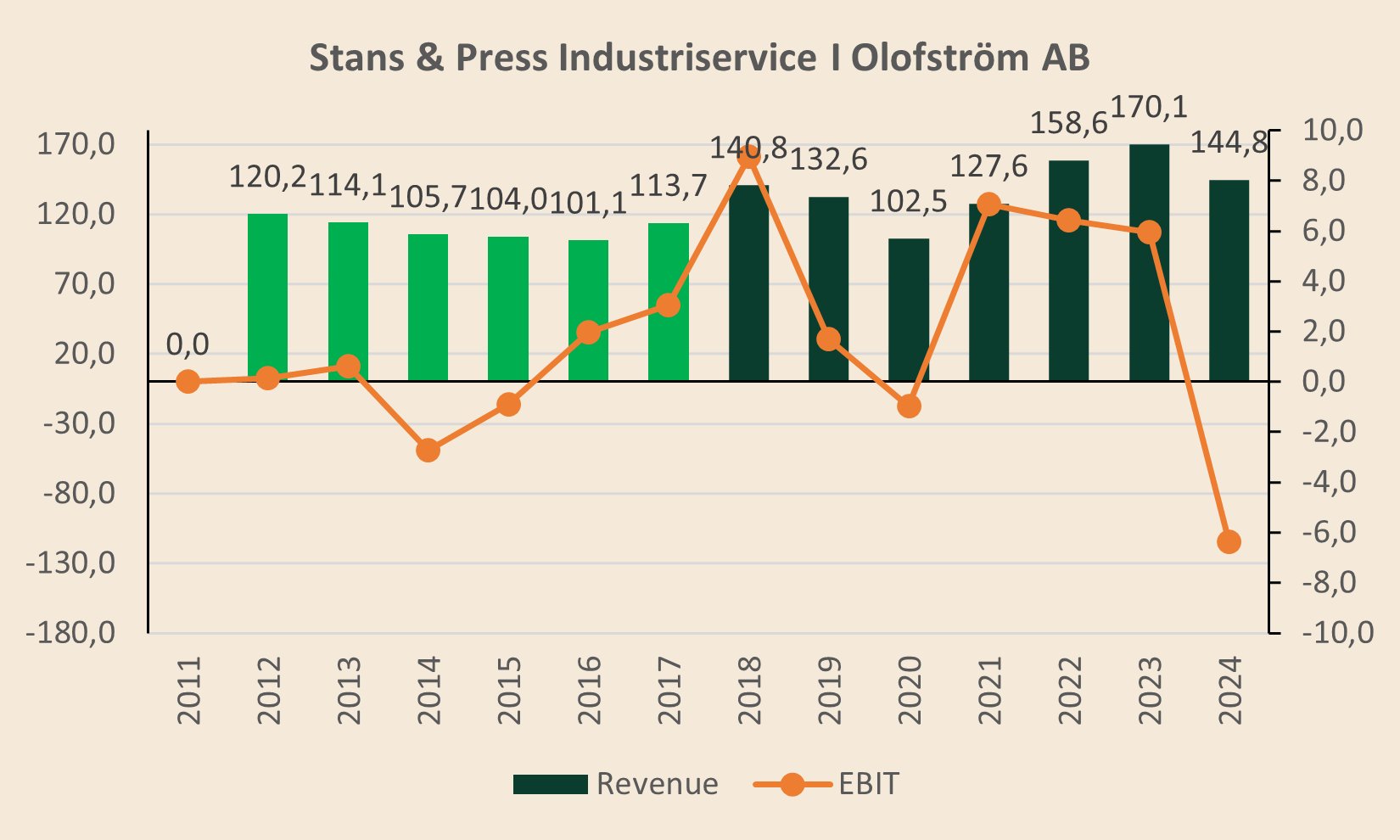

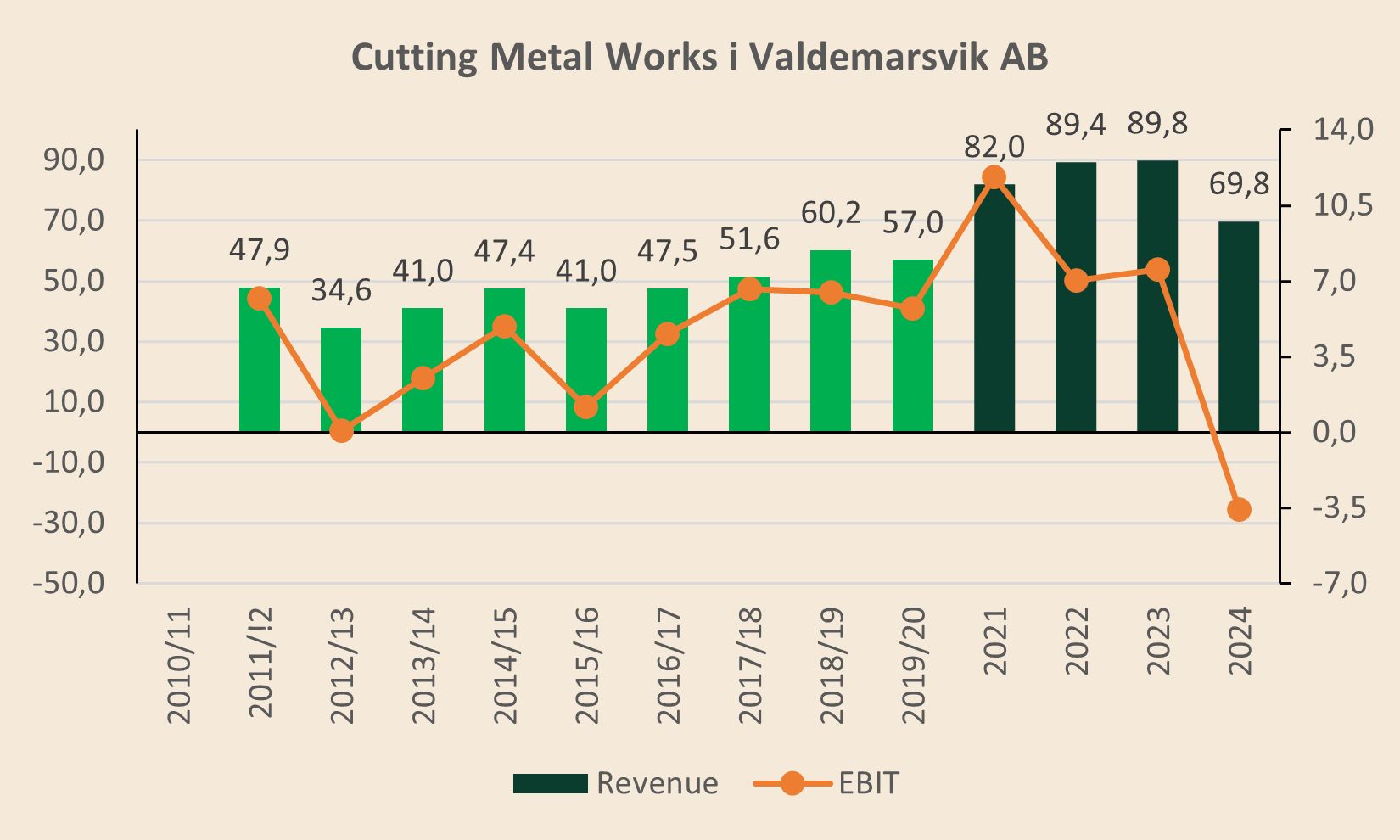

Contract manufacturing (Stans & Press and CMW):

Contract manufacturing often comes with limited margin upside because customers are skilled at pressing prices. But it’s not a universal rule. It depends on the industry. Just think of TSMC, the world’s largest chip contract manufacturer, with EBITDA margins of ~65%.

In Teqnion’s case, Stans & Press and Cutting Metal Works illustrate the structural challenge of many contract manufacturing businesses: you can run a highly competent operation for years, grow revenue, and still end up with fragile economics once volumes weaken because pricing power is limited and the cost base is structurally fixed.

Stans & Press Industriservice shows a long stretch of stable-to-growing revenue, but profitability is clearly cycle-sensitive. After strong years around the acquisition period, EBIT compresses quickly when demand softens, culminating in a sharp loss in 2024 despite still meaningful revenue.

Cutting Metal Works shows a similar pattern: revenue scaled steadily through 2021–2023, EBIT peaked during the up-cycle, and then fell into negative territory in 2024.

The takeaway isn’t that these are “bad businesses” per se—it’s that the model is structurally margin-capped and macro-exposed. That’s exactly why Teqnion has been explicit about deprioritizing typical contract manufacturers in its updated acquisition strategy.

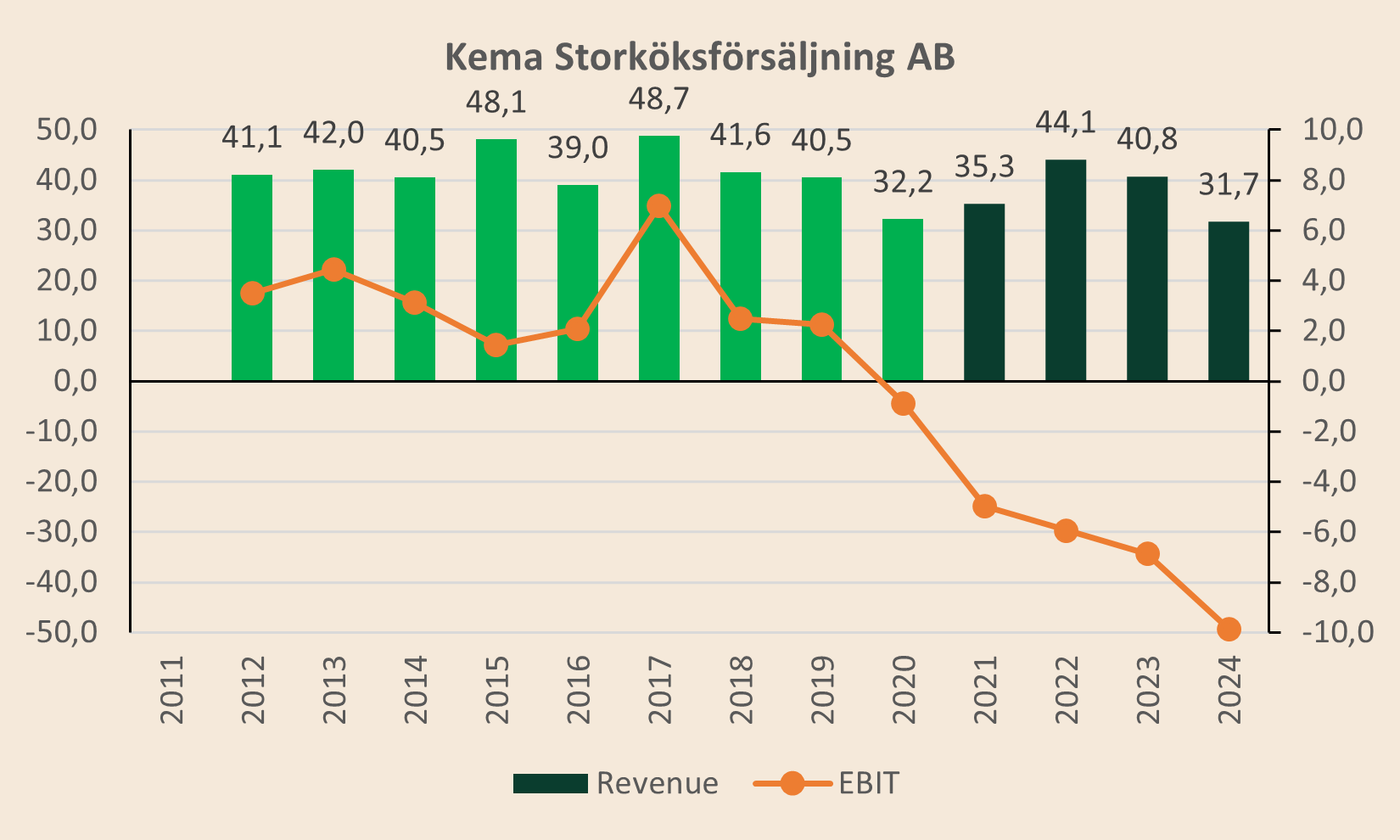

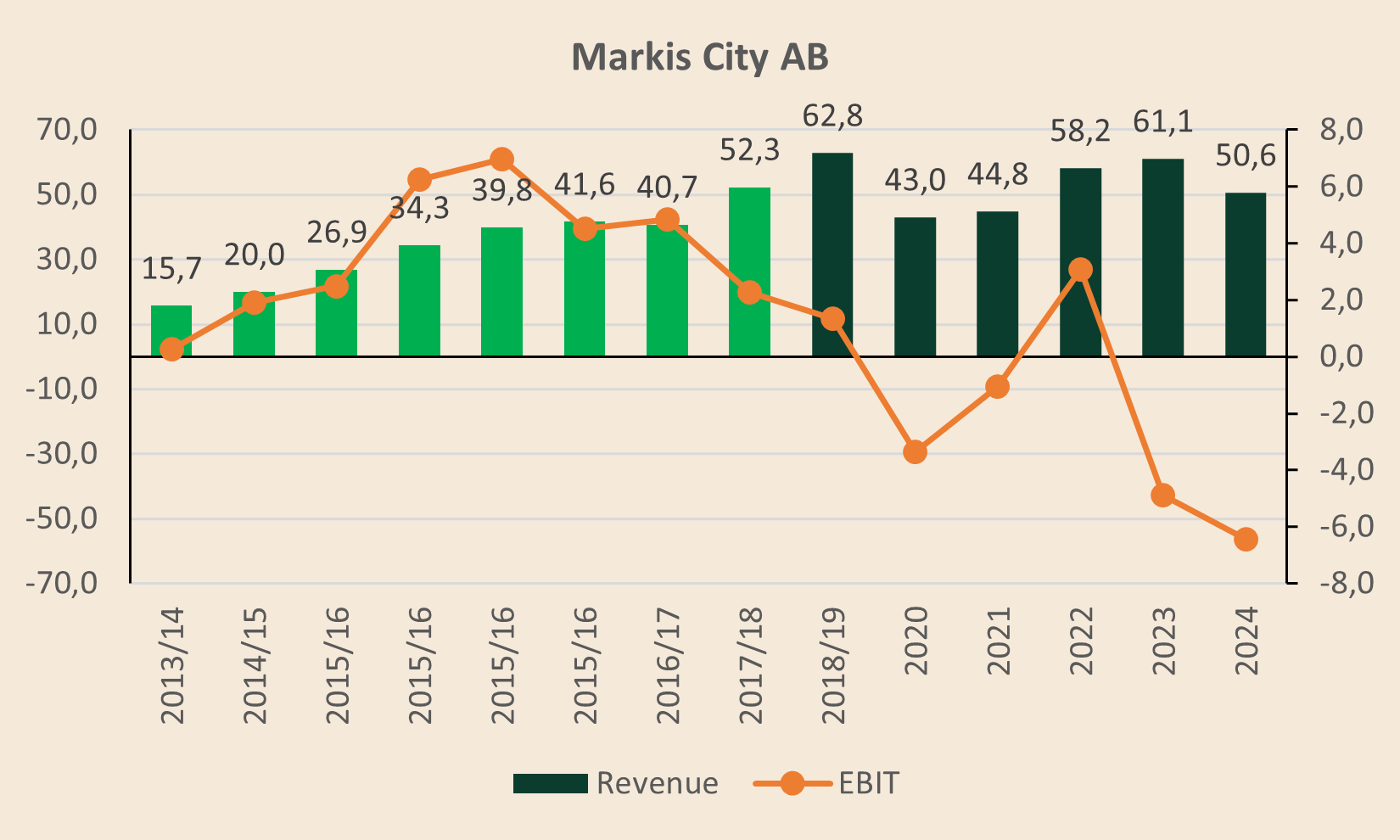

Other struggling businesses (Kema and Markis City):

Kema and Markis City are two more examples where the issue is an inability to protect profitability once conditions turned tougher. Kema’s revenue has been relatively stable in the ~SEK 30–45 million range for more than a decade, yet earnings have deteriorated step by step since 2019/2020. What used to be consistently positive EBIT has turned into persistent losses, culminating in a deeply negative result in 2024.

Markis City shows a similar “profits evaporate faster than revenue” dynamic: revenues grew strongly into 2019, but EBIT swung sharply negative in 2020, briefly recovered in 2022, and then deteriorated again into sizable losses in 2023–2024 despite still meaningful revenue levels.

After looking at the weakest performers, let’s now turn to the positive side.

5.3.2. The Positive Examples

Positive examples matter because they show what Teqnion can look like when the portfolio is dominated by the right kinds of businesses. These are subsidiaries that require minimal intervention from HQ, convert earnings into cash, and hold up over time. They’re also the best proof that decentralization can work.

“Maybe to just point out what we’re trying to do is that we continuously try to just improve the companies that we have within the group. If we do it correctly with small changes throughout the years, we’re going to sooner or later have really, really good cash-generating units that we now have from companies that we owned for a very long time. Those companies, of course, generate more in one year than we paid them when we bought them. That’s the way to do it, of course.” (Johan Steene, CEO, Earnings Call 2024 Q1)

I won’t comment on the charts individually. They speak for themselves.

Across these positive examples, the message is that Teqnion has shown it can buy the right kind of businesses: niche value, real pricing power, strong cash conversion, and leaders who act like owners. Those businesses create the slack that allows Teqnion to deal with the minority of subsidiaries that need intervention, without turning the whole group into a turnaround shop.

In Part 3, we’ll explore whether the mix shift is already showing up in the financials (spoiler alert: yes, they do).

Very interesting. So they try to transition from Lifco to MBB or more precisely something in between?

Very interesting, thank you for your work.