Short reports can be very useful. They force investors to stress-test a thesis and look for evidence that might otherwise be ignored. The best short sellers do real work and make long investors better.

But sometimes short reports are just exhausting when a handful of scary anecdotes gets packaged into a much broader conclusion than the evidence can actually support.

That is how I currently view the latest Kinsale Capital Group bear piece from The Bear Cave by Edwin Dorsey.

The core allegation is familiar: Kinsale is supposedly not a high-quality E&S compounder with superior underwriting, technology, low costs, and strong execution. Instead, the story goes, Kinsale is allegedly selling overpriced, exclusion-heavy insurance to less sophisticated small businesses, then denying claims when losses occur. The conclusion is that Kinsale’s business is low quality and unsustainable.

That is a serious allegation. It deserves to be taken seriously. But it also deserves a serious evidentiary standard.

This is not the first time Kinsale has been attacked along these lines. The earlier version came through the PAA Research short pitch last year.

I recently published a roughly 100-page Deep Dive on Kinsale. Unsurprisingly, I reached a very different conclusion. After reading the Bear Cave piece, I reached out to Edwin Dorsey to discuss the arguments, and I specifically asked whether he had also requested complaint files for Kinsale’s competitors. As of writing, I have not received feedback on those counterarguments.

So let me lay out my view, allegation by allegation.

The bear case in one sentence

The short thesis is that Kinsale’s industry-leading margins are not driven by a real moat, but by a combination of high prices, narrow policy wording, limited regulatory oversight, and a less sophisticated customer base.

That sounds plausible on the surface. E&S insurance is less standardized than admitted insurance. Policies can be more customized. Rates and forms can often be changed without the same pre-approval regime. Customers are often small businesses with unusual risks. And if one reads a complaint from an angry insured after a denied claim, it can look terrible.

The problem is that this is exactly why base rates matter. A few ugly files do not tell us whether Kinsale is an outlier. They tell us that some customers are angry. That is not the same thing.

1. “Kinsale sells overpriced insurance”

This is probably the weakest part of the bear case in my view.

Kinsale operates in a highly competitive market and sells through brokers. Brokers can and do obtain multiple quotes. In many E&S placements, the risk first has to be declined by admitted carriers before it can be exported to the surplus lines market, unless the risk is on an export list (please check out Part 2 of my Deep Dive for a better understanding of E&S regulation).

Nobody is forced to buy insurance from Kinsale.

If Kinsale were simply charging ‘enormous amounts’ for a clearly inferior product, the most obvious question is: why did the company grow so much for so long?

In my view, the more likely explanation is that Kinsale is structurally more efficient in a commodity-like market where speed, price, capacity, terms, and risk appetite all matter.

In the recent Rock & Turner interview, CEO Michael Kehoe was very direct about this.

“Insurance is a commodity business, especially when you sell to an SME type customer. There’s an exaggerated emphasis on price to the exclusion of other considerations. And so I think it’s really important to design and build the company always with an eye toward efficiency. Let’s wring every expense we can out of the transactions. And then the customer gets a little bit of that savings in the form of better insurance pricing.” (Michael Kehoe, CEO)

Insurance, especially SME insurance, is a commodity-like business where buyers care a lot about price. Again, why did Kinsale grow so much for so long if they were overpriced?

Kinsale decides what risks it is willing to cover and at what price. If customers or brokers do not like the terms, they are free to seek quotes elsewhere.

2. “Kinsale targets unsophisticated customers”

This argument sounds intuitive, but it ignores how insurance is actually distributed.

Kinsale’s end customer may be a small business. But the placement typically involves a retail agent and a wholesale broker. The broker’s job is to find the best available mix of coverage, price, capacity, and execution. If a broker consistently places customers into inappropriate coverage, that is a broker problem. It is not automatically proof that the insurer’s entire business model is predatory.

Kehoe made the broker point clearly in the interview:

“Brokers need markets, right? That’s their job is to serve their customers and get the best mix of coverage and price.” (Michael Kehoe, CEO)

Kinsale depends on brokers as its sales force, while brokers depend on insurers to solve hard-to-place risks. This is a symbiotic relationship, not a simple one-way exploitation of uninformed buyers.

The SME focus is also not suspicious by itself (honestly, I don’t understand why that’s a problem). It’s quite the opposite, as smaller accounts are operationally more difficult. Kinsale had around one million new business submissions in 2025, sent out roughly 750,000 new business quotes, bound about 100,000 new policies plus another roughly 100,000 renewals, and handled thousands of claims. That volume is exactly why many competitors struggle to serve this market directly and often use MGAs instead.

Kinsale keeps underwriting in-house. That gives it more control over risk selection, pricing, claims feedback, and economics. To me, that is not a sign of low quality. It is one of the core reasons the business deserves attention in the first place, as Kinsale found its sweet spot in a niche of a niche market.

3. “The policies are exclusion-heavy, so customers do not really have insurance coverage”

This is the most emotionally powerful part of the short case. It is also the argument Edwin Dorsey leans on most heavily in his Bear Cave report. It is also the part where one has to be very careful.

Insurance is a contract. It covers certain risks and excludes others. This is not a bug of the insurance industry; it is the product. In E&S insurance, where risks are unusual, distressed, hazardous, or hard to place, customized terms and exclusions are even more normal.

That does not mean every exclusion is fair, every policy is well explained, or every insured understands what they bought. But it does mean that pointing to an exclusion after a claim denial is not enough. The relevant question is: was the policy priced and sold based on the coverage actually provided, and did the broker and insured understand what was excluded?

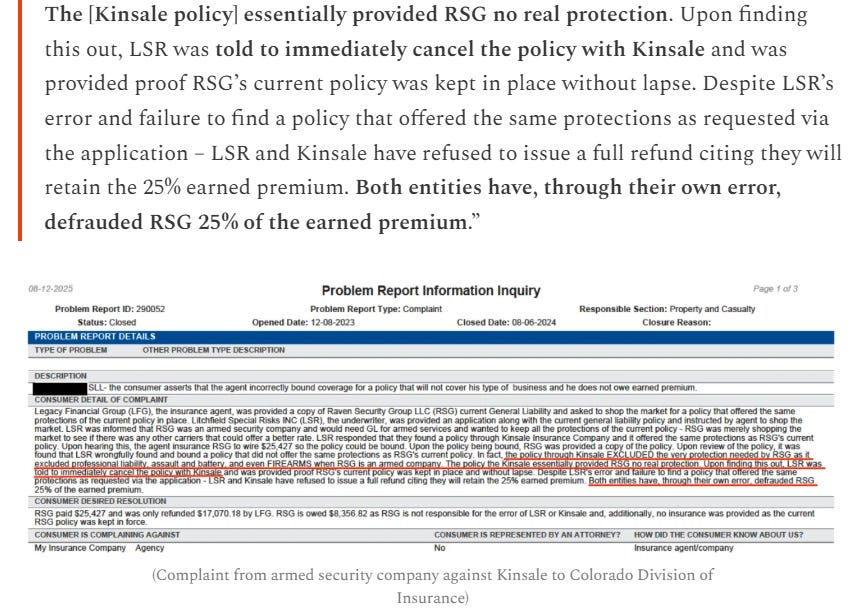

To support this allegation, The Bear Cave cherry-picked a handful of negative customer complaints. One of those is Raven Security Group (RSG), a private armed security company in Colorado. The complaint says the broker, LSR, allegedly found and bound a policy that did not offer the same protections as RSG’s existing policy. Kinsale’s coverage allegedly excluded the very protection needed by RSG as it excluded professional liability, assault and battery, and firearms.

Come on, you really can not blame Kinsale.

The lawsuit example appears to be a broker issue rather than a Kinsale issue. The broker seems to have sold a product they did not fully understand, instead of Kinsale misrepresenting the product itself. It sounds more like a communication breakdown between the broker and the insured, especially since Kinsale most likely did not deal with the insured directly.

The insured wanted equivalent coverage. The broker allegedly placed something else. Why is the conclusion that Kinsale’s entire business model is fraudulent?

Repeating myself here: Kinsale decides what risks it is willing to cover and at what price. If customers or brokers do not like the terms, they are free to seek quotes elsewhere. My guess is that many complaints arise not because Kinsale misrepresented the product, but because the insured either did not read the policy carefully or did not fully understand what was and was not covered.

This is also why customer complaints need to be interpreted carefully. Reviews and complaints are naturally skewed toward negative experiences. The vast majority of customers who are satisfied with their coverage will never file a complaint (why should they?) or leave a positive review, while unhappy customers are far more likely to speak up. So, a handful of complaints may sound emotionally powerful, but they do not automatically prove a systemic issue with the business model.

“We sell coverage. It is not an all-encompassing policy. It covers certain perils.” (Michael Kehoe)

4. “Kinsale’s retention is unusually low”

This is another area where the comparison seems flawed, leaving the impression that the argument was not particularly well researched.

“They have a 60% retention rate, which for a P&C insurer is extraordinarly low. […] Most P&C insurers have a 90% retention rate.” (Bradley Safalow, PAA Research)

How can you compare a standardized P&C insurer with a highly specialized E&S insurer?

Kinsale is not a standard personal auto or homeowners insurer. It is an E&S carrier writing unusual, hard-to-place, and often changing small-business risks.

In E&S, accounts move in and out of the market. Businesses close. Risks get reclassified. Prices change. Terms change. Some accounts become admissible again. Brokers shop renewals. A retention number that looks low versus standard P&C can be normal in E&S.

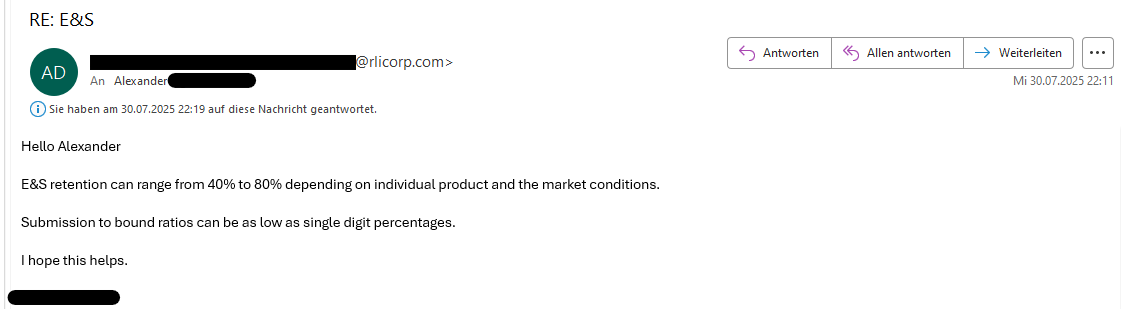

I actually asked one of Kinsale’s competitors (RLI) about this last year.

Against that backdrop, Kinsale’s retention does not strike me as particularly low (and it’s been pretty consistent over the years).

6. “The public records complaints prove a broader pattern”

Public records requests are useful. I like this kind of work. Pulling complaint files from insurance regulators is exactly the sort of primary-source research investors should do more often.

But complaint files are not conclusions. They are allegations, correspondence, and sometimes regulator responses. The key question is whether Kinsale has more confirmed complaints, worse outcomes, or more regulator findings than comparable E&S carriers.

That is why I asked Edwin whether he had also run public records requests on competitors. If the answer is ‘yes’, and Kinsale clearly stands out, that would be interesting. If the answer is ‘no’, the evidence is much weaker.

So far, he has not replied. I would cautiously interpret that as a “no.”

7. “Kinsale has no moat”

This is where I disagree most strongly.

The bear case frames Kinsale as a low-quality insurer temporarily benefiting from aggressive pricing and weak regulation.

My view is the opposite: Kinsale’s moat is the combination of a highly focused E&S model, centralized operations, an in-house technology stack, full control over underwriting, avoidance of MGAs, very fast broker response times, and a structurally lower expense ratio. In a competitive insurance market, a 10–20 point cost advantage is a real strategic weapon. I covered this in much more detail in Part 2 of the following article:

What would actually change my mind?

The right way to test the bear case is not to collect the scariest complaint files and stop there. The right way is to build a comparative evidence base.

I would take the bear case much more seriously if we saw one or more of the following:

Confirmed complaint ratios that are materially worse than comparable E&S carriers, adjusted for premium, policy count, and line of business;

A pattern of regulator findings, enforcement actions, or court decisions showing that Kinsale systematically denied valid claims;

Evidence that brokers broadly view Kinsale’s product as low quality but place business there anyway because of distorted incentives;

Reserve development or loss emergence that shows the claimed underwriting superiority was largely accounting noise;

A competitor comparison showing that Kinsale’s exclusions, audit practices, and claims closures are genuinely abnormal.

That would be real evidence. A handful of anecdotes, some of which appear to have been resolved in Kinsale’s favor or corrected by Kinsale, is not enough.

The actual risk is more boring

None of this means Kinsale is risk-free. The real risks are more boring and probably more important.

E&S is cyclical. Property pricing has already become more competitive in some areas. Casualty inflation can surprise insurers. New capital can enter the market. Growth can slow sharply when Kinsale refuses to chase underpriced business. The company’s stock has historically carried a premium valuation, and when growth decelerates, that premium can evaporate quickly.

Kehoe basically said this himself. Growth can be 20%, 30%, or 40% in some periods, and 1% in others. That is the nature of disciplined underwriting. A good insurer does not grow because Wall Street wants a smoother chart. It grows when the risk-adjusted economics make sense.

The stock is down. That does not make the shorts right.

When PAA Research presented its short case in July 2025, Kinsale’s share price was materially higher than it is today. Since then, the stock has fallen ~35%, while earnings have continued to grow. That means the valuation has compressed significantly. In fact, Kinsale is now trading at the lowest forward P/E multiple in its public history (down significantly from an inflated P/E of 70 some years ago).

But a falling stock price does not automatically validate the short thesis. The key question is why the stock declined. In my view, the answer is much less dramatic than the bear case suggests. Kinsale is facing a softer E&S market, lower property pricing, tougher growth comps, and a normal cyclical slowdown after several exceptional years. That can absolutely pressure the multiple, especially for a stock that used to trade at a premium valuation. But that is very different from saying the business model is broken, low quality, or unsustainable.

In other words: the shorts may have been directionally helped by the stock’s de-rating. But that does not mean their underlying arguments were correct. A cyclical growth slowdown is not the same thing as structural impairment.

At the same time, the forward return profile becomes increasingly attractive from this valuation level. As earnings continue to compound while the multiple stays low, shareholders can still earn a solid return through earnings growth alone. But if growth reaccelerates as the E&S cycle improves, the P/E multiple could expand again as well. That would create a double return engine: earnings growth on the one hand and multiple expansion on the other.

Bottom line

The Kinsale short reports are getting annoying because they keep returning to the same narrative without, in my opinion, clearing the evidentiary bar required to make the conclusion credible.

Yes, Kinsale writes difficult risks. Yes, policies have exclusions. Yes, customers sometimes complain. Yes, Kinsale may be more aggressive than peers in claims handling. And yes, E&S insurance is less standardized and less tightly rate/form regulated than admitted insurance.

But none of that proves that Kinsale is a low-quality, unsustainable business.

My interpretation remains the opposite: Kinsale is a disciplined, cost-advantaged, technology-enabled E&S insurer that has built a rare operating model in a market where most competitors are constrained by legacy systems, fragmented cultures, MGA dependence, and weaker cost structures.

The burden of proof is on the short case to show that Kinsale is an outlier, not merely that Kinsale has unhappy customers and coverage disputes like every insurer writing complicated risks.

It would be interesting to check with the states in, say Kinsale's top 5 for underwriting and see what the complaint rates are, e.g. complaints per policy or complaints per $1M premium (states vary a bit in what they track data on, so you may have to be flexible). If Kinsale's complaint rates are similar to other competitors, then that short argument would appear to be less valid.

Good job, Alexander, as usual. Just want to make two comments:

1. Handling all the underwriting and claim functions internally is a strategic decision. Closely scrutinizing every claim is probably quite natural, versus the MGA model.

2. Although I agree with your statement that the price going down by 35% does not prove the short case was right, as with Brad Safalow of PAA Research's July 2025 original publication. However, there were some valid points in Brad's arguments, such as the extreme valuation and macro headwinds. It's a masterful short in July 2025, and I think the PAA folks are sharp. Whether they are right or not does not really matter as long as they got the 35% decline right.

I advised caution several times in two quality communities and on Twitter/X since middle-2025. However, when the Bear Cave short article dropped, I felt it was a bit silly and a little "Johnny-Come-Lately". As I commented by quoting Buffett, "What the wise do in the beginning, fools do in the end."