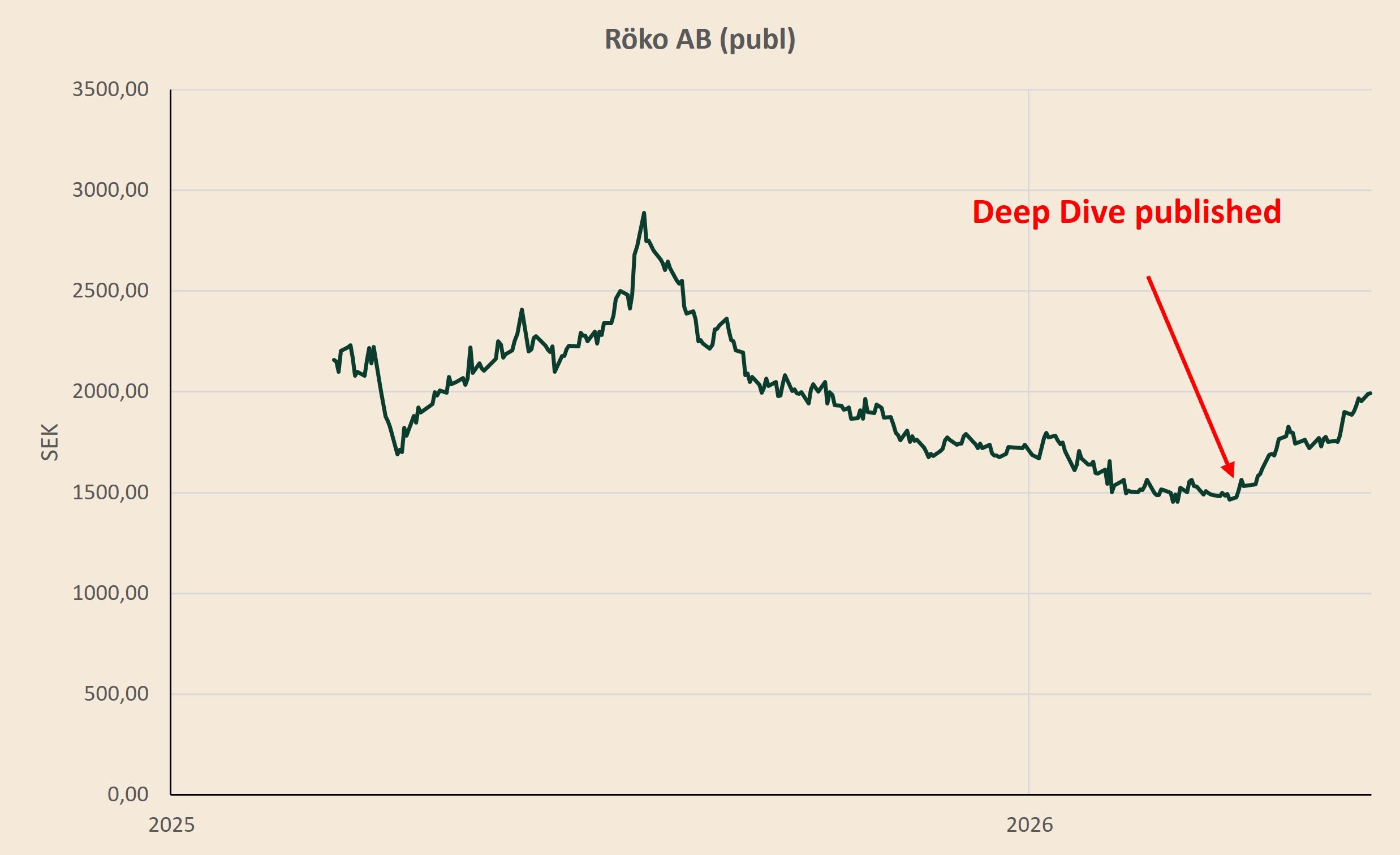

The timing of my Deep Dive was more luck than skill, but since publishing the series, Röko’s share price has started to recover materially (up ~30%). More importantly, the underlying story has also improved: the M&A machine is beginning to move again.

2025 was a frustrating year for Röko from an M&A perspective. Management was very open about it. In Q3, Johan Bladh said they were “not satisfied” with profit growth, that organic development was not satisfactory, and that Röko had not completed acquisitions at the pace they aim for. The most important line, in my view, was this: “the pipeline is not worth anything as long as we do not complete acquisitions.”

For a serial acquirer, a nice pipeline does not compound capital. Only closed deals do — assuming they are accretive and generate attractive ROIIC.

That said, capital deployment in serial acquisition is inherently lumpy. Deals are binary, timing is hard to predict, and a few larger transactions can make one quarter look unusually strong while another period looks quiet. This is also one of the reasons why many investors stay away from serial acquirers. A meaningful part of the growth engine has very little visibility. And low visibility means uncertainty — something the stock market rarely likes.

But for long-term investors, that is also part of the appeal. If the market is overly focused on near-term visibility, it may underappreciate the value of a proven acquisition engine that compounds capital over many years. The key requirement, of course, is trust in management’s capital allocation. That trust should not be based on storytelling, but on evidence: disciplined deal-making, attractive returns on incremental capital, and a long track record of buying good businesses at attractive prices.

This is why the start of 2026 is interesting. A single quarter (again) does not prove that the acquisition engine is back to full speed, but it does show that Röko has started to move from pipeline to execution again.

In Q1 alone, Röko completed three acquisitions:

Lambda is an Italian manufacturer of dental and veterinary lasers with global sales, adding another medical technology niche to Röko’s B2B segment.

ABP Group is a UK-based manufacturer and supplier of access panels and door canopies for commercial and residential buildings, a more construction-exposed but market-leading building products business.

Golfshopen, meanwhile, is Norway’s leading golf equipment retailer and fits neatly with Röko’s existing ownership of Denmark’s leading golf equipment retailer, which it acquired in 2021.

Together, these three businesses add MSEK 552 of annual net sales.

Management also sounded notably more constructive on the M&A environment. On the Q1 call, Johan Bladh said that Röko believes “the M&A market has improved” and that they are seeing “more and more deals with good quality.” He also highlighted a “good inflow of new acquisition opportunities,” which should support a strong pipeline for the rest of the year.

Then, in mid-May, Röko announced the acquisition of Fri-Jado in the Netherlands: a global market leader in chicken rotisseries and hot/cold food displays with annual net sales of €64 million and roughly 220 employees. Röko acquired 93% of the business, making it Röko’s fifth platform acquisition in the Netherlands and, by disclosed sales, its largest acquisition to date.

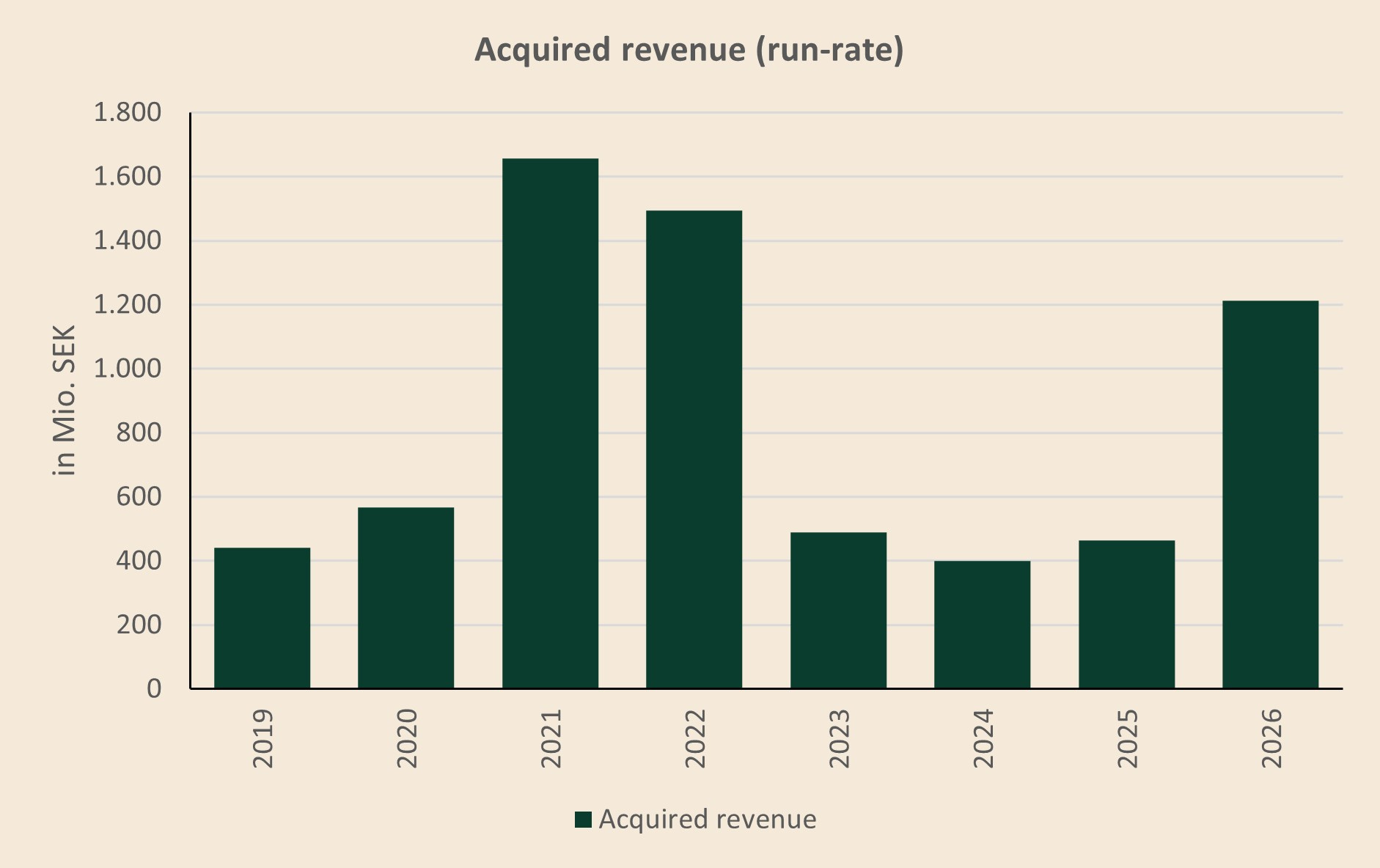

So within the first five months of the year, Röko has already deployed meaningful capital again. The chart below puts this acceleration into perspective. Including the Q1 acquisitions and the recently announced Fri-Jado deal, Röko has already added roughly SEK 1.2 billion of acquired revenue run-rate in 2026. That is almost as much as the company acquired in total during the three-year period from 2023 to 2025.

The issue in 2025 was not a broken acquisition model, but a temporary lack of completed deals. The market, however, treated that lack of execution as if the machine itself was impaired. After the IPO, and particularly from July 2025 onward, Röko’s share price suffered a drawdown of roughly 50%, largely reflecting the market’s frustration with weak visibility and slower-than-expected acquired growth. Early 2026 suggests that the machine is starting to move again.

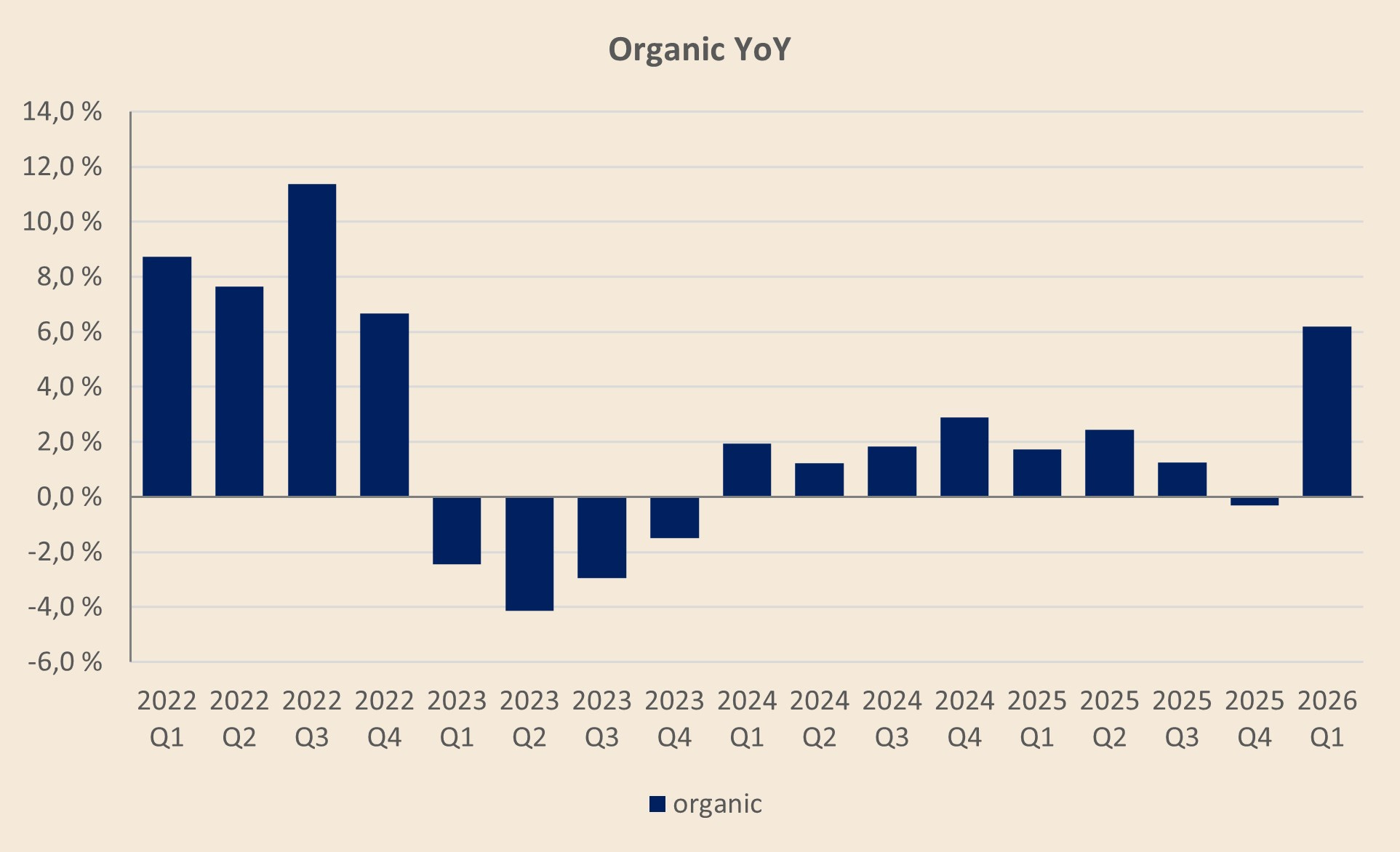

Looking ahead, this should also start to show up more clearly in the reported numbers. Excluding seasonal effects, I would expect M&A-driven growth to accelerate further in Q2 as the Q1 acquisitions contribute for a fuller period. By Q3, once the five completed 2026 acquisitions are more fully reflected in the numbers, acquired growth should move above 20%, compared to roughly 9% in Q1.

The other encouraging data point in Q1 was organic growth. After several quarters of low-single-digit growth and even a slightly negative Q4 2025, organic net sales growth rebounded to 6% in local currency, the strongest quarterly organic growth rate since 2022. That should not be overinterpreted as a pure volume recovery. On the call, management was careful not to split the contribution between volume and price, given the diversity of Röko’s subsidiaries. But Johan Bladh did point to the work Röko has done over the past few years to educate local management teams on continuous price increases, with some companies benefiting from the current environment by raising prices. Q1’s organic growth seems to be driven at least meaningfully by pricing rather than a broad-based demand rebound.

FX was a headwind in Q1 (again). Röko reports in Swedish krona, but 29 of its 33 subsidiaries report in other currencies, so the sharp appreciation of the SEK created a meaningful translation drag. FX reduced growth by 6 percentage points. The same effect also weighed on Adj. EBITA and operating profit, while net income was additionally hit by SEK 26 million of negative FX effects in financial items.

And that is pretty much where I stand today. The key pieces are in place: a proven acquisition culture, a decentralized model, disciplined capital allocation, improving M&A momentum, and a portfolio of niche businesses that should continue to compound over time. For now, there is not much more to write about. The best thing to do may simply be to let time pass, let the company compound, and watch management continue to allocate capital. I look forward to being a shareholder for hopefully many more years to come.

Same here, thanks Alexander