HEICO Corp: A World-Class Compounding Flywheel Riding a Multi-Decade Tailwind

How regulation, customer trust, and disciplined acquisitions built one of the world’s most powerful compounding machines.

New to Slow Compounding?

This Company Snapshot is the short version of the most extensive research project I have published so far.

The full HEICO Deep Dive was published in collaboration with Compounding Quality, one of the best-known investment newsletters on Substack with more than 550.000 readers.

The project is based on months of work, including going through more than 1,200 pages of earnings call transcripts, decades of annual and quarterly financials, aviation aftermarket reports, regulatory documents, PMA industry sources, and even a doctoral thesis on the aircraft parts value chain.

Slow Compounding is built for long-term fundamental investors who want deep, source-driven research on high-quality compounders and serial acquirers.

A small plastic bag containing 1,000 metal bushings can cost an airline $50,000.

That price has little to do with the value of the metal. It reflects the extraordinary market power of OEMs, which can use their control over approved replacement parts to charge exorbitant prices and push through substantial price increases over time.

HEICO has built one of the world’s most successful compounding machines around this simple imbalance.

Since the Mendelson family took control in 1990, revenue has grown from $26 million to approximately $4.5 billion, while net income has increased from $2 million to almost $700 million. Along the way, HEICO has developed thousands of aircraft parts, completed more than 100 acquisitions, and expanded into a decentralized portfolio of highly specialized aerospace and electronics businesses.

Yet the company’s success is not simply the result of selling cheaper parts or acquiring more businesses.

It is the result of a system in which regulatory barriers, customer trust, recurring aftermarket demand, entrepreneurial autonomy, and disciplined capital allocation reinforce one another.

In our Quality Growth framework, HEICO checks almost every box:

🛩️ Recurring demand from aircraft that require maintenance for decades

🧱 High barriers created by regulation, operating history, and customer trust

💰 A strong value proposition based on lower prices and better availability

🔬 A repeatable organic growth engine driven by new product development

🤝 A decentralized acquisition model with a reputation as a permanent home

👨👩👦 Meaningful family ownership and a genuinely long-term culture

📈 A multi-decade runway supported by fleet growth and rising aftermarket demand

This Company Snapshot provides the guided tour: what HEICO does, why its business model is so powerful, how its two operating groups differ, and where the opportunities and risks lie.

The upcoming full 187-page (!) Deep Dive then goes much further—into the aviation ecosystem, aerospace regulation, aircraft maintenance, PMA parts, HEICO’s operating system, acquisition history, financial economics, and valuation.

Please do not click "Download"—it links to the Teqnion Deep Dive. A bug in the Substack editor is currently preventing me from deleting it.

👔 Company Name: HEICO Corporation (“HEICO”)

🔎 ISIN: US4228061093 (Common Stock) and US4228062083 (Class A)

🔧 Business model: Aerospace and electronics serial acquirer

🌍 Geographic exposure: global (~62% U.S. and ~38% international sales across approximately 130 countries)

📈 Stock Price: HEI Common Stock: $339 | HEI.A Class A Common Stock: $253

💰 Market Capitalization: ~$40 billion

👨💼 Number of CEOs since foundation: 2 (one transition — Laurans Mendelson to Eric and Victor Mendelson)

since 1990

👨👩👦 Founder-/Owner-operator: Yes — owner-operated by the Mendelson family

📅 CEO tenure: Since 1990

🥇 Insider ownership: ~21.0% of shares

📊 10Y EPS CAGR: ~16%

🔁 Reinvestment profile: High

💸 Capital intensity: Low — capex-light, but inventory-intensive

🏰 Moat: Regulatory approvals, customer trust, installed-base scale, price and availability, culture

🧨 Main risks: Valuation, acquisition execution, aviation cyclicality, OEM countermeasures

🌳 Slow Compounding fit: Yes – high-quality (niche) serial acquirer

Business Model in a Nutshell: HEICO is a decentralized aerospace and electronics serial acquirer. Its Flight Support Group provides lower-cost aircraft parts, repairs, and distribution services, while its Electronic Technologies Group supplies highly engineered components for aero-space, defense, space, medical, and other de-manding markets. Growth comes from new product development, market-share gains, and disciplined acquisitions of niche businesses that retain signifi-cant operational autonomy.

If you are new to the world of serial acquirers, please check out my fundamental piece before you continue with Heico:

Serial Acquirers: Mastering the Art of acquisition-driven Compounding 🚀

This article lays the groundwork for understanding serial acquirers (as serial acquirers make up ~50 % of my portfolio and this might increase over the future).

A World-Class Compounding Flywheel Riding a Multi-Decade Tailwind

A $50,000 Bag of Bushings

Imagine I handed you a small plastic bag containing 1,000 metal bushings. They are unremarkable to look at—small, round pieces of metal that most people would probably describe as washers or spacers. Unless you happened to know exactly what you were looking at, you might expect to find something similar in a hardware store.

How much do you think the bag costs?

Perhaps $100? Maybe $500? Even $2,000 would sound expensive for a collection of such simple-looking components.

The original equipment manufacturer (OEM) charges $50,000.

The bushings are installed in a CFM56 aircraft engine, one of the most widely used commercial jet engines in the world. Yet the fact that they ultimately end up inside an engine does not make the price any less striking. The bag contains 1,000 small pieces, implying an average price of $50 per bushing. A set of approximately 400 small Teflon washers can also cost $50,000. So can 80 drain plugs. In the latter case, the customer is paying more than $600 for each plug.

At first glance, these prices seem almost impossible to justify. The raw materials are clearly not worth tens of thousands of dollars, and the physical manufacturing process alone cannot explain the difference. Yet the airline is not really paying for the metal, the Teflon, or the plug itself. It is paying for something much more valuable: the right to install that component on an aircraft and continue operating the aircraft safely and legally.

That distinction is the key to understanding HEICO.

A commercial aircraft can be worth well over $100 million, but it generates revenue only while it is flying. If one small component is worn, damaged, or unavailable, the entire aircraft may remain on the ground. Passengers may have to be rebooked, connections can be missed, crews and airport slots may be lost, and the disruption can spread across the airline’s network. The economic damage caused by an aircraft sitting idle for another day can therefore be many times larger than the price of the part needed to return it to service.

The obvious response would be to buy the component somewhere else. After all, there are thousands of industrial manufacturers capable of producing small metal parts. An airline could presumably take the original bushing or washer to one of them, ask for an identical copy, and avoid paying the OEM’s extraordinary price.

In aviation, however, that is not an option.

A part cannot be installed on a commercial aircraft merely because it looks identical, fits into the same space, or is made from the same material. Its design must be approved, it must be manufactured within an accepted quality system, and its origin and production history must be documented and traceable. The manufacturer must also be capable of showing that the part performs its intended function under the demanding conditions in which an aircraft operates.

A machine shop may be perfectly capable of manufacturing an identical-looking component. That does not make the component an approved aircraft part.

When the original aircraft, engine, or component manufacturer is the only approved source, the airline therefore has very little bargaining power. It can purchase the part at the price requested by the OEM, wait for the OEM to deliver it, or keep the aircraft on the ground. This combination of regulatory barriers, limited alternative supply, and the urgent need to return expensive assets to service explains why the price of a small replacement part can bear so little relationship to its raw-material value.

HEICO was built around offering airlines another choice.

The easiest way to understand what the company does is to think about the difference between branded and generic medicine.

When a patient visits a pharmacy, there may be two versions of the same treatment. The first is the branded drug sold by the pharmaceutical company that originally discovered and developed it. That company financed the research, carried the risk that the development program might fail, completed the necessary clinical work, obtained regulatory approval, and established the product in the market. The branded drug therefore reflects not only the cost of manufacturing the tablet itself, but also the original development burden and the value attached to the brand.

Over time, other manufacturers may be permitted to offer an approved generic alternative. The name on the packaging is different, but the generic product must satisfy strict regulatory requirements and provide the same intended therapeutic effect. Because the generic manufacturer did not finance the original discovery process and does not carry the same brand premium, it can normally offer the medicine at a substantially lower price.

The analogy is not perfect in every technical or legal respect, but it captures the economic idea remarkably well.

The OEM aircraft part is the branded drug. A PMA part is the regulated generic alternative.

PMA stands for Parts Manufacturer Approval, an authorization granted by the U.S. Federal Aviation Administration. It allows an independent company to develop and manufacture a new replacement part that can be installed in place of the corresponding OEM component. A PMA part is not second-hand, refurbished, counterfeit, or an unofficial copy. It is a factory-new aviation product manufactured under an FAA-approved design and production system and required to comply with the applicable airworthiness standards.

In other words, HEICO does not simply produce a cheaper piece of metal that happens to fit into the same opening. It performs the engineering work, obtains the regulatory approval, establishes a controlled manufacturing process, and provides the documentation and traceability that allow an airline to install the part with confidence.

That is what turns an apparently ordinary component into a legitimate alternative to the OEM product.

HEICO has become the world’s largest independent provider of such approved alternatives. Historically, the company has introduced new PMA parts at prices approximately 30–40% below those charged by the OEM.

In some cases, the difference becomes considerably larger over time. OEMs have frequently used their strong aftermarket positions to raise replacement-part prices substantially, whereas HEICO has generally followed a much more restrained pricing approach. As the two prices develop along different paths, an initial discount of 30–40% can eventually widen to 50%, 60%, or even approximately 70%.

These savings matter particularly in an industry that has historically struggled to earn attractive returns on capital. Airlines operate with thin margins and have limited control over many of their largest expenses. Fuel prices are largely determined by global markets, labor is operationally essential, aircraft ownership and leasing costs are contractually fixed, and airport and air-traffic-control charges cannot simply be negotiated away. Maintenance, repair, and overhaul (MRO) is therefore one of the relatively few major cost categories in which an airline can actively reduce spending without flying fewer routes, removing seats, or weakening the passenger experience. A dollar saved on maintenance can flow directly into operating profit without the airline having to sell another ticket.

For airlines, those savings are not limited to one unusual purchase. Aircraft maintenance creates frequent and recurring demand. Components wear out, fail, become damaged, reach mandatory inspection limits, or have to be replaced after a specified number of flight hours or takeoffs and landings. A commercial aircraft may remain in service for 20–30 years, while the underlying aircraft or engine platform can continue generating demand for replacement parts and repairs for 35–40 years or longer.

A single approved part may therefore be purchased repeatedly across hundreds or thousands of aircraft over several decades. Once HEICO has completed the engineering and regulatory work, the same product can continue generating revenue whenever another component needs to be replaced.

This is what makes the model so powerful. HEICO is not merely helping an airline save money on one bag of bushings. It is gaining access to a long stream of recurring demand within an installed fleet that continues to fly, wear, and require maintenance year after year.

The $50,000 bag therefore represents much more than an example of excessive aerospace pricing. It illustrates the economic gap on which HEICO was built: a captive OEM aftermarket on one side, and airlines desperate for safe, approved, available, and more affordable alternatives on the other.

HEICO sits between them.

Sharing the Savings

The remarkable feature of HEICO’s model is not only that the company can sell an approved alternative for less than the OEM. It is how much of that difference management has historically chosen to leave with the customer.

Suppose an OEM part costs $100 and HEICO can develop and manufacture an approved alternative at a much lower cost. HEICO could charge $90 or $95. The airline would still save money, and HEICO would retain most of the economic benefit created by the alternative. Given the customer’s limited options and the importance of keeping the aircraft in service, such a strategy might remain profitable for a considerable period.

HEICO has deliberately avoided that approach. Instead, it may offer the part for $60 or $70, creating a saving large enough to matter to the airline and to justify the technical and administrative work required to approve another supplier. This is not an indication that HEICO lacks pricing power. It is a deliberate decision to reinvest part of that pricing power in the customer relationship.

The airline lowers its maintenance costs, while HEICO can still earn an attractive margin because it does not carry the development cost of the entire aircraft, engine, or larger system. Lower prices encourage greater adoption, support higher volumes, and make customers more willing to evaluate additional HEICO products. Those volumes, in turn, allow HEICO to invest further in engineering, product development, inventory, manufacturing, quality control, and distribution. The stronger the platform becomes, the more products it can develop and the more value it can offer to customers.

The approach resembles Nick Sleep’s concept of scale economies shared, most famously associated with Costco. Costco does not retain every benefit created by its purchasing power and operating scale. It returns a meaningful share to its members through lower prices, thereby strengthening customer loyalty and increasing volume. The additional volume improves Costco’s bargaining power and cost position, allowing it to offer even more value and reinforcing the cycle.

HEICO follows a similar principle in a very different industry. As the company’s catalog, engineering base, purchasing power, manufacturing knowledge, customer relationships, and distribution capabilities have expanded, it could have used those advantages primarily to increase prices. Instead, it has preserved a substantial discount to the OEM. Customers save money, HEICO earns attractive returns, and the resulting trust and volume support further product approvals. The savings shared with customers reinforce the scale advantages that made those savings possible.

HEICO also exercises restraint in the amount of market share it pursues. Management has historically been satisfied with an attractive minority position—often around one-third of the market for an individual product—rather than trying to eliminate the original supplier. The OEM can continue supplying most of the volume at a substantially higher price, while HEICO serves the portion of the market willing and able to adopt an alternative.

This creates the possibility of rational coexistence. The airline receives meaningful savings, HEICO earns attractive economics, and the OEM retains most of a profitable aftermarket. An OEM considering an aggressive response must weigh the cost of reducing prices across its much larger installed base against the benefit of winning back the minority share held by HEICO. As long as HEICO does not threaten the entire market, the economics of a price war may be unattractive for the incumbent.

HEICO has reinforced that balance by generally avoiding the most valuable life-limited engine parts, which represent some of the crown jewels of the OEM aftermarket. Its restraint therefore operates in both directions: the company leaves substantial savings with customers and substantial volume with the original supplier. Rather than maximizing the economics of a handful of products, it has created a model that can be repeated across thousands of parts.

The resulting flywheel is straightforward. More approved products create more opportunities for customers to save. Greater savings encourage adoption and deepen the commercial relationship. Higher adoption produces volume, product ideas, operating data, and additional resources for engineering and inventory. Those capabilities allow HEICO to develop more products, which create further savings and strengthen the relationship again.

That is a much more durable proposition than simply selling a cheaper component.

Why Price Alone Is Not Enough

A discount of 30–40% sounds compelling, but aviation customers do not choose parts on price alone. The employee responsible for approving an alternative may generate substantial savings for the airline, yet that individual also bears the perceived professional risk if the product later creates a problem. Choosing the OEM is institutionally easy: it is the incumbent supplier, its part was installed originally, and few people are criticized for remaining with the established source. Choosing an alternative requires someone to make an active decision and accept responsibility for it.

This is why Victor Mendelson, one of HEICO’s current Co-CEOs and the long-time leader of its Electronic Technologies Group, has described it as extremely difficult to convince people to use an alternative part on an airplane. The financial benefit belongs to the airline, while the perceived downside may sit with the engineer, maintenance executive, or procurement professional who approved the switch. A lower price can begin the conversation, but credibility determines whether the sale actually happens.

HEICO has spent more than three decades reducing that perceived risk. It has built specialized engineering and regulatory capabilities, established quality systems across a broad manufacturing network, accumulated extensive operational experience, and developed long-standing relationships with airlines and maintenance organizations. The HEICO Parts Group has shipped more than 90 million parts without a Service Bulletin, Airworthiness Directive, or in-flight shutdown attributed to one of its products.

A new competitor may be able to hire engineers, purchase machinery, and obtain approval for an individual product. It cannot purchase a comparable operating history. Every year of successful performance adds to a record that can only be built over time, and every approved product creates further evidence that HEICO’s processes work beyond a single component.

The partnership with Lufthansa Technik played a decisive role in establishing that credibility. When Lufthansa Technik acquired a minority interest in HEICO’s aircraft-parts operations in 1997, one of the world’s most respected maintenance organizations placed its technical reputation and capital behind the company. Lufthansa could help identify parts that were expensive, difficult to source, or commercially attractive, while also providing operating knowledge and anchor demand once HEICO had completed the development and approval process.

The first HEICO part an airline approves may require considerable analysis, internal discussion, and technical documentation. Once that part has operated successfully, the company is no longer an unknown supplier. The customer has already reviewed HEICO’s quality systems, documentation, engineering capabilities, and support organization. Each subsequent approval can build on the credibility established by the products that came before it.

Catalog breadth magnifies this advantage. An airline may be reluctant to invest time in qualifying a small PMA manufacturer that offers only one or two products and therefore creates limited potential savings. HEICO can offer thousands of opportunities across engines, airframes, hydraulic and pneumatic systems, interiors, avionics, wheels and brakes, electromechanical equipment, and other categories. The technical and administrative effort required to establish the supplier relationship can be spread across a much larger pool of potential savings.

HEICO already serves virtually every major airline. Its remaining organic opportunity is therefore not primarily about adding customer names. It is about expanding the number of products each existing customer is willing to purchase. Every successful part increases confidence in the next one, while every newly approved product expands the portion of the customer’s maintenance spending in which HEICO can participate.

Availability adds another layer to the proposition. A lower-priced part is useful only if it can be delivered when required. When an aircraft is grounded, the economic cost of waiting can quickly exceed the price difference between competing components. HEICO therefore carries meaningful inventory and has built distribution capabilities that allow approved alternatives to be supplied at short notice. In periods of severe supply-chain disruption, immediate availability can become more important than the discount itself. A customer may first approve a HEICO part because the OEM cannot deliver, then continue buying it after the alternative has performed successfully and the higher OEM price becomes difficult to justify.

The moat is therefore not a single patent, approval, factory, or customer contract. It is the accumulated system of regulatory knowledge, engineering capability, quality control, operating history, product breadth, inventory, distribution, customer relationships, and institutional trust. Each element supports the others, and the system becomes progressively harder to reproduce as it grows.

From One Aircraft Part to Approximately 20,000

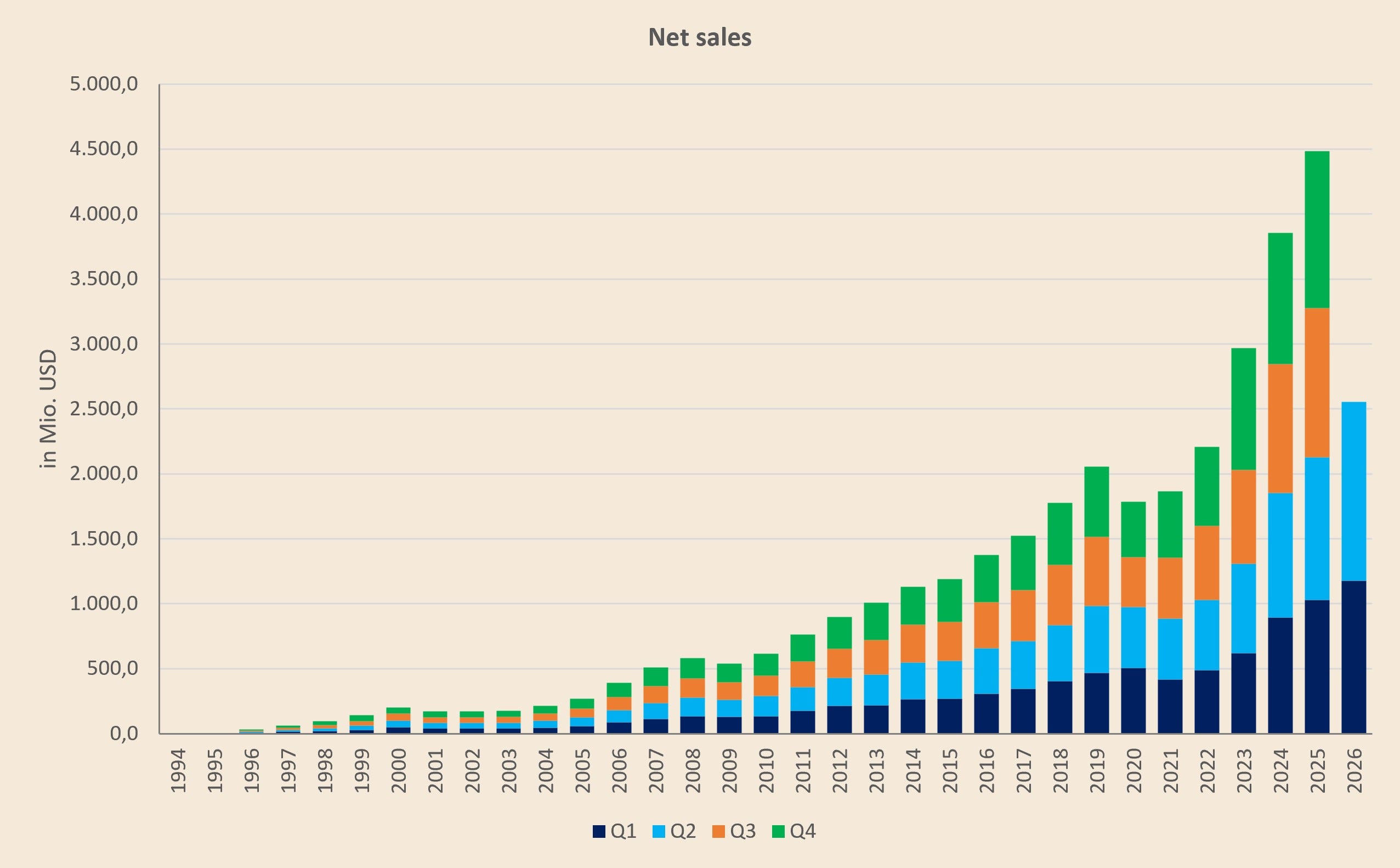

The HEICO recognized by investors today began taking shape when the Mendelson family assumed control in 1990. At the time, the company generated $26.2 million in revenue and $2.0 million in net income. Its aerospace operation was centered on essentially one core PMA product: a replacement combustion chamber used in a Pratt & Whitney aircraft engine.

That product demonstrated that an independent manufacturer could overcome the technical, regulatory, and commercial barriers required to compete with an established aerospace supplier. It did not yet prove that the opportunity could become a scalable business. HEICO still needed to expand its approval capabilities, gain the trust of conservative airline customers, establish repeatable manufacturing processes, hold inventory, and show that it could support products reliably over long periods.

The Mendelsons proceeded gradually. HEICO added further engine components, expanded into additional aircraft systems, developed repair capabilities, and used acquisitions to obtain technical expertise, customer relationships, manufacturing processes, and entry into adjacent product categories. Over time, the portfolio moved beyond its original engine focus into fuel, hydraulic, pneumatic, electromechanical, wheel and brake, airframe, interior, structural, and avionics products.

The acquisition of Wencor in 2023 materially increased the scale of the platform. Before the transaction, HEICO offered approximately 12,000 PMA parts and Wencor roughly 7,000, creating a combined portfolio approaching 20,000 approved products. HEICO now adds approximately 400–550 new PMAs each year and also offers thousands of DER-approved repairs, which allow damaged components to be restored rather than replaced with expensive new OEM products.

The number of products is important, but the process that continually creates them is the more valuable asset. Customers identify components suffering from high prices, poor availability, or an absence of competitive supply. HEICO evaluates the size of the market, the remaining life of the aircraft or engine platform, the technical complexity of the product, the likely customer demand, the incumbent price, and the development and inventory investment required. Promising candidates move through engineering, regulatory approval, manufacturing setup, quality validation, and commercial introduction.

Not every new product becomes important immediately. Airlines may require time to complete their own technical reviews, and adoption can build gradually as the part establishes an operating history. Product cohorts can therefore ramp for several years, while mature products continue generating recurring revenue from the installed fleet. HEICO’s organic growth reflects the layering of many such cohorts: older products continue selling, newer products gain adoption, and hundreds of additional approvals enter the portfolio each year.

This also explains why the opportunity can remain large despite the company’s long history. New aircraft and engine platforms enter service, existing platforms mature and move beyond initial warranties, OEM prices rise, supply problems emerge, technologies change, and customers identify additional components or repairs for which they want another source. The addressable opportunity continually renews itself.

What began with one combustion chamber has consequently become the world’s largest independent portfolio of FAA-approved jet-engine and aircraft-component replacement parts. Yet describing HEICO simply as a PMA company now understates the breadth of the business.

Two Operating Groups, One Economic Logic

HEICO operates through two principal segments. The Flight Support Group, or FSG, is the larger platform and the historical core of the company. It designs and manufactures PMA parts, repairs and overhauls selected aircraft components, distributes proprietary and third-party products, and manufactures specialized aerospace equipment. Depending on the customer’s situation, HEICO may provide a new replacement part, restore the existing component through an approved repair, source a needed OEM product through its distribution network, or combine several of these capabilities.

This broader offering matters because the customer’s underlying problem is not necessarily a desire to buy a PMA part. The customer needs an aircraft or component returned to service safely, quickly, and at a reasonable cost. By supplying parts, repairs, inventory, distribution, and technical support, HEICO can address that problem through several routes rather than forcing every situation into a single product category.

FSG generated approximately 70% of HEICO’s fiscal 2025 revenue and operating income. Its scale, catalog breadth, regulatory capabilities, and direct customer relationships make it the crown jewel of the company and the clearest expression of the HEICO model.

The Electronic Technologies Group, or ETG, receives less attention but provides a second growth engine. Its companies manufacture highly engineered components and subsystems used in aircraft, defense equipment, missiles, satellites, medical devices, telecommunications infrastructure, and other technically demanding applications. The portfolio includes products such as power supplies, antennas, microwave components, shielding, sensors, connectors, and other specialized devices that are often small relative to the value of the larger system in which they operate.

ETG reaches attractive economics through a somewhat different mechanism. FSG frequently challenges a highly priced incumbent by creating an approved alternative. ETG businesses often become the incumbent by having their component designed into a customer’s product or platform. Once the product has been selected, tested, qualified, documented, and incorporated into the larger system, replacing it may require redesign, additional testing, new documentation, customer approval, and regulatory or technical requalification. The possible cost saving from changing suppliers is often insignificant compared with the expense, delay, and risk involved in replacing a product that already performs reliably.

The two groups therefore appear diverse at the product level but share a common economic logic. HEICO focuses on small yet important products used in much larger systems, where the cost of failure is high and the component’s selling price is modest relative to the value of the aircraft, engine, missile, satellite, medical device, or other platform. Customers care about reliability, availability, documentation, qualification, and technical support far more than the cost of the underlying raw material.

This is why Laurans Mendelson did not primarily describe HEICO as an aerospace or electronics company. He regarded it as a vehicle for generating and reinvesting cash. The industries and products provide the setting, but the underlying objective is consistent: acquire or develop businesses with strong margins, durable demand, defensible customer positions, and opportunities to reinvest capital at attractive returns.

The Acquisition Flywheel

Organic product development forms one side of HEICO’s compounding model. Acquisitions form the other.

The company generally seeks specialized businesses with strong customer relationships, capable management teams, attractive margins, defensible niche positions, and opportunities for continued growth. Many targets are founder- or family-owned companies that have developed valuable products and technical expertise but remain too small to attract widespread attention.

After an acquisition, HEICO typically preserves the identity, management, employees, and operating autonomy of the business. Decisions about customers, products, engineering, manufacturing, and personnel remain largely with the people closest to the operation. Headquarters focuses on capital allocation, financial discipline, incentives, acquisitions, and the balance sheet rather than attempting to run dozens of specialized companies through a centralized corporate bureaucracy.

Sellers may retain a minority interest and continue managing the business. This allows an entrepreneur to achieve personal liquidity and diversify wealth without necessarily abandoning the company, employees, and customer relationships built over many years. The seller can continue participating in future value creation while gaining access to HEICO’s capital, acquisition expertise, public listing, and broader network.

HEICO also presents itself as a permanent owner. It does not generally acquire businesses with the intention of improving reported metrics for a few years and selling them to the next financial buyer. For founders who care about the future of their employees, the independence of the business, and the preservation of its identity, that distinction can matter as much as the highest immediate purchase price.

The seller proposition has become more credible with time. A founder considering HEICO can speak with entrepreneurs who sold their businesses many years earlier and ask whether management honored its promises. Each successful acquisition therefore becomes a reference for the next one. The larger and longer the track record becomes, the harder it is for a new buyer to reproduce.

This can generate proprietary or less competitive deal flow and allow HEICO to acquire businesses that might not choose a conventional strategic buyer or private equity firm. It does not eliminate competition, and HEICO will not win every attractive transaction, particularly when another buyer is prepared to pay a price that management considers excessive. However, it expands the factors on which the company can compete beyond valuation alone.

The parallels with the customer proposition are striking. HEICO does not attempt to capture every available dollar from airlines, and it does not attempt to extract every degree of control from acquired entrepreneurs. In both cases, management willingly leaves meaningful economics or autonomy with the other party because the resulting relationship may endure for decades.

HEICO’s long-standing refusal to maximize each individual transaction strengthens confidence in both components of its growth engine. Customers continue bringing the company expensive or difficult-to-source products they would like HEICO to develop. Entrepreneurs continue considering HEICO as a permanent home for the businesses they created. The acquisition pipeline and the organic product pipeline are therefore both supported by a reputation accumulated over many years.

This is particularly valuable because there is frequent, recurring demand for HEICO’s products. Aircraft continue flying, components continue wearing, maintenance events continue occurring, and customers repeatedly return for replacement parts, repairs, distribution, and technical support. Preserving the relationship is more valuable than maximizing the margin on one order. In a business built around repeated transactions over long product lives, retention is not merely a commercial metric. It is central to the economics.

Longevity is the cornerstone of compounding.

An Internal Flywheel Riding a Multi-Decade Tailwind

HEICO’s internal compounding system operates within one of the world’s most durable secular growth markets. Commercial air travel has expanded over many decades as populations, incomes, tourism, trade, and international connectivity have increased. The path has never been smooth. Recessions, terrorist attacks, wars, fuel-price shocks, and the COVID-19 pandemic have all caused severe temporary disruptions. Yet passenger demand has repeatedly recovered and resumed its long-term growth.

The current environment offers additional support to the aftermarket. Aircraft manufacturers and their suppliers have struggled to deliver enough new aircraft, forcing airlines to keep older models in service for longer than originally planned. Older aircraft generally require more maintenance, while the high utilization of the available fleet accelerates the accumulation of flight hours and cycles that trigger inspections, repairs, and replacement demand. Long OEM lead times also increase the value of an approved second source capable of delivering a part immediately.

These near-term conditions are favorable, but the longer-term installed-base development is more important. The global commercial fleet is expected to expand substantially over the coming decades as air travel grows, particularly in emerging markets where trips per capita remain far below developed-market levels. Each aircraft entering service creates a potential stream of parts, repairs, inspections, and inventory demand extending far beyond the original delivery.

New aircraft initially remain more closely tied to OEM warranties, service agreements, and approved maintenance networks. As those aircraft age, warranties expire, maintenance events become more frequent, and operators become more motivated to reduce costs. The addressable market for independent aftermarket suppliers therefore grows not only as more aircraft enter service but also as each generation of aircraft matures.

HEICO benefits from both time horizons. In the near term, delayed deliveries, aging fleets, high utilization, and parts shortages support demand for repairs and readily available alternatives. Over the long term, a larger installed fleet creates a broader base of aircraft and systems requiring maintenance for decades.

The financial record reflects the combination of these industry tailwinds with HEICO’s internal execution. Between fiscal 1990 and fiscal 2025, revenue increased from $26.2 million to approximately $4.49 billion, representing annual growth of roughly 16%. Net income attributable to HEICO rose from $2.0 million to approximately $690 million, equivalent to about 18% annually.

Growth has come from a combination of new products, increased adoption of existing products, market-share gains, acquisitions, and entry into adjacent niches. Importantly, HEICO has generally achieved this without relying on aggressive price increases or substantial equity issuance. Acquisitions have predominantly been financed with internally generated cash and debt, resulting in relatively limited dilution for long-term shareholders.

The business is also modestly capital-intensive in the conventional sense. Physical capital expenditure represented approximately 1.6% of fiscal 2025 revenue. HEICO does, however, commit meaningful capital to inventory because immediate availability is a central part of the customer proposition. It also expenses research and development through the income statement, meaning current earnings already bear the cost of product-development efforts that may generate revenue for many years.

The Mendelson family’s significant ownership reinforces the long-term orientation. Its financial outcome is primarily linked to the value of HEICO’s shares rather than the maximization of executive compensation or short-term transaction volume. Subsidiary managers and employees also participate through retained minority interests, performance incentives, and ownership of HEICO shares.

The result is a rare combination of organic product development, recurring aftermarket demand, programmatic acquisitions, attractive margins, modest physical capital requirements, aligned ownership, and a secular growth runway extending over multiple decades. Few businesses possess even several of these characteristics. HEICO has assembled them within one compounding system.

Understanding HEICO Requires Understanding the Industry

This Deep Dive is intentionally structured differently from a conventional company report. When I began researching HEICO, I did not yet have a deep understanding of the aerospace industry, and I quickly realized that the company could not be properly analyzed in isolation. Understanding why HEICO’s products are valuable—and why its competitive position is so difficult to replicate—first requires an understanding of the broader aviation industry, the aerospace value chain, aircraft maintenance, and the regulatory system governing every part installed on an aircraft.

I therefore expanded the research well beyond HEICO itself. The result is not only a company Deep Dive, but also a broader reference guide to the aerospace industry that can be revisited when analyzing other companies operating across aircraft manufacturing, aerospace supply, maintenance, repair, distribution, and the aftermarket.

HEICO itself is therefore not examined in detail until Part III. The first two parts establish the industrial, economic, and regulatory system in which the company operates.

Part I (published on July 19) begins with the broader aviation industry. It examines long-term passenger growth, the current aircraft shortage, production backlogs, delayed retirements, fleet utilization, and the expected expansion of the global installed fleet. It then moves through the aerospace value chain, explaining how a modern aircraft is assembled from highly specialized systems and components and why aircraft and engine manufacturers rely on a deep network of suppliers. Finally, it establishes the regulatory framework governing design, production, maintenance, and continuing airworthiness.

Part II turns to the aircraft aftermarket. It explains why maintenance demand exists, how maintenance, repair, and overhaul developed into a global industry, how aircraft checks and component repairs work, and where control and bargaining power sit across the value chain. It then examines PMA parts and DER-approved repairs in detail, including the regulatory approval routes, the airline economics supporting adoption, the price and availability proposition, and the practical barriers that still limit penetration.

Only after that foundation has been established does Part III turn directly to HEICO. It covers the company’s development under the Mendelson family, the creation of the modern Flight Support Group, the customer proposition, the acquisition of Wencor, HEICO’s current market position, and the remaining organic runway.

Part IV examines the Electronic Technologies Group and the HEICO Operating System, including ownership, incentives, decentralization, acquisition criteria, and the reasons entrepreneurs may choose HEICO over competing buyers.

Part V brings the analysis together through HEICO’s acquisition history, financial development, capital intensity, competitive advantages, risks, and valuation.

Parts I and II are therefore not an extended detour before reaching the company. They are necessary to understand why the company exists. Without a working knowledge of aircraft lifecycles, certification, continuing airworthiness, maintenance economics, OEM aftermarket power, airline incentives, and the PMA approval process, it is difficult to appreciate why a small bag of apparently ordinary components can cost $50,000—or why offering the airline an approved alternative for substantially less can become the foundation of an extraordinary business.

Most company reports begin with HEICO’s revenue, margins, acquisitions, and valuation multiples. Those figures describe what the company has achieved, but they do not fully explain why it has been possible.

To my knowledge, no other publicly available HEICO Deep Dive develops the underlying aerospace ecosystem in comparable depth.

That context ultimately reveals what makes HEICO unusual. It is not simply an aerospace supplier, a PMA manufacturer, an electronics group, or a serial acquirer. It is a carefully constructed system that converts customer cost pressure, regulatory complexity, recurring maintenance demand, technical credibility, entrepreneurial autonomy, and disciplined capital allocation into a flywheel capable of compounding over decades.

Stay tuned for Part 1 of the upcoming deep-dive!

Before reading this snapshot, I had virtually no knowledge of the airline industry. Now, I'm eager to learn more and dig into the full deep dive. I'm also curious did you decide against a full deep dive on Sea limited or just been too busy with the Heico deep dive?

Jesus, you've technically just written a book about HEICO 😂