Part 4 of the Kinsale Deep Dive will be pusblished on Wednesday, January 21. In this “Fundamental”, we look at the mechanics of reinsurance. It’s a bit "technical”, but it was important for me to understand how it works and how reinsurance impacts the financial statements.

1. Why reinsurance matters

Reinsurance is one of the most important, but often least understood, parts of an insurer’s business model. This is especially true in the E&S market, where many risks are unusual, complex or concentrated and where loss patterns can be highly volatile. On the surface, reinsurance looks simple – an insurer passes part of its risk to another insurer.

Reinsurance shapes the volatility of earnings, the amount of capital required, the capacity to write new business and, ultimately, the company’s long-term return on equity.

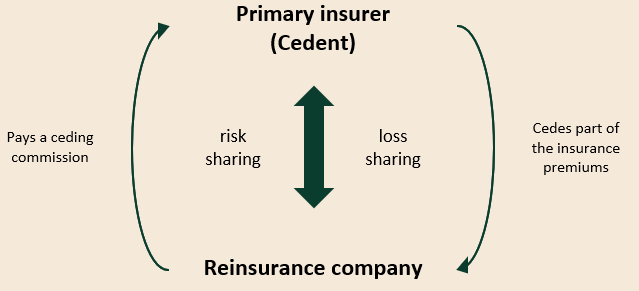

A reinsurance agreement is a contract between at least two parties: the primary insurer (the cedent) and one or more reinsurers. Under this agreement, the reinsurer agrees to assume a defined share of the cedent’s risk on pre-agreed terms. The reinsurer can, in turn, choose to lay off part of this assumed risk through retrocession to other reinsurers. This creates a chain of risk transfer that helps distribute and manage large or complex exposures across multiple balance sheets.

For the cedent, reinsurance shifts part of the risk from its own balance sheet to that of the reinsurer. This reduces the capital at risk in the event of large losses, stabilizes results and frees up capacity to underwrite additional business.

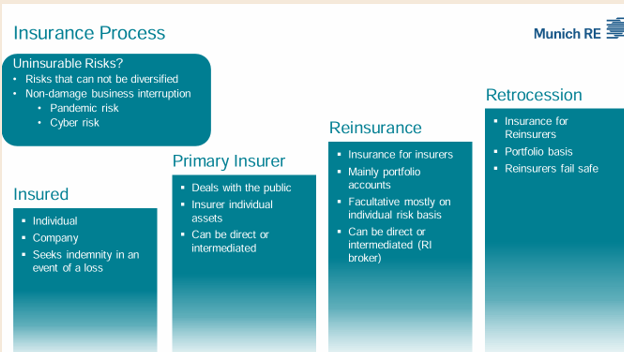

Simply put, reinsurance is insurance for an insurer.

For Kinsale, reinsurance is not a mere compliance requirement. It is a central tool to protect the balance sheet against large individual losses and catastrophe events, to stabilise underwriting results, to support growth in attractive niches and to meet regulatory and rating agency expectations. Understanding how reinsurance works in general – and how Kinsale’s programme is set up in particular – is therefore essential for understanding the company’s risk profile and economics.

Reinsurance serves several functions for a primary insurer:

Protection against major losses: Large single claims or catastrophe events can threaten an insurer’s solvency. Reinsurance absorbs a portion of these extreme losses and helps stabilize capital and ratings.

Stabilization of profits: By ceding part of the volatility in its portfolio to reinsurers, a company can make its earnings profile more predictable over time.

Increased underwriting capacity: Reinsurance allows an insurer to write more business than it could on its own balance sheet by freeing up capital and limiting downside risk.

Access to expertise: Reinsurers often possess deep analytical capabilities and global experience in specific risk classes, which can support product design, pricing and claims management.

Regulatory and capital relief: In many jurisdictions, reinsurance helps reduce required regulatory capital, as part of the risk is transferred to strongly capitalized counterparties.

Market entry and experimentation: Reinsurance can be used to test new products or enter new markets with a lower balance-sheet risk, especially when loss histories are limited or uncertainty is high.

2. Reinsurance fundamentals – the tools Kinsale is using

2.1. Obligatory vs. facultative reinsurance

Reinsurance contracts can broadly be grouped into obligatory and facultative arrangements. The distinction is about which risks must be ceded under the contract and how much discretion the parties have.

In an obligatory reinsurance treaty, the primary insurer (cedent) and the reinsurer agree in advance on a defined portfolio of risks. If a policy falls within the scope of that treaty, it must be ceded, and the reinsurer is obliged to accept its share. Obligatory treaties are typically used for large, recurring books of business – for example auto insurance policies. Flexibility is limited, as the germs are predetermined, and all defined risks must be reinsured under the agreement.

Facultative reinsurance, by contrast, is arranged case by case. The primary insurer offers a specific risk to the reinsurer, which can then decide whether to accept or decline it and on what terms. Facultative reinsurance is particularly common for very large, unusual or complex single risks that do not fit neatly into a standard treaty structure. This type of reinsurance offers greater flexibility, as the primary insurer can decide for each risk whether to reinsure it and on what terms, or not. However, the reinsurer may decline to accept the specified risk.

2.2. Proportional vs. non-proportional risk sharing

A second important distinction relates to how premiums and losses are shared between the primary insurer and the reinsurer. The basic categories are proportional and non-proportional reinsurance.

2.2.1. Proportional reinsurance: quota-share and surplus

In proportional reinsurance, the reinsurer takes on a fixed share of both premiums and losses. The primary insurer and the reinsurer participate in the same underlying risks in the agreed proportion and share premiums and losses proportionally. The reinsurer typically pays a ceding commission back to the cedent to compensate for a share of acquisition and administrative expenses.

There are two main forms of proportional reinsurance:

2.2.1.1. Quota-share reinsurance

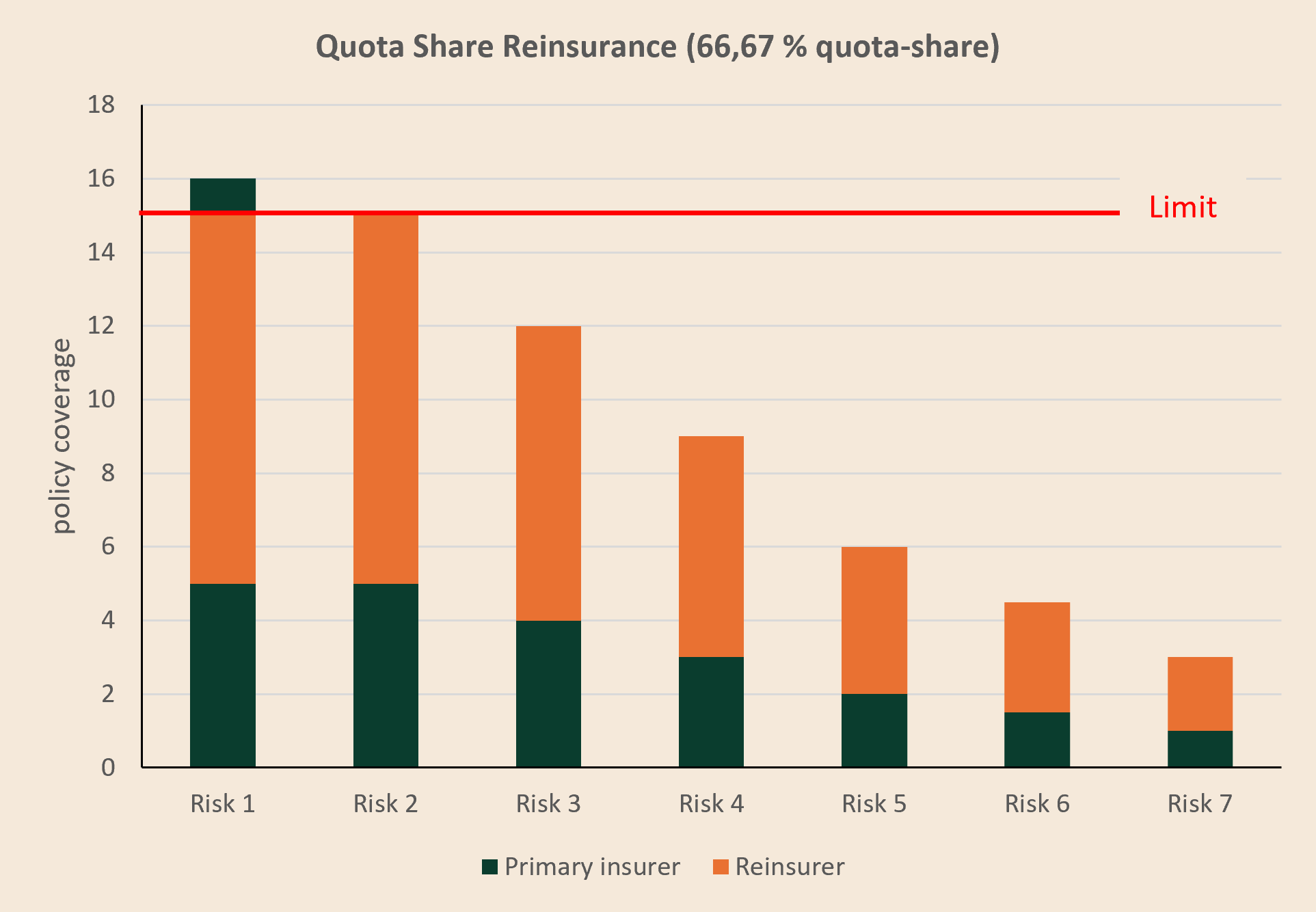

In a quota-share treaty, premiums and risks are shared between the primary insurer and the reinsurer in a fixed proportion. This structure is often used when the cedent wants a broad, even sharing of risk and premium with a reinsurer, rather than transferring only specific layers.

Because the reinsurer assumes a fixed percentage of both premiums and claims, quota-share reinsurance has a stabilizing effect on the cedent’s income statement: losses are smoothed in line with the agreed quota. The trade-off is that the cedent also gives up a corresponding share of its potential underwriting profit.

The reinsurer’s liability is capped at a defined limit, but within that framework all risks (premiums and losses) are split according to the agreed percentages. The cedent’s retention and the reinsurer’s share are expressed as percentages, so the absolute dollar amounts vary with the size of the insured risk.

Consider the following example:

The quota-share is 66.67% (2/3) in favour of the reinsurer.

The primary insurer retains 33.33% (1/3).

The reinsurer’s liability limit is $10 million.

The risk is then allocated as follows:

For the portion of the claim up to a total claim size of $15 million, the reinsurer takes two-thirds, and the cedent retains one-third.

If the claim exceeds the total of $15 million, any excess above this level has to be borne by the cedent or protected via additional reinsurance (for example, an excess-of-loss cover, as illustrated by Risk 1 in the chart below).

Both premiums collected and the claims paid are split according to the agreed percentage. For instance, if the insurer collects $1 million in premiums and the quota share is 66.67%, the reinsurer receives $666,667 in premiums and is responsible for 66.67% of any claims. If a $12 million claim is filed, the reinsurer pays $8 million and the cedent pays $4 million.

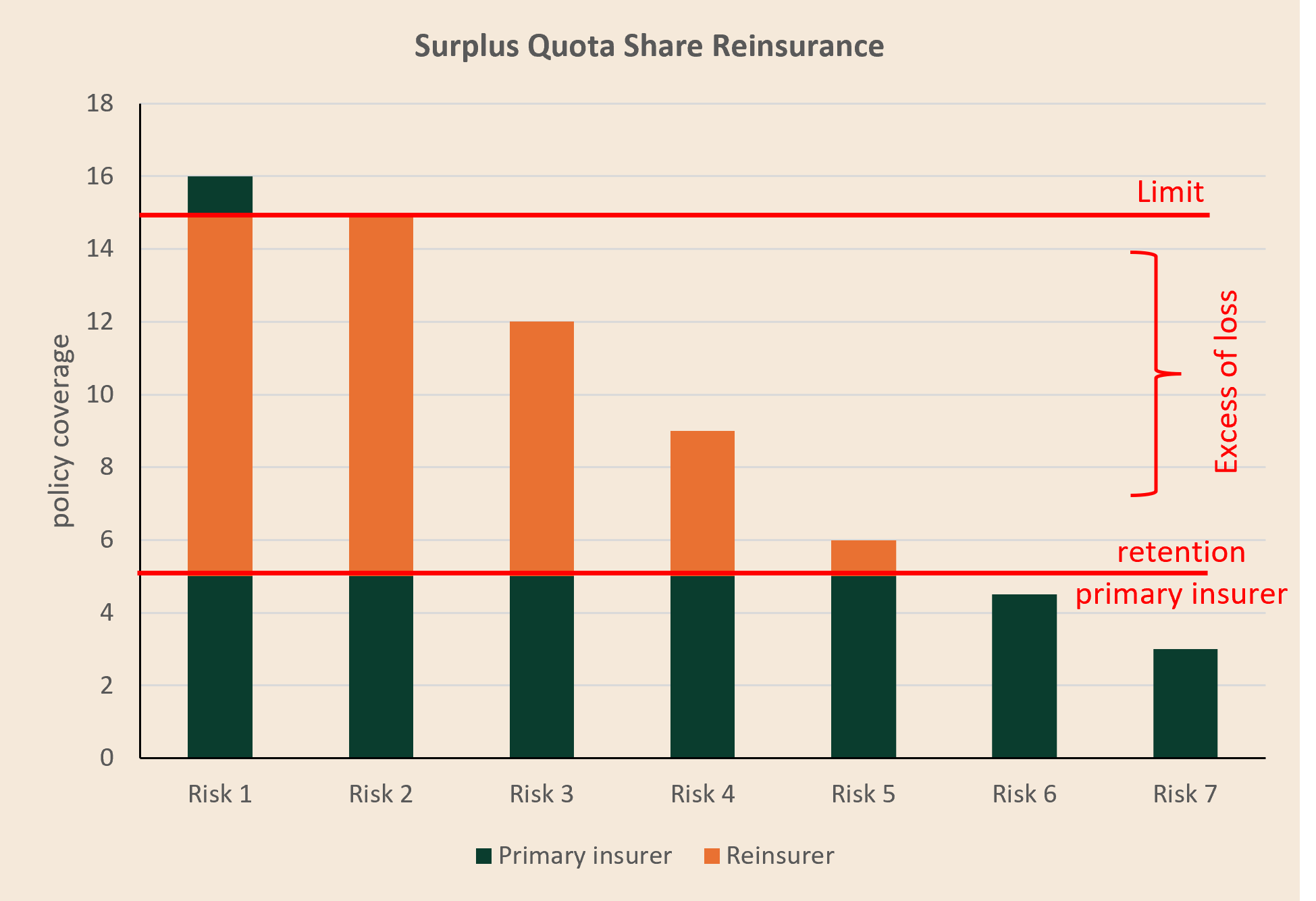

2.2.1.2. Surplus Quota-share reinsurance

The key difference between surplus quota-share reinsurance and a straight quota-share treaty is that the cedent’s retention is defined as an absolute amount (“maximum”) rather than as a fixed percentage of every risk. What doesn’t differ though is the proportional distribution of premiums and losses.

The reinsurer’s liability limit is typically set as a multiple of this maximum and agreed upfront in the contract.

The portion of the sum insured that exceeds the cedent’s maximum is referred to as the surplus and is assumed by the reinsurer.

Premiums are allocated proportionally between cedent and reinsurer for each individual risk according to this split.

Example:

A policy covers risk of $16 million.

The annual premium is $1 million.

The surplus quota-share treaty comes with a retention (“maximum”) of $5 million for the cedent.

The reinsurer agrees to cover up to (!) two times this retention as surplus, but it can be less, depending on each risk.

For Risks 1–4, the policy coverage lies above the retention line. In these cases, the primary insurer always retains the first $5 million of each risk (the green portion), while the excess above the retention up to the limit is ceded to the reinsurer (the orange portion). Where the bar reaches the top red line (e.g. Risk 1), the treaty capacity is fully utilized.

For Risks 5–7, the policy coverage is below the retention. In those cases, there is no surplus to cede and the bars are entirely green: the primary insurer retains 100% of the risk and the full premium.

Let’s take a closer look at Risk 3. The sum insured is $12m and the cedent retains $5m. In the event of a loss, the reinsurer would cover up to(!) $7m. For this particular risk, the proportional allocation of premium and losses is therefore:

Cedent: $5 million / $12 million ≈ 42%

Reinsurer: $7 million / $12 million ≈ 58%

Assume the insurance premium is $1m: the reinsurer receives $580,000 and $420,000 remain with the primary insurer. If a loss of $3m occurs, it is borne proportionally in the same ratio – roughly $1.25m by the cedent and $1.75m by the reinsurer. Although the loss is below the cedent’s maximum (!) retention of $5m, it does not fall 100% on the primary insurer. This is a defining feature of proportional surplus quota-share reinsurance (and what confuses most people).

2.2.2. Non-proportional reinsurance: excess of loss and catastrophe covers

Non-proportional reinsurance works differently. Instead of sharing every premium and every loss in a fixed ratio, the reinsurer only steps in above a specified threshold – the retention or priority – and up to an agreed limit. Below the retention, the primary insurer bears the entire loss.

In an excess-of-loss treaty, the reinsurer only assumes the portion of any single claim that exceeds the cedent’s retention, up to a contractually defined limit (the “excess” layer). This type of cover is typically used when the primary insurer wants to protect itself against large, infrequent losses but is comfortable retaining smaller and medium-sized claims on its own balance sheet. It is particularly useful as protection against catastrophic events or unusually large individual losses.

The impact on the income statement is therefore irregular. As long as claims remain below the retention, the primary insurer keeps 100% of the premium and bears the entire loss. While the cedent pays a regular premium for the excess-of-loss cover, recoveries from the reinsurer only arise when losses breach the retention and enter the excess layer. As a result, the volatility-reducing effect of the treaty on the cedent’s P&L is concentrated in adverse years, even though the ceded premium expense is recognized evenly over time.

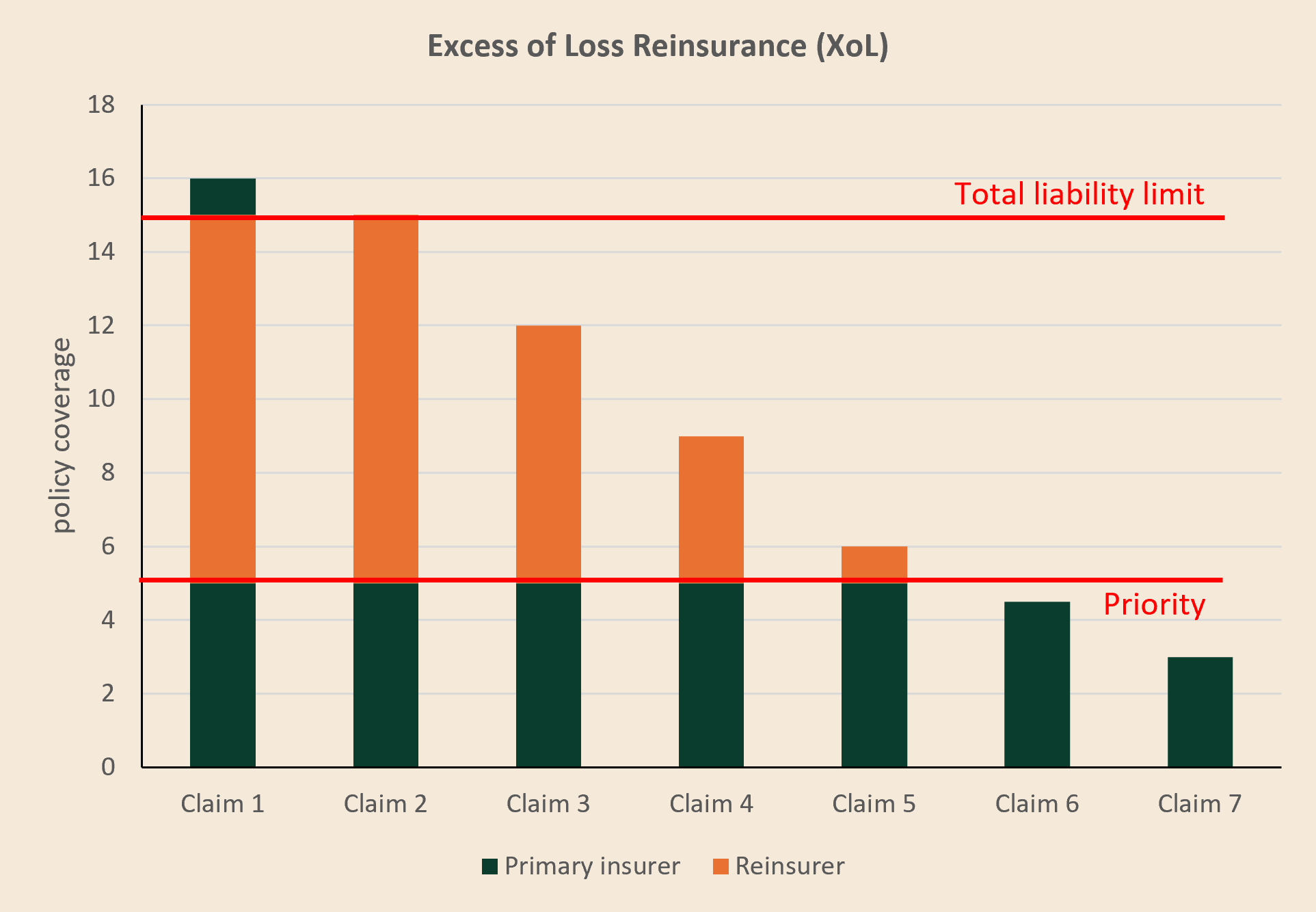

2.2.2.1. Excess of loss (XoL)

XoL reinsurance is the most common non-proportional structure. The reinsurer only covers that part of a loss which exceeds a pre-defined threshold called “priority”. The primary insurer bears all claims up to this retention, while the reinsurer takes over the portion of the loss above the retention, up to a contractually agreed maximum. In return, the cedent pays a reinsurance premium. Unlike in proportional treaties, this premium is not a fixed percentage of the original premium, but is based on the expected frequency and severity of losses that might hit the excess layer.

Excess-of-loss cover is activated by the actual loss amount: the reinsurer only steps in once a claim exceeds the retention and then pays the portion above that threshold, up to the agreed limit. Unlike proportional treaties, the reinsurer’s participation is not derived from a fixed share of the sum insured.

The parties agree (1) a loss threshold (also called the attachment point or excess point or priority) and (2) a liability limit, i.e. the maximum amount the reinsurer will pay for a single loss. Together, the retention and the liability limit define the total layer of coverage. For this protection, the cedent pays a fixed reinsurance premium for the contract period.

Example:

Assume a policy with a coverage of $15 million and an annual premium of $1 million. The primary insurer and the reinsurer enter into an XoL treaty with a retention of $5 million and a liability limit equal to four times the retention. The reinsurer therefore covers the loss layer of $10 million in excess of $5 million. The cedent remains fully exposed to all losses up to $5 million.

The premium ceded to the reinsurer under this XoL contract is determined on a non-proportional basis: it is negotiated as a function of exposure and expected losses in the excess layer, rather than being mechanically linked to a fixed share of the underlying premium or the nominal amount of risk ceded.

In non-proportional reinsurance, a shorthand notation is often used to describe the cover:

Limit xs Priority

For example, a layer of $10 million xs $5 million in an XoL context means that the reinsurer covers losses above $5 million, up to a maximum of $10 million per loss (or per event, in the CatXL case, see below):

The following graphic illustrates how this reinsurance works using seven different claims (not risks!).

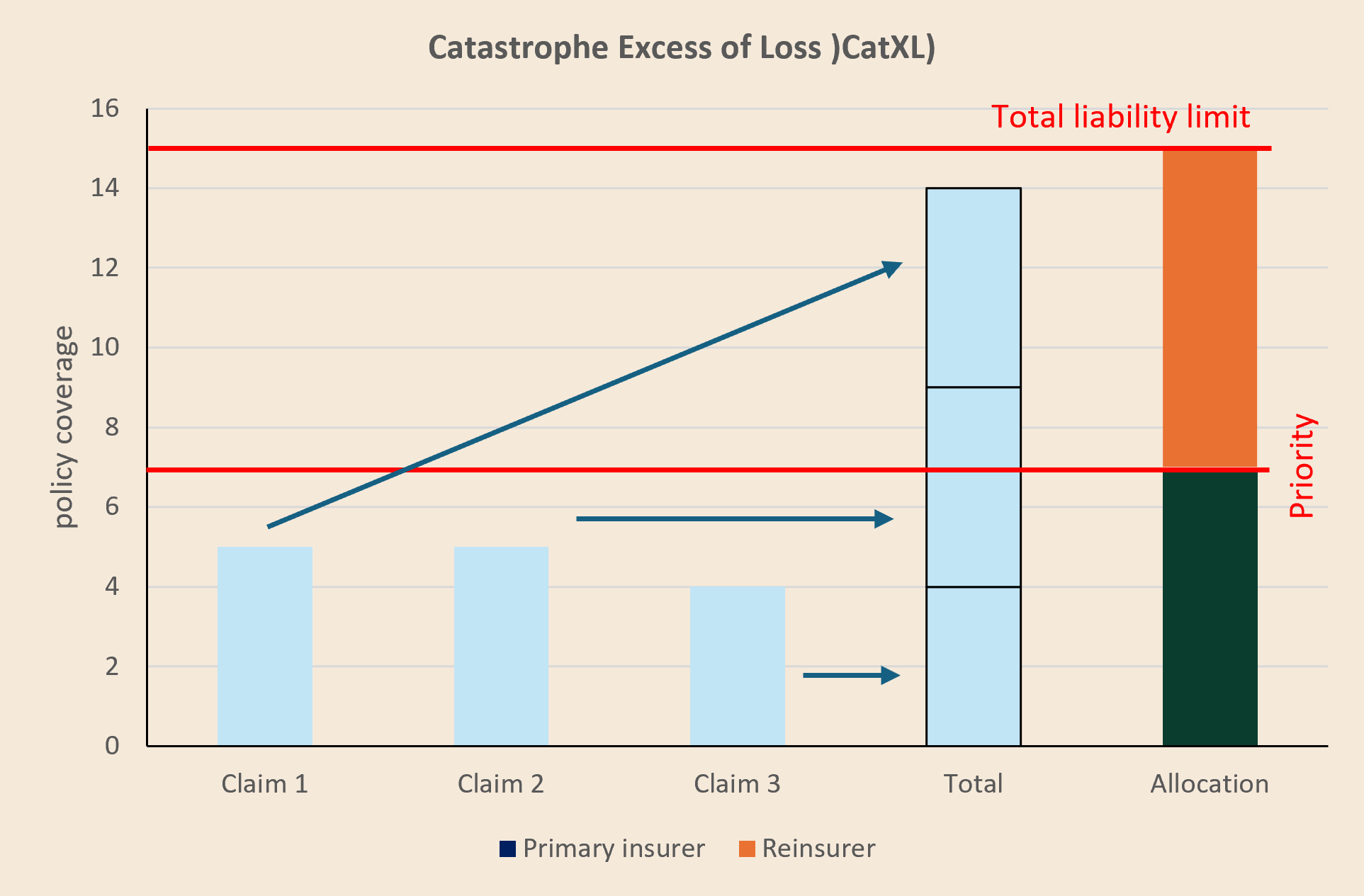

2.2.2.2. Catastrophe Excess of Loss (CatXL).

In catastrophe excess of loss reinsurance, the priority and the total liability limit are defined as absolute amounts, similar to a standard XoL cover. The key difference is how the loss is defined: in CatXL, the relevant loss is the sum of all individual claims arising from a single event, such as a hailstorm, hurricane or earthquake.

The contractual definition of what constitutes an “event” is therefore critical, because the reinsurer only responds once such an event has occurred and the aggregate losses from that event are known.

In this context, the priority is typically set above the maximum expected individual loss. The reinsurer only comes into play when the cumulative damage from the event exceeds the agreed priority. Above this threshold, the reinsurer covers the layer of losses up to the stated liability limit.

2.3. Ceding commissions – who pays whom and why

When a primary insurer cedes business to a reinsurer, it typically receives a ceding commission. This commission is meant to compensate the cedent for part of the acquisition and underwriting costs it incurs when originating the business – for example broker commissions, internal underwriting expenses and policy administration.

There are three common forms of ceding commission:

Flat commission: A fixed percentage of ceded premium that does not change with the performance of the underlying book. This is simple but can create poor incentives if the cedent earns the same commission regardless of underwriting quality.

Sliding-scale commission: The commission level depends on the loss ratio of the ceded business. A lower loss ratio results in a higher commission for the cedent, while a higher loss ratio reduces the commission. This aligns the interests of cedent and reinsurer more closely.

Profit commission: An additional commission that becomes payable if the ceded portfolio is particularly profitable. This structure provides a strong incentive for the cedent to maintain disciplined underwriting even when a large share of the risk is passed to the reinsurer.

In practice, reinsurance programmes often combine quota-share and excess-of-loss treaties with carefully structured ceding commissions. The overall design determines not only how losses are shared, but also how profitable new business is for the primary insurer after reinsurance.

3. Accounting for reinsurance: net vs. gross

3.1. How reinsurance flows through the income statement

In the income statement, Kinsale reports its underwriting results on a net basis – that is, after the effects of reinsurance. This has several implications for how the top line and key ratios should be read:

Premiums: Ceded premiums reduce gross written premium to arrive at net written premium. Net earned premium is therefore the portion of premium that remains with Kinsale after reinsurance over the period in which coverage is provided.

Losses and loss adjustment expenses: These are reported net of the amounts expected from reinsurers. If a large loss is partially covered by reinsurance, only the net portion borne by Kinsale appears as loss expense in the income statement.

Acquisition and insurance expenses: These are shown after deducting ceding commissions received from reinsurers. The commissions offset part of the direct commissions paid to brokers and internal acquisition and underwriting costs.

Understanding these linkages is important. Strong net underwriting results at Kinsale reflect not only pricing and risk selection, but also how reinsurance is structured and how much volatility is retained on the company’s own balance sheet.

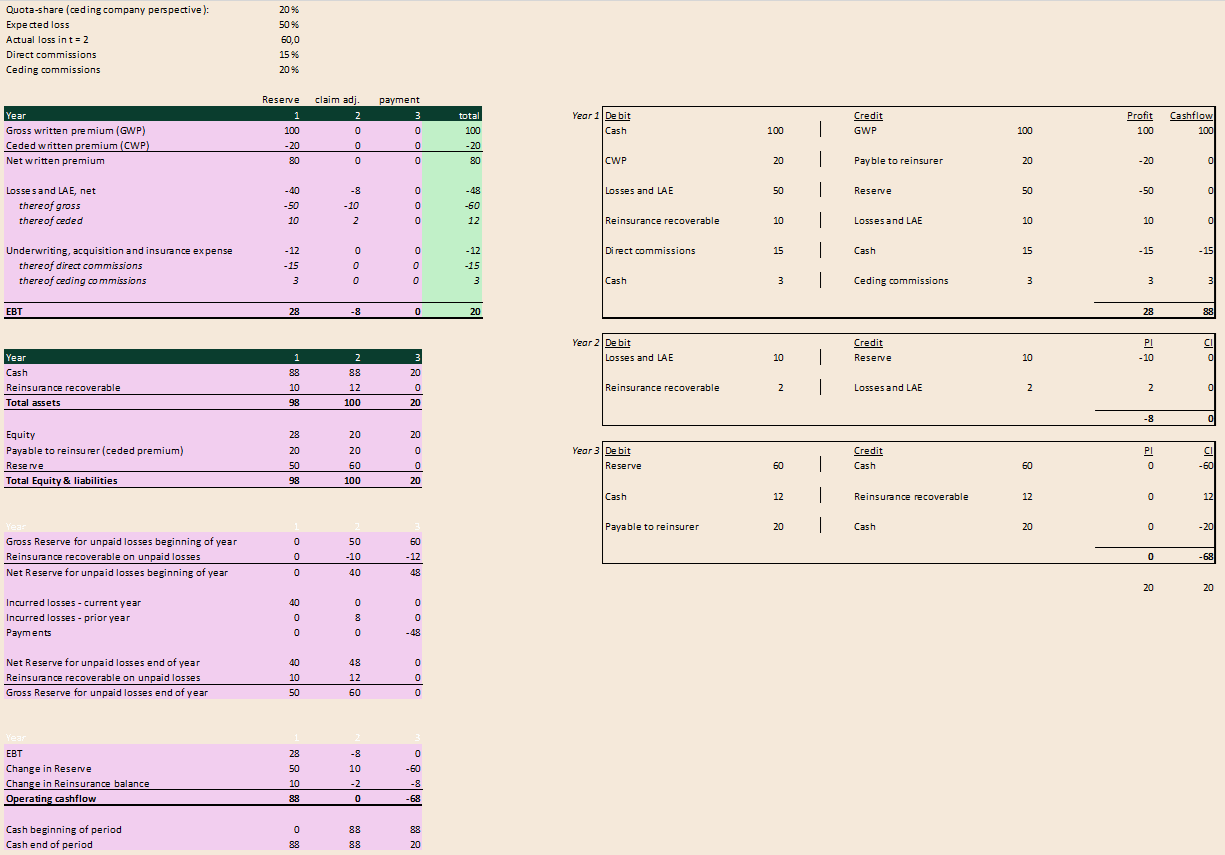

3.2. Balance sheet mechanics – a simple three-year example

The balance sheet impact of reinsurance is easiest to see in a simplified example. We will go through the journal cycle to fully comprehend how reinsurance transactions impact financial statements.

Consider a single insurance contract with the following assumptions:

Gross premium: 100

Quota-share reinsurance: 20% (remaining with the insurer)

Expected loss at inception: 50

Actual loss ultimately incurred: 60

Broker commission: 15 % of gross premium

Ceding commission from reinsurer: 20% of the broker commission (i.e. 3)

Contract written on 1 January with a one-year coverage period, hence no pro rata revenue recognition. Net written premiums equal Net earned premiums

Year 1: Initial recognition of the IBNR reserve and payment of commission

Year 2: Increase (strengthening) of the IBNR reserve

Year 3: Settlement of the claim by paying the insured and settling the corresponding amounts with the reinsurer

The following sections go through accounting events. A summary follows afterwards.

3.2.1. Year 1 – premium, initial reserve and commissions

First, the insured pays the gross premium of 100, which increases cash. At the same time, a liability to the reinsurer for ceded premiums of 20 (20% of 100) is recorded. This reduces net premium revenue but does not affect cash immediately, as we assume that the payment to the reinsurer follows in Year 3.

Next, the claims reserve is established based on the expected loss of 50. In parallel, a reinsurance receivable of 10 (20% of 50) is recognised for the reinsurer’s quota-share of that expected loss. On a net basis, this results in earned premiums of 80 and loss and loss adjustment expenses of 40 in the income statement for Year 1.

Finally, acquisition costs are recorded. The direct broker commission of 15 reduces profit and cash. The ceding commission from the reinsurer – 3, or 20% of the broker commission – is recognised as income and cash inflow.

After these steps, the underwriting profit (EBT) for Year 1 is 28. On the balance sheet, cash stands at 88 (100 gross premium minus 12 net acquisition expenses), reinsurance recoverables at 10, equity has increased by the 28 of profit, and liabilities include 20 due to the reinsurer for ceded premium and a gross loss reserve of 50.

3.2.2. Year 2 – reserve strengthening as the claim develops

In Year 2, the claim is reported and the expected ultimate loss is revised upward from 50 to 60. The claims reserve must therefore be increased by 10. Of this amount, again 20% (2) is recognised as an additional reinsurance receivable, reflecting the reinsurer’s share of the higher expected loss. The remaining 8 are booked as additional loss expense. The net effect is a loss of 8 in the Year‑2 income statement.

On the balance sheet, the claims reserve increases from 50 to 60, and the reinsurance recoverable increases from 10 to 12. The reinsurance premium payable and cash positions are unchanged in this step.

3.2.3. Year 3 – settlement of the claim and cash flows

In Year 3, the claim is settled and the reserve is released. Kinsale pays 60 in claims to the policyholder, resulting in a cash outflow. At the same time, it collects 12 from the reinsurer, corresponding to the 20% share of the final loss. The liability for ceded premium of 20 is also paid. Depending on how the entries are booked, the reinsurer’s payment can either be recorded as an incoming cash flow or be offset directly against the liability for ceded premiums.

After settlement, the claims reserve and reinsurance recoverable for this contract have both been reduced to zero. The cumulative profit over the three years reflects the underwriting margin after reinsurance and the cost of the quota-share protection.

From the gross premium of 100, 20 were ceded to the reinsurer, leaving 80 of net premium. The ultimate loss was 60, of which 12 were reimbursed by the reinsurer, so 48 were borne by the insurer. After deducting net acquisition expenses of 12, the insurer earns a profit of 20. This corresponds to a loss ratio of 60%, an expense ratio of 15% and a combined ratio of 75% on this simplified example (25 % EBT vs 80 Net Earned Premiums).

3.3. Gross vs net

From an accounting perspective, it is important to distinguish between gross and net presentation.

On the balance sheet, technical provisions such as the loss reserve are reported on a gross basis, i.e. including the portion that is ultimately expected to be borne by reinsurers. The reinsurer’s share is recognized separately as an asset under reinsurance recoverables on unpaid losses, so that the net obligation of the primary insurer is the gross reserve minus this recoverable.

In the income statement, by contrast, premiums, losses and loss adjustment expenses are already shown net of reinsurance: ceded written premiums reduce earned premiums, and reinsurance recoveries reduce losses and LAE. As a result, the P&L reflects only the insurer’s retained share, while the balance sheet shows gross reserves together with the corresponding reinsurance asset.

Incredibly helpful, especially the example you end with. Thanks a lot!